Tom Yeung here with your Sunday Digest.

Could a spark light private credit markets on fire?

According to former Goldman Sachs CEO Lloyd Blankfein, the answer is clear:

Absolutely.

In a Bloomberg Television interview this week, the Wall Street veteran warned that the recent panic around private credit funds could be a signal of more trouble ahead.

“You accumulate tinder on the floor of the forest and eventually a spark will come,” Blankfein said. “We haven’t had a crisis for a long time, that itself is a reason for concern, because… you haven’t had to sell in distress things that accumulate on your balance sheet that might not be marked correctly.”

In other words, a lot of trouble could be hiding within Business Development Companies (BDCs) – the funds that invest in illiquid private firms and sell shares to the public. Their investments are not “marked to market,” so losses can hide in plain sight. It’s the same accounting magic that allowed banks to obscure losses leading up to the 2008 global financial crisis.

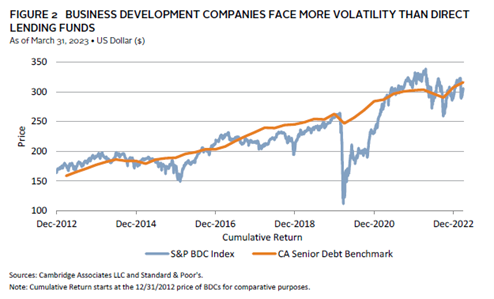

It’s hard to overstate how popular these private-market funds are, or how much trouble they might cause. The top 40 publicly traded BDCs were valued at almost $80 billion last year, and this “shadow banking” system is worth as much as $3 trillion once you include private-market deals and other financing vehicles.

Few other places offer the double-digit dividends that retirees and risk-averse investors seek out.

Even fewer allow the “Four Horsemen” of dangerous investing – complexity, concentration, leverage, and illiquidity – to roam so openly.

The opaque structures have now begun to crack. Last September, automotive supply company First Brands filed for Chapter 11 bankruptcy, triggering a selloff in the BDCs that owned shares. One fund with roughly $22.5 million locked up in First Brands saw its stock price plummet 30%.

The trouble has only snowballed. In November, Blue Owl Capital Corp. (OBDC) called off a merger because too many investors were pulling their money out. By late March, at least four major private-market funds had limited how much investors could withdraw – a move that tends to trigger exactly the panic it’s meant to prevent.

After all, every BDC investor knows that these funds can run into trouble even if they’re solvent. When enough panicked investors sell shares, all at once, the resulting decline in stock prices generally prohibits BDCs from raising fresh capital. That can indirectly cause a wider fire-sale if the fund then fails to meet asset-coverage ratios required by the Securities and Exchange Commission.

So, how afraid should we be of a spark that lights the private capital markets on fire?

The Next Credit Crisis

InvestorPlace Senior Analyst Louis Navellier believes we should be very, very concerned. There’s a lot more that can still go wrong in private credit, and he believes that a $3 trillion crisis in this “shadow banking” business is nearing a breaking point.

He identifies June 30, 2026, as the most likely date we’ll see a reckoning, and he explains why in his latest presentation here.

There are three key reasons you should pay close attention… and not only because Louis also predicted the collapses of Enron, Lehman and Silicon Valley Bank.

First, BDCs and other private credit funds have had years of ultralow interest rates and rising asset prices to gorge themselves on questionable deals.

Bought a company for too much?

Don’t worry, someone else will buy it from you for even more next year.

Have a $100 million loan that’s coming due?

Go ahead and refinance it. The Fed’s rate is near zero.

In fact, the First Brands blow-up was a poster child of a bad deal hiding in plain sight. Few funds questioned the aggressive debt-financed growth of the automotive supply firm. And no one bothered asking how a CEO with a history of alleged misrepresentation (and getting sued by former business partners) was able to borrow more than $10 billion to finance his empire.

And if a high-profile company like First Brands got away with it for so long… how many more “cockroaches” could be hiding among lesser-known firms?

Secondly, BDC ownership is overwhelmingly made up of dividend-seeking retail investors. This cohort has a history of panic selling during times of crisis, and global investment firm Cambridge Associates notes that the group was happy to unload BDCs well below net asset value in 2020.

As Louis outlines in his latest presentation, this is something that could well happen again. Fear is contagious, and BDC redemptions could go from “bumping up against limits” to an all-out dash for the exits.

Finally, the agentic AI-instigated bloodbath in the software industry could soon spill into BDC valuations. As Louis explains, software firms are some of the largest borrowers in private credit markets, and all are now facing existential threats from AI automation.

Shares of blue-chip software companies like Salesforce Inc. (CRM) have already plummeted 36% from their peaks, and Louis believes these losses will become apparent by his June 30 deadline.

So, what can investors do? Well, earlier, I mentioned that BDC owners are overwhelmingly retail investors.

I’m not talking about the meme-stock crowd. Most social media users under 40 would never have heard of Ares, Hercules, or Prospect Capital.

Instead, BDC owners are typically older individuals seeking consistent dividend income. They’re the ones looking at Ares Capital Corp. (ARCC) – the world’s largest BDC – and snapping up shares to enjoy a 10.5% dividend yield. Smaller firms like Oxford Square Capital Corp (OXSQ) and Great Elm Capital Corp (GECC) offer yields of 20% or more. (GECC was the $16.5 million investor in First Brands that lost 30%.)

That’s important, because investors rotating out of BDCs will not be reinvesting their cash into low-quality moonshots or speculative growth firms.

Instead, they will be seeking alternative sources of dividend income.

And so, we should expect high-yielding quality stocks to outperform as this rotation gets underway. There could be a lot of cash flowing out of private markets, and investors will be parking it in these types of investments.

Louis talks about this in greater detail in his latest presentation, which you can see here. And in the meantime, I’d like to illustrate his thinking with three companies that fit this bill.

Profiting from America’s Shale Exports

Much of America’s natural gas has historically been “trapped” in the Permian Basin. Older interstate pipelines ran to the wrong places, and so gas was flared, trucked, and even sold to buyers at negative prices. Texas’ Waha Hub prices have often drifted below zero as a result.

That’s where Energy Transfer LP (ET) comes in.

The company operates one of the largest pipeline networks in America and runs several indirect routes from the Waha Hub in West Texas to the Texas Gulf Coast, where gas is compressed and exported as liquefied natural gas (LNG). Energy Transfer plans to open a more direct Waha-to-Gulf route later this year. ET is also a major player in natural gas liquids (ethane, propane, etc), where it holds a 20% global share of exports. And it’s seen demand surge due to insatiable AI demand and LNG shortages from war in the Middle East.

Best of all, Energy Transfer is a low-leverage, income-earning play that offers a 6.9% dividend yield and plenty of room for growth. Its upcoming Waha-to-Gulf pipeline offers a near-term catalyst, and several more pipelines are planned to come online by 2029.

Analysts expect free cash flows to surge 28% this year, 31% in 2027 and 8% in 2028. Shares trade at just 6.5X forward cash flows, making it my favorite midstream company right now.

A Blue Chip on Sale

Investors exiting BDCs will also be seeking out more traditional dividend plays. And Kimberly-Clark Corp. (KMB) sits at the perfect intersection of having 1) high dividends, 2) consistent profits, and 3) a defensible business.

Kimberly is a household goods company that owns six key brands: Huggies, Scott, Kleenex, Cottonelle, Depend, and Kotex. Each generates over $1 billion in annual sales, and profit margins are high.

The Dallas area-based company generated 44% returns on capital invested last year, second in its class only to Proctor and Gamble Co. (PG). KMB also plans to acquire Kenvue Inc. (KVUE), Johnson & Johnson’s (JNJ) former consumer health division. That will add brands like Tylenol, Neutrogena, and Band-Aid to Kimberly’s portfolio.

This acquisition has clearly spooked investors. KMB’s shares have plummeted 18% since announcing the acquisition last November, because everyone knows Kimberly’s profit margins will decline in the short term. Kenvue’s lineup is not nearly as profitable as Kimberly’s existing portfolio.

Yet, markets are also forgetting that Kimberly has a long history of building strong brands in commodity-like markets. Despite some stumbles abroad, the firm has managed to convince the world that it’s worthwhile to pay a premium for branded tissue paper.

In addition, the recent selloff now prices KMB’s stock at a 5.3% dividend yield – well above its long-term average of 3.6%. (Lower stock prices mean higher dividend yields.) Shares trade at their most attractive levels since 2012.

So, even though Kimberly lags the industry leader, its high dividend and reasonably defensible business should be enough to tempt conservative investors its way.

The Conservative REIT

As I’ve said before, Realty Income Corp. (O) is the REIT to buy and hold forever.

It is the only Dividend Aristocrat that offers monthly dividends, and it maintains an ultra-conservative profile by favoring “triple-net” leases where the tenants pay for utilities, taxes, and other costs. Realty’s shares have advanced 15% since I wrote about them in mid-2024, compared to a 26% collapse in the BDC index (including dividends), as measured by the VanEck BDC Income ETF (BIZD).

The downside of this conservatism is slower growth. Management will often sacrifice higher rental income to secure better clients, making Realty Income the opposite of hypergrowth data center plays like Digital Realty Trust Inc. (DLR) or CoreWeave Inc. (CRWV).

However, “slower” doesn’t mean “zero.” The company has grown its Adjusted Funds From Operations (AFFO) per share by 4.6% annually over the past decade – outpacing most of its triple-net rivals. Analysts expect another 4.1% growth this year, and its 5.3% dividend yield is especially attractive.

For conservative investors, Realty offers a way to help savings grind higher over time.

Buying Quality

Energy Transfer, Kimberly-Clark, and Realty Income all have this in common:

They are high-earning companies that clearly explain how their dividends are made.

The companies will face no surprise revaluations… no sudden withdrawal limits… no financial blowups that threaten BDCs. Instead, they will be pumping gas, selling Kleenex, and renting retail space while sitting on their strong balance sheets.

Meanwhile, BDCs are looking increasingly at risk. Bloomberg reports that around $5 billion of capital is now trapped in the private credit industry – stuck behind redemption limits. More asset managers are expected to impose curbs in the coming weeks.

That could create a feedback loop that spirals out of control.

“I don’t see anything systemic,” Lloyd Blankfein conceded in that same interview. “But by the way, I didn’t necessarily see anything systemic in the run-up to the [2008] crisis, which is why that’s the nature of bubbles. Everyone sees it in hindsight, but no one sees it in prospect.”

That’s why you’re going to want to hear what Louis has to say in his new free presentation. In it, he explains why a new wave of bankruptcies could rock the U.S. stock market, and how the shake-up will create devastating losses for some investors… and riches for others.

Click here to sign up for the event.

I’ll be out for travel next week, so I’ll see you back here in two weeks.

Regards,

Thomas Yeung, CFA

Market Analyst, InvestorPlace