Square Inc (NYSE:SQ) has been absolutely on fire. SQ stock is up 96% this year and 161% over the past 12 months. While CEO Jack Dorsey may be struggling to lead Twitter Inc (NYSE:TWTR) to the promised land, he’s doing so with SQ stock right now.

The business is gaining traction and its financials are looking better. After losing 50 cents per share in 2016, analyst expect Square to cut its losses by over half in 2017 and turn profitable in 2018. 25.6% sales growth is forecast for 2017 and estimates call for an acceleration to 26.5% growth in 2018.

Digging Deeper into SQ Stock

In spring 2016, SQ had gross margins of about 29%. Fast forward 12 months and those gross margins are up more than 650 basis points to 35.7%. Gaining market share and growing margins are a huge key to getting investors to open up their wallets and pay a higher valuation.

Last quarter was a big one. Analysts were looking for a loss of 8 cents per share, while SQ came in with a surprise profit of 5 cents per share. Revenue of $461.55 million also beat expectations and grew 21.5% year-over-year. What didn’t grow 21.5% YoY? Operating expenses, which actually shrunk by about $80 million to $475.6 million.

Bears may point out that overall expenses again outpaced revenue. While this is true, a bull will also point out that operating income came in at negative $14 million vs. negative $97 million in the same quarter last year.

Cash from operating activities grew to $44 million last quarter, its third straight quarter with a positive result.

Valuing Square

There is very little doubt about Square’s underlying business. In fact, broadly speaking, the whole ecosystem in which Square operates is improving. SQ is used by many small- and medium-sized businesses, and as we know, the economy continues to improve. It may not be robust, but a growing economy is key to Square’s business.

Payment companies like Visa Inc (NYSE:V), Mastercard Inc (NYSE:MA) and Paypal Holdings Inc (NASDAQ:PYPL) continue to churn higher, too. E-commerce trends, which we identified when taking a closer look at Alibaba Group Holding Ltd (NYSE:BABA), continue to see strong results as well for companies like Amazon.com, Inc. (NASDAQ:AMZN).

Additionally, Shopify Inc (US)

(NYSE:SHOP) turned in another strong report this week as well.

The point is all the same: e-commerce and spending tends are strong, which bodes well for Square.

While the underlying business may be doing well, there are larger questions when it comes to properly valuing the company. Given that SQ is fighting for profitability, it’s hard to judge it on an earnings basis. On a sales basis, SQ trades at 5.5 times its trailing-12-month revenue. That compares to 6x for Paypal.

For PYPL’s part, it’s forecast to grow revenue by 18% for 2017 and 2018. The stock may trade at 26x forward earnings estimates, but PYPL is profitable and expected to grow earnings by 18% to 20% over the next five years.

In this case, one could argue that SQ stock is undervalued to PYPL given its superior revenue growth. However, given PYPL’s profitability, one could also argue it deserves a premium over SQ stock.

Dare we say, SQ is close to fair value?

One Other Consideration

One more important factor is M&A. With a $71 billion market cap, PYPL is hardly an M&A target. However, with its $10 billion market cap, SQ stock could fit in nicely with another company. Of course, 13 months ago SQ traded with a market cap of just $3 billion, so it seems if a buyer were to be lurking, they would have pounced long ago.

However, there’s clear demand for companies in the space.

Less than a month ago, Vantiv Inc (NYSE:VNTV) bought Worldpay for $10 billion. Blackstone Group LP (NYSE:BX) along with CVC Capital Partners offered $3.7 billion for Paysafe less than two weeks ago.

It’s possible that SQ could in the M&A scope for a larger company.

The Bottom Line on SQ Stock

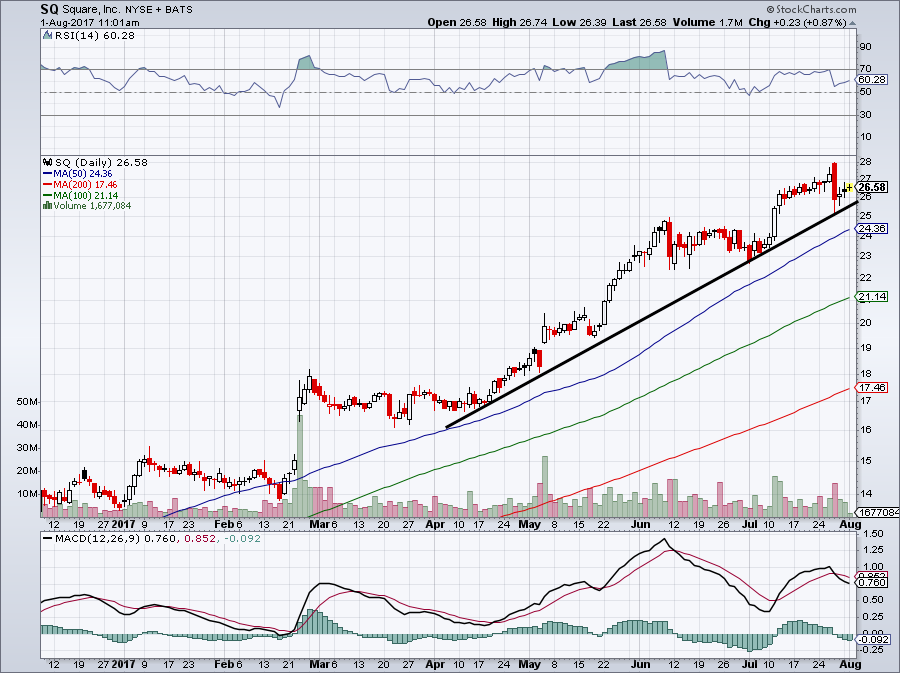

Click to Enlarge

While Square’s business is growing impressively and while it could very well be an M&A candidate, we need caution.

SQ stock is up more than 75% since its February breakout. As much as I believe SQ was severely undervalued before, investors have now seen the value. As a result, they’ve run up the stock price tremendously.

It’s hard to fault investors who have been long to stay long. But new investors would be better off waiting for a pullback. Even a minor pullback to its 50-day moving average near $24.50 may make for a good entry.

A deeper decline to $20 to $22 would be even better, although that type of decline seems unlikely to come without a market-wide selloff.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell held a long position in V and MA.