According to The New York Times’ Jim Tankersley, the Federal Reserve’s recent interest rate cut won’t immediately affect regular folks. However, if you’re heavily vested in Wells Fargo (NYSE:WFC), you might want to pay attention. As a member of the “big four” banks, Wells Fargo stock is an economic bellwether. And that’s why I find this juncture so worrying.

If you read the Times article here, on the surface, my concerns make me look like a negative Nancy. For example, in mid-July, WFC released its earnings result for the second quarter of 2019. and the print was quite impressive. Against a consensus per-share profitability target of $1.15, the bank produced an earnings per share of $1.30. Plus, Wells Fargo rang up $21.58 billion in revenue against the consensus estimate of $20.93 billion.

However, WFC stock absorbed a fierce tumble following the Q2 disclosure. A key reason why is the already low-interest rate environment. Obviously, one of the revenue channels for institutions like Wells Fargo stock is lending, but with deflated rates, this situation favors borrowers, not lenders.

In ideal circumstances, this is a time to raise interest rates. Real estate prices in several hot markets are blowing through the roof. Moreover, the unemployment rate is down at multi-year lows. Apparently, no need exists for a dovish monetary policy. Naturally, this dynamic should benefit Wells Fargo stock, along with peers JPMorgan Chase (NYSE:JPM), Citigroup (NYSE:C

) and Bank of America (NYSE:BAC).

But the Fed is moving in the opposite direction for seemingly understandable reasons: they want to avoid another massive recession by taking proactive measures. But looking at the financials for WFC stock, I’m not sure this is the right move.

Unspoken Headwind Impacting Wells Fargo Stock

Compared to the other big banks, Wells Fargo stock is incredibly disappointing. Over the trailing five-year period, shares are actually in the red. That pales in comparison to its peers.

For example, banking king JPM is up over 105%. Citigroup is up 48% while BofA has gained nearly 105%. Under this context, WFC stock looks almost shockingly bad. Supposedly, we have a ready explanation. Over the years, the Wells Fargo sparked a series of high-profile controversies.

On a side note, these issues of malfeasance are tragic. WFC used to have a very positive reputation.

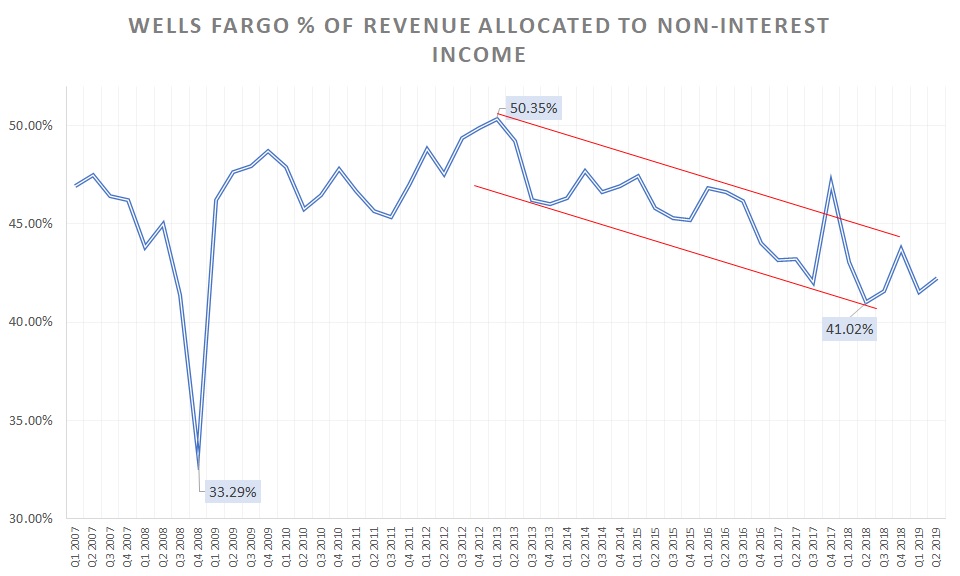

However, another possible explanation, one that isn’t discussed much, is the allocation of total WFC revenue that is non-interest income. This is the line segment that represents sales through activities like lending, advising, and consulting. In other words, they’re sales from actually doing something.

What’s problematic for WFC stock is that non-interest income relative to total revenue has largely declined since Q1 2013. Essentially, Wells Fargo and other big banks have produced the majority of their revenues passively.

Click to Enlarge

Moreover, we know that a low ratio of non-interest income represents an unhealthy economy. In Q4 2008, during the height of the financial panic, non-interest income relative to total revenue dropped to 33.3%.

Thankfully, the Fed, led at the time by chairman Ben Bernanke, was ready. Taking the lessons of the Great Depression at heart, Bernanke turned the monetary spigot loose. This drove confidence among the business class. Slowly but surely, the economy recovered under the Obama administration.

But the sticking point is that the economy didn’t recover substantively. The allocation of non-interest income peaked in Q1 2013 at 50.4%. From that point forward, sales from activities have taken a backseat to interest-driven income.

Wells Fargo Stock Is a “Wait and See” Play

A counterpoint to the above argument is that the decline in non-interest income appears to have hit a bottom. In Q2 2018, the allocation of non-interest income to revenue dropped to a multi-year low of 41%. Subsequent quarters featured a higher ratio, averaging 42.3% from Q3 2018 through Q2 2019.

Does this mean the business environment is improving, and that entrepreneurs are willing to take more risks? Perhaps. Also, it’s not completely out of the question that the Fed’s decision to cut rates would spark a borrowing rush. After all, this is a great time to buy a house if you can afford it.

Ultimately, though, I think Wells Fargo stock is a wait-and-see trade. Economies improve based on true, rational fundamentals, not monetary sleight of hand. Still, I’m willing to be proven wrong. I just need the data to be comfortable with WFC or its peers.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.