Back in June I suggested cannabis company Hexo (NYSE:HEXO), in a sea of noisier names like Canopy Growth (NYSE:CGC) and Aurora Cannabis (NYSE:ACB), might be the market’s best-kept marijuana-minded secret. Hexo stock has continued its struggles.

Its hub-and-spoke business model that leans on big-name partners is a savvy approach to low-cost growth its rivals aren’t utilizing.

I followed up on that commentary in late July, further fleshing out the notion that Hexo stock requires a long-term mindset. Near-term volatility threatened to shake shareholder confidence and undermine HEXO shares, in the absence of those partnerships.

The underlying thesis still stands. With plans to add more Fortune 500 caliber partners like its relationship with Molson Coors (NYSE:TAP) at the end of its spokes, this young cannabis name is a name worth watching. But, it’s still a long-term play.

The in the meantime just became very hairy and scary for Hexo stock though, and there’s absolutely nothing to prevent matters from getting worse before they get better.

Sector-Wide Headwinds Persist

More than once since marijuana mania took hold, after Constellation Brands (NYSE:STZ) made a major investment in Canopy Growth, have I warned investors about two related pitfalls of the cannabis craze as a whole.

One of them is the likely price-cutting commoditization of the plant. The other is investors’ impending realization that simply being in the pot business is no guarantee of immediate profits.

The former, incredibly enough,

hasn’t started to happen yet even though the prospect remains on the table.

As for the latter, following second quarter’s industry-wide results it’s quite clear some of these names may never make their way out of the red. Canopy’s quarterly sales of recreational pot actually fell sequentially, per the report from June, and Hexo stock took a beating after an unexpected revenue dip for its most recently-ended quarter.

It’s not the individual stories within the marijuana arena that are of interest here and now though. The movement could shrug off one or two stumbles.

Rather, the cannabis craze has become a groupwide matter again, much like it was in early 2018. All of these names are being lumped together because after the past couple rounds of quarterly reports they all seem to be facing the same underlying headwinds. Those headwinds are (1) the realization that building scale is expensive and difficult, and (2) the fact that recreational demand hasn’t lived up to the palpable hype from a year ago.

And that’s a problem for Hexo stock. With every other major marijuana name losing ground after a few-too-many red flag started to wave this year, the falling tide is dragging the Hexo stock price lower with it.

Pot Stocks Have a Problem

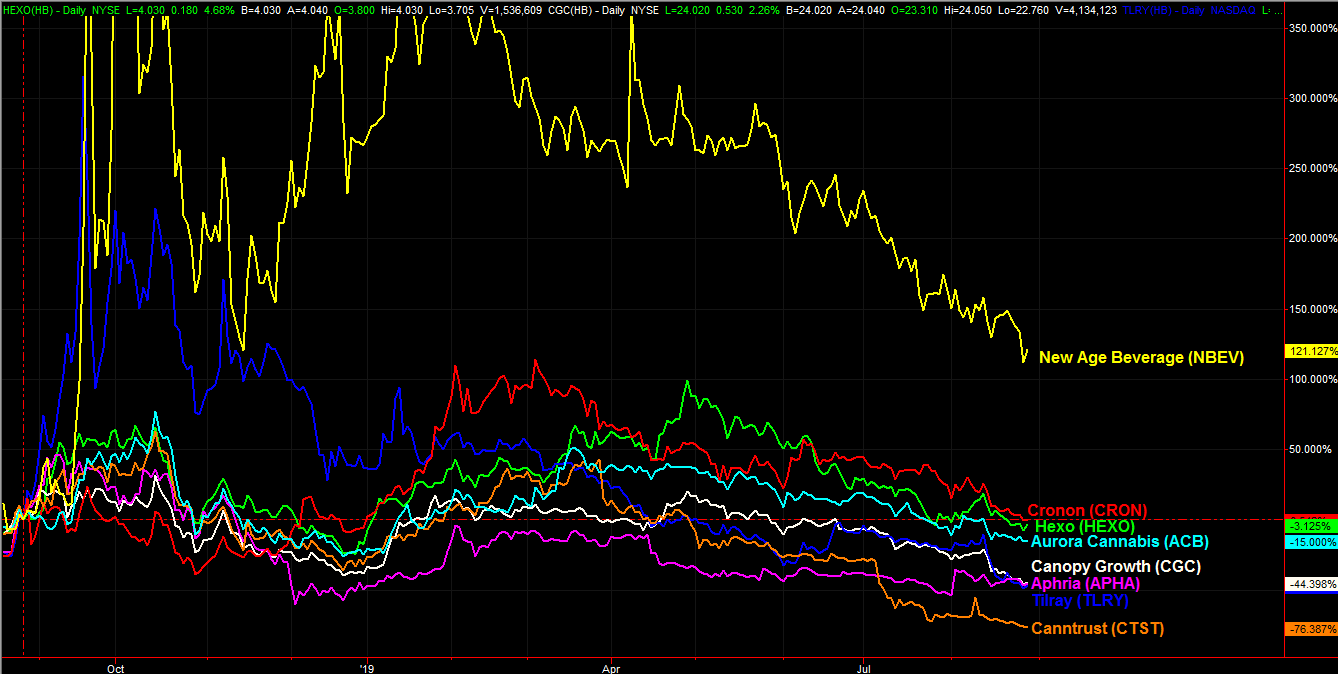

The graphic below tells the tale. Over the course of the past twelve months, with the exception of New Age Beverages (NASDAQ:NBEV), every major cannabis stock is in the red. And even then, a major footnote is merited. That is, of all the marijuana names in focus, NBEV stock has fallen the farthest from its peak. It’s now down nearly 70% from its September-2018 high.

It’s not a mere matter of bad luck or an unfair comparison either. These names have been steadily trending lower, as a group and individually, since April. Several are at or near new 52-week lows.

Click to Enlarge

When one name in a group of eight stocks stumbles, there’s something wrong with that company. When all eight lose ground for four straight months there’s something wrong with the industry.

Admittedly, it may be more about perception than reality. It just doesn’t matter. If the bulk of investors are convinced none of these names are worth holding onto, then these names are going to struggle. Bad news for one leads to bad results for another, creating a self-fueling selloff.

Bottom Line for HEXO Stock

Hexo is still arguably one of the more compelling names in the cannabis business. By putting itself in a support and supply role for major brands that want to plug into the cannabis market, it avoids being forced to make risky investments that may or may not pan out.

Hexo also doesn’t grant large, controlling stakes of itself to its partners the way rivals have. Case(s) in point: Constellation now controls nearly 40% of Canopy Growth, which was enough to oust CEO Bruce Linton in July.

Altria Group (NYSE:MO) now owns 45% of Cronos Group (NASDAQ:CRON), with the option of buying up to 55%. That effectively puts it in charge of Cronos, even though it may not have the same vision as Cronos CEO Michael Gorenstein does. Hexo remains relatively flexible in comparison.

But, so what? All pot-based plays are being treated as liabilities now, and Hexo stock is no exception to that trend.

As to when it might end is anybody’s guess, but the tide’s not likely to turn until at least a couple of these names can prove there’s sustainable profit growth ahead.

I’m not holding my breath.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can learn more about James at his site, jamesbrumley.com, or follow him on Twitter, at @jbrumley.