Twilio (NYSE:TWLO) was once heralded as a top pick among growth investors. Now, TWLO stock seems to have fallen by the wayside to a degree, as investors turn their attention to Shopify (NASDAQ:SHOP), Roku (NASDAQ:ROKU), and others.

There has also been a resurgent focus on names like Amazon (NASDAQ:AMZN) and Netflix (NASDAQ:NFLX) as the novel coronavirus keeps our world in an altered state. But that doesn’t mean investors should forget about Twilio.

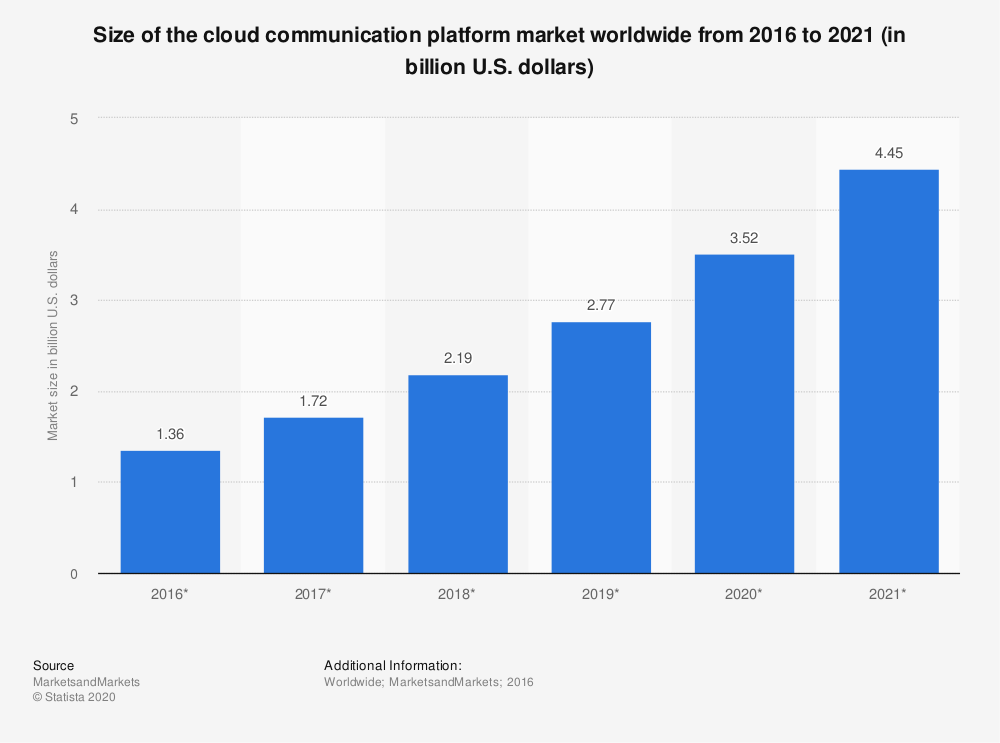

This company serves as a cloud-based communication platform for some of the world’s largest and newest companies. Does that create opportunity or risk? In the short-term, perhaps it’s the latter, but in the long-term, it’s the former.

Coronavirus and Twilio

Some companies are seeing a big uptick in usage thanks to the outbreak of coronavirus. That is, companies like Roku, Netflix, and Zoom Video (NASDAQ:ZM) are all seeing a demand spike thanks to lockdown and stay-at-home orders.

For Twilio, it’s unclear how it will affect the top and bottom line.

On the one hand, customers like Uber

(NYSE:UBER), Lyft (NASDAQ:LYFT), and Airbnb are certainly under pressure. A decline in trips — whether across the world or across town — hurt these guys. But on the other hand, Netflix, DoorDash, Hulu, Instacart, eBay (NASDAQ:EBAY) and Shopify are all Twilio customers too.

Obviously Netflix doesn’t communicate with customers as much as a company like Uber. However, investors would like to think Twilio’s exposure to these types of companies helps to offset weakness in other areas.

In essence, the company faces short-term risk due to the virus outbreak, but it should be just that — short term. Twilio still has growth and long-term catalysts in play.

A Closer Look at TWLO Stock

Analysts have started to take to Twilio. Rosenblatt analysts cut their price target to a Street-low $80 and downgraded shares tio “neutral” from “buy.” They argued that there will be a “major decline” in GDP among the world’s largest economies, which will drive a “sharp Q2 decline” in Twilio revenue.

Others have cut estimates too, including Needham, who didn’t downgrade the stock but cut its price target from $145 to $130. It also includes Piper Jaffray analysts, who cut their price target to $90 from $151. They also lowered their 2020 revenue growth estimates from 31% to just 10%.

There are some positive analysts out there, but by and large, the tone feels negative. Most analysts acknowledge that it should be a short-term hit, but one that likely weighs on the stock price. It’s unfortunate, but pragmatic.

However, let’s not miss what TWLO stock brings to the table. When Twilio last reported earnings in early February, it delivered a top- and bottom-line beat. While revenue guidance for the current quarter and the full year topped consensus estimates, earnings guidance fell short.

Ultimately, management plans to keep running the business at a slight loss vs. the slight gain that analysts were expecting. On the surface, that’s not the end of the world, but it’s discouraging that, even as the company continues to grow, its bottom line won’t stay on the right side of zero.

That’s even more true with Twilio’s SendGrid acquisition. The deal gives the company a nice boost to revenue, but also opens it up to an email product. SendGrid sends email to more than half the world’s email addresses and has been profitable for eight straight quarters. It should help.

The Bottom Line

Click to Enlarge

At the end of the day, Twilio is still a solid growth company in an enviable position. Its cloud-based communication plays right into the hands of investors looking for secular growth themes and allows a more seamless line of communication between companies and their customers. The acquisition of SendGrid opens up another addressable market and allows TWLO stock to benefit from cross-selling to current customers.

Here’s the thing, though. When the company reported earnings, TWLO stock fell out of favor with investors. It did rebound a bit in the ensuing days, but investors did not like management’s outlook. They want to see the bottom line over break-even while revenue continues to accelerate. While stocks can certainly still be buys while running at a loss, knowing that profits are at least somewhat of a priority can go a long way.

Now up near $110, I would love to see a dip in TWLO stock. Something down into the $70 to $85 range would give long-term investors a solid opportunity to buy and hold this quality growth name.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.