Nvidia Corporation (NASDAQ:NVDA) is perhaps one of the greatest companies in the stock market. Now focusing on datacenter, machine learning, self-driving cars and other high-growth industries, NVDA stock is set up in front of long-term tailwinds. Shares are already up an astounding 724% in the past two years.

Momentum last quarter was breathtaking. Revenue grew almost 50%, while GAAP earnings soared 126%. Gross margins of 59.4% were higher by 190 basis points year-over-year (YoY).

We recently discussed the strength of the cloud, highlighted by Alibaba Group Holding Ltd (NYSE:BABA) growing its cloud segment by 121% in fiscal 2017. Others are robust too, like Alphabet Inc (NASDAQ:GOOGL, NASDAQ:GOOG), as well as Microsoft Corporation (NASDAQ:MSFT), which grew its Azure cloud revenues 97% last quarter.

Last quarter is also when Nvidia put Google Cloud, International Business Machines Corp. (NYSE:IBM) cloud, Baidu Inc (ADR) (NYSE:BIDU) and Microsoft’s Azure on its customer list. And then, with those names and others, datacenter revenue nearly tripled YoY.

NVDA is training 100,000 developers using its deep-learning products — 10 times last year’s count. As deep-learning and artificial intelligence businesses gain momentum, developers will turn to the products they know and trust. In this case, it will be Nvidia. It’s new Volta GPU architecture is hoped to be at the forefront of the artificial intelligence (AI) revolution.

Nvidia’s DriveWorks kit for advanced self-driving allows for level 3 to level 5 autonomy (level 5 being the highest). The sophistication of this kit enables developers to get right into making their own system, rather than having to start everything from scratch. As autonomous driving continues to gain momentum, higher priced and advanced kits like this will drive sales and margin expansion.

Source: Nvidia/Nasdaq OMX

{kind=link}

Moving Forward on NVDA

For Q2 fiscal 2018, management expects a 50-basis-point improvement in GAAP gross margins. They expect revenue to climb 36.3% YoY to $1.95 billion. Analysts expect second-quarter EPS to explode by 72%. While next quarter is forecast to be incredible, full-year fiscal 2018 estimates “only” call for 19.3% revenue growth and 20.6% earnings growth. For 2019, estimates call for 19.7% and 13.2% growth, respectively.

On an earnings basis, Nvidia’s not much better, trading with a price-to-earnings ratio of 55 and a forward P/E of 47. If NVDA stock had a P/E of 55 and a forward P/E of say, 25, it wouldn’t be so bad. That would mean robust earnings growth is on the horizon.

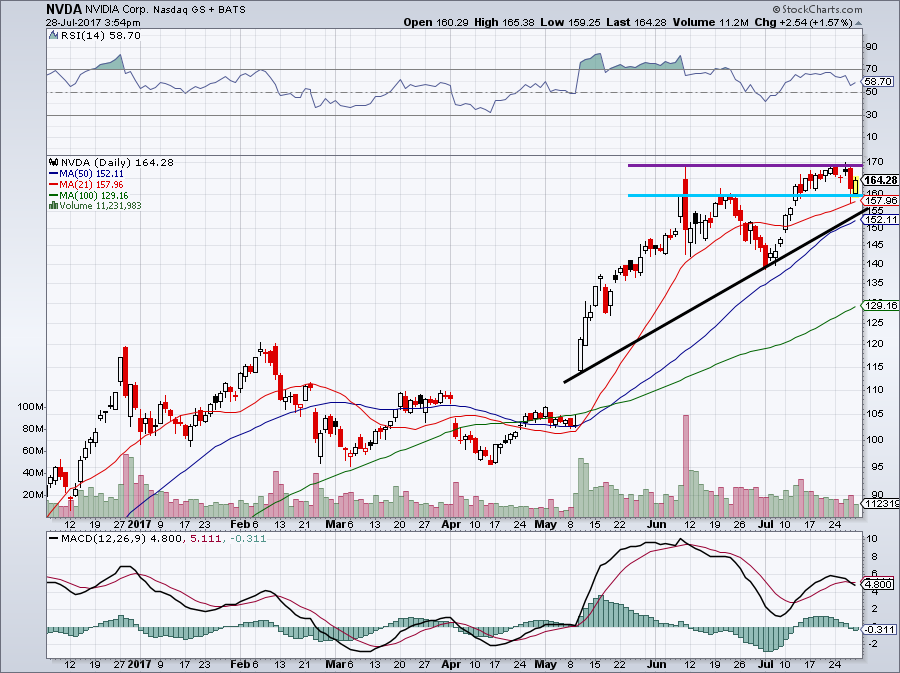

Click to Enlarge

Granted, NVDA has beaten on EPS and revenue estimates for seven straight quarters; it very well could continue to do so and I hope it does.

But the valuation is asinine, with NVDA stock trading at 13 times sales. For reference, Intel Corporation (NASDAQ:INTC) and Advanced Micro Devices, Inc. (NASDAQ:AMD) trade at about 3 times sales.

But it’s not, and 47x forward earnings is expensive.

However, unless a stock has a proven historical valuation range, it’s dangerous to bet against it based on overvaluation. Think Tesla Inc (NASDAQ:TSLA), Amazon and Netflix, Inc. (NASDAQ:NFLX). All currently have and have long had an extreme valuation. Shorting them would’ve be lethal (financially speaking). Thus far, shorting NVDA has been, too.

The Bottom Line on NVDA Stock

If you want to go long NVDA stock, I’m sorry but you’ve missed the boat. Three months ago, shares were at $95. Now they’re at $165. Investors shouldn’t chase it after that big of a move.

If you’re a nimble trader, there are spots to choose from. Twice NVDA stock has failed at $170, but you’re on your own if you want to bet against it. Until NVDA stock really breaks down, I would be a dip buyer rather than a rip seller. The 50-day and 21-day moving averages (above) along with trend-line support (black line) are all nearby. Decent, but not great support at $160 (blue line) is also there.

Traders can buy NVDA stock here with a stop-loss just below support if they want to play for more upside. Otherwise, longer-term investors need to wait. If a tech-wide selloff materializes, Nvidia will be anything but immune. A pullback to $120 would be an excellent spot for long-term thinkers.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.