Listen to the audio version of this article (generated by AI).

Tom Yeung here with your Sunday Digest.

When people talk about the year “1999,” most investors will immediately tense up. That year was the start of a terrible stretch for the value-focused buy-and-hold crowd. The dot-com bubble burst meant that anyone who bought the Nasdaq Composite in January that year would have been in the red until 2006… just in time for the global financial crisis two years later.

Experienced growth investors will also shudder at the thought of 1999. Many internet companies saw their share prices peak early that year, including Lycos (March), Priceline (April), and TheStreet.com (May). In fact, many smaller dot-coms were already on their way out by the time 1999 began.

That means when Louis Navellier says he thinks today’s market looks a lot like 1999, he’s really saying two things:

- Bullish. Much like the internet, AI is justifying more gains to come. Consumers and companies are paying handsomely for the best AI models, and industry leaders are generating record profits as a result. Anthropic, an AI startup that lost roughly $5.2 billion last year, expects to swing to an operating profit this quarter.

- Bearish. However, high valuations today make for an extremely fragile bull market. Smaller AI laggards are already fading away, and indebted ones like Oracle Corp. (ORCL) are showing cracks in their balance sheets. Louis forecasts a highly volatile summer and the possibility of a meaningful pullback.

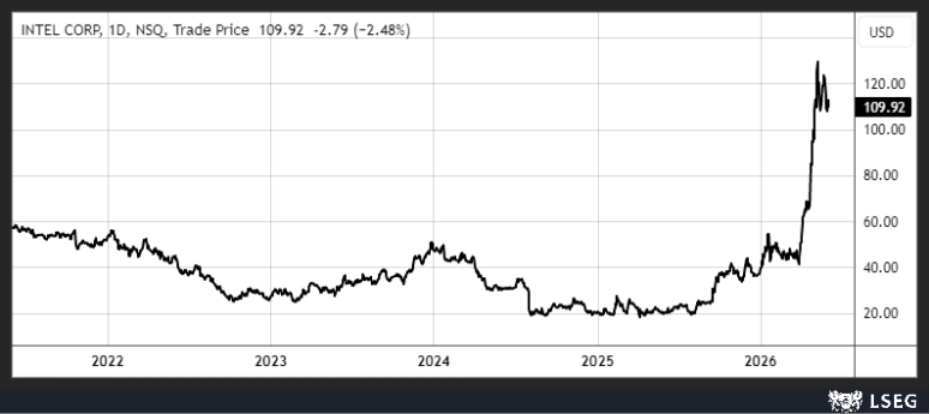

After all, if so many AI stocks are starting to look like hockey-stick charts like the one from Intel Corp. (INTC) below, it’s easy to see how ugly a selloff can get.

INTC stock price

Source: LSEG

To navigate this increasingly brittle rally, Louis has become far more selective in the stocks he’s recommending. And to do that, he’s partnered with TradeSmith CEO Keith Kaplan to build a new AI-driven investing system that combines his Stock Grader research with TradeSmith’s market-timing technology.

The result is a new Tactical Profits Portfolio that selects the best AI-focused companies with strong fundamentals that can withstand drawdowns. It also helps flag weaker players at risk of losing ground.

On Thursday, June 10, Louis will sit down with Keith and explain the work they’ve done with their system and how their stock-selection tools have helped investors navigate past volatility.

You can sign up for their presentation here.

Today, I’d like to give a sample of five stocks that pass this threshold, and another three that fail it. And if you’re worried about the stocks in your own portfolio, you can register for their event and use their free ticker tool for a limited time to check their short-term health.

Five High-Quality Names for a Volatile Summer

Readers will immediately notice that the five companies in this list are wide-moat firms trading at surprisingly reasonable prices. All run like quasi-monopolies, giving them the strength to outlast a market selloff. And all were recently ranked well by both Louis’ Stock Grader and TradeSmith’s market-timing system.

1. Nvidia Corp. (NVDA). The “king of AI” continues to expand its domain. Last week, at Computex 2026, CEO Jensen Huang revealed that the chipmaker plans to move into personal computers (PCs) with a new chip called the RTX Spark that combines AI and traditional computing power.

His rationale is straightforward: PCs are looking much like the “dumb phones” from the 1990s. Their purpose has not changed in decades, even though technology has marched ahead. Today, smartphones are used for everything except making calls. Why can’t the same happen for a reinvented laptop?

In addition, Nvidia continues to surprise even its greatest fans. Last month, the company announced its 14th consecutive earnings beat. Earnings per share grew 95% to $1.87, surpassing consensus by 6%. The company has expanded its supply chain faster than Wall Street expected and kept its lead in AI chips. At Computex 2026, the company additionally announced that its next-gen Vera Rubin AI supercomputer is already ramping into full production – delivering on a promise Nvidia made in 2024.

By my calculations, that means Nvidia’s fair value is closer to $300 per share today, up 40% from its current share price. The firm is dominating its industry, and its solid “B” rating in Louis’ Stock Grader suggests it’s an excellent company to buy, even after its multiyear run.

2. Alphabet Inc. (GOOGL). Meanwhile, Google’s parent company is the only major hyperscale AI data center firm expected to remain cashflow positive in every quarter this year. Analysts expect net cash inflows of $18 billion in 2026 (despite $185 billion in data center spending). That’s thanks to a combination of:

- A dominant search business. Search revenue growth hit 19% growth last quarter, and the remainder of 2026 should see a windfall from record political ad spending for the midterm elections.

- Efficient data center chips. Alphabet began building custom “TPU” chips as early as 2013 to handle its voice-to-text system on Android phones. These purpose-built chips have allowed the firm to run its AI models far more efficiently than rivals’. Studies show Alphabet’s TPUs delivering between 1.6X and 4X more performance per dollar than general-purpose GPUs.

- A winning AI model. Google’s Gemini 3.5 AI model has proven exceptionally capable, and it’s beginning to steal consumer market share from OpenAI. Betting markets expect Google to have the second-ranked model behind Anthropic by the end of 2026.

That suggests Alphabet’s fair value is somewhere in the mid-$400s range, according to my math. The company’s vertical integration is proving to be a durable competitive advantage, and the advantage looks set to expand over time. Louis’ and TradeSmith’s system both agree.

3. Advanced Micro Devices Inc. (AMD). Over the past several years, AMD has capitalized on Intel’s stumbles to establish itself in the CPU market. It has gone from less than 10% market share to about a third overall – and provides nearly half of all server CPUs. Its evolution from near-bankrupt company to world-beater got CEO Lisa Su named Time magazine’s CEO of the Year 2024.

Markets might still be underestimating AMD’s potential.

In a recent earnings call, Su noted that the CPU-to-GPU ratio should move from a 1-4 or 1-8 ratio today to 1-1 in the coming years. She joins the bosses of Intel and Arm Holdings PLC (ARM) in predicting the return of the CPU.

I believe they’re right (even though they’re all CEOs of CPU companies).

That’s because AI is shifting from mostly training and simple inference to agentic inference. This new type of AI requires far more “thinking,” where AI models will plan, call tools, run code, inspect results, and sometimes run in circles before asking for help. GPUs are still needed to run AI models, but CPUs are then used to orchestrate and analyze results.

That should put AMD on a far faster growth track than people expect. Analysts are currently expecting growth to taper off by the end of 2027, but I expect demand could last through 2030. Louis’ and Keith’s systems both agree, awarding AMD their top bullish scores.

4. Taiwan Semiconductor Manufacturing Co. Ltd. (TSM). Taiwan Semi (also known as TSMC) is the world’s largest contract chip manufacturer. The firm controls roughly 70% of the market and is the only chipmaker capable of manufacturing the advanced 2-nanometer process at profitable scale. It is now working on the A16 and A13 nodes.

Expectations for the company are surprisingly modest. TSMC trades at just 28X forward earnings and 21X forward cash flows – well below less established firms like Intel and China’s Semiconductor Manufacturing International Corp. (SMIC). Investors have become conditioned by years of boom-bust cycles in the chip “fab” business and typically view incumbents with skepticism. (Upstarts typically get a free pass during boom times.)

Yet, skeptics will ignore the Taiwanese firm at their own risk. Like Nvidia, TSMC has been able to raise prices thanks to insatiable AI demand. The company expects capacity to rise just 7% in 2026, meaning that over two-thirds of its 31% revenue growth is coming from price increases. Its monopolistic position means further price increases are likely.

Consolidation among semiconductor companies has also created demand for more complex chips. Larger firms like Nvidia and AMD are combining GPUs, CPUs, and memory components into integrated products, and these complicated chips require the type of leading-edge nodes that TSMC produces. Though Taiwan Semi is more of a “grind higher” company because of its capital investment needs, it’s still a solid enough company that should weather a selloff. The company earns top marks in Louis’ and Keith’s system.

5. Analog Devices Inc. (ADI). Finally, we have Analog Devices, one of the world’s largest analog and mixed-signals chipmakers. The company has a particularly wide lead in high-performance signal processing chips – the devices that convert real-world information (light, sound, temperature, voltages) into the usable “0s” and “1s” that digital chips need.

Profits are high thanks to years of investments and high customer switching costs. Operating margins have hovered around 40% since 2020. Growth is also quite reasonable, thanks to the rise of electric vehicles, robotics, and “internet of things” devices. Analysts expect revenues to increase 34% this year.

The AI boom now offers three new paths for growth.

- Advanced robotics. The most established way for Analog Devices to grow is through providing chips for AI-powered devices. Every AI-enabled phone, car, camera, robot, and wearable device must convert analog data into digital information.

- Chip power systems. High-end GPUs pull hundreds of watts, and their inconsistent demands create voltage spikes that power systems must smooth out. According to a report from Deloitte, power systems cost between 5% to 10% of a typical AI server rack. That benefits Analog greatly – data center product revenues rose 76% in the most recent quarter).

- Analog AI computations. Researchers are now exploring analog AI chips that can store more than binary 0s and 1s. Though commercialization of this technology is years away, this could provide Analog Devices with a powerful growth engine down the road.

Together, that makes Analog one of my top long-term companies to buy. The company has a durable moat in analog chips, and its strong quantitative scores from Louis and Keith suggest there’s still time to get in on this high-quality firm.

Knowing When to Sell

Louis’ and Keith’s systems also make it clear that some AI stocks are off the table. These include:

Not only are the fundamentals at these firms deteriorating – often from AI competition – but short-term momentum is also turning decidedly negative. That’s a highly bearish sign in this returns-chasing market. No retail investor wants to hold a sinking stock.

These are not the only companies at risk.

In their upcoming presentation, Louis and Keith caution why the months ahead could be much more volatile than many investors expect… and why comparisons to 1999 are both an encouragement and a warning for investors today.

You can register for their presentation here.

I’ll be out of town next week, so I’ll see you back here in two weeks

Regards,

Thomas Yeung, CFA

Market Analyst, InvestorPlace