Robinhood (NASDAQ:HOOD) — the “people’s broker” — has been one of the most controversial IPOs of 2021. As the legend goes, Robin Hood and his Merry Men would jump out from hiding as nobles and dukes passed through the woods. The men would then rob the rich to give money to the poor. Similarly, the online broker Robinhood wants to empower everyday retail investors and level an unequal playing field. The message is simple. Deliver commission-free stock trading to the masses. Yet, somewhere along the way, the narrative around Robinhood stock changed — significantly.

Robinhood is now cast as the villain in the age-old story of Wall Street versus Main Street after revelations of hidden costs, poor execution and restrictive trading practices.

HOOD carried this polarizing narrative with it long before it went public last week at $38 per share. (Robinhood stock trades at $62 now, after rocketing over 24% and 30% intraday in its last two days of trading).

On one hand, the investing app birthed a revolution of direct stock investing, making even the most inexperienced of investors winning stock-pickers. The company is also largely responsible for the demise of passive exchange-traded fund (ETF) style investing that has dominated retail investing for the past decade. Bulls argue that a steady influx of young, hungry — mostly millennial — investors should power it further. They also believe that further growth of the company’s cryptocurrency trading operation (now well over 6 million users) could sustain double-digit growth for the next decade.

On the flip-side, critics accuse Robinhood of “gamifying” investing. And there are plenty of reasons to be concerned, ranging from the company’s head scratching $37 billion market cap, controversial trade execution practices and the potential for further trading restrictions.

Here’s a closer look at Robinhood’s controversial business model and a quick dive into the stock’s valuation.

Robinhood Stock: Quick and Easy

Robinhood is an online brokerage that offers commission-free trades of stocks, ETFs and cryptocurrency. Meanwhile, Robinhood Gold, a monthly paid subscription service, provides customers with additional features, including professional research and margin investing. The company estimates it had 22.5 million funded accounts as of the end of June 2021.

The company reports revenue in three segments:

- Transaction-based Revenue: Revenue from market makers for routing order flow for options, equities and cryptocurrencies. For options, the transaction price is on a per-contract basis. For equities, the price is based on the bid-ask spread. Transaction-based revenue is Robinhood’s largest operating segment, comprising roughly 75% of estimated 2021 revenues. It’s also the company’s largest lever for future revenue growth.

- Net Interest Revenue: Interest the company earns from securities lending, cash holdings and margin loans to users.

- Other Revenue: Revenue Robinhood earns from its Robinhood Gold subscription service as well as from fees charged to users to transfer accounts to other broker-dealers.

PFOF: The Goose that Laid the Golden Egg

Robinhood’s early claim-to-fame was a decision to not charge a fee for executing stock trades. This feature has since been copied by other brokers, including E*Trade and Schwab (NYSE:SCHW), among others. But, if a broker isn’t getting paid for orders, it has to make money somewhere. So, instead of getting paid directly by the people buying the shares, brokers sell their orders in bulk to market makers who then execute the trades. As a result, Robinhood, like many no-fee brokers, has instituted a controversial practice called Payment for Order Flow (PFOF), in which a brokerage firm receives rebates on trades routed through its clearing firm.

Here’s how it works. Robinhood, like other retail brokers, can internally cross trades between its own customers or send trades out to market makers like Citadel Securities, or Virtu Financial (NASDAQ:VIRT), which in turn pay Robinhood for sending them the order flow.

Although brokers are supposed to execute orders based on the current price on an exchange, PFOF allows a broker to skim a profit off of customer trades by offering a higher price than the “best” quote posted on the exchanges. Robinhood generated $687 million from such PFOF-related payments in 2020.

Game-Stopped?

Most of us have learned in some way or another that nothing in life is ever free. Still, it’s easy to understand why the lack of transparency surrounding PFOF has incensed retail investors. PFOF underscores a potential conflict of interest between brokers and their customers, as it implies they may not always be motivated to get the best possible prices for their customers. It’s not just the everyday people in ire. PFOF’s critics also include the country’s top market regulator, Securities and Exchange Commission (SEC) Chairman Gary Gensler. Some Democrats on Capitol Hill have also backed prohibiting payment for order flow. And PFOF is actually illegal in some countries, such as the U.K.

On the other hand, for the brokers themselves, PFOF is the gift that keeps on giving. Arguably, PFOF has been instrumental in attracting millions of new millennial investors to speculate in stocks. Robinhood’s products have became enmeshed in popular culture thanks to both the “stonks” movement and Reddit-driven stocks like Gamestop (NYSE:GME), AMC (NYSE:AMC) and Blackberry (NYSE:BB), which have gone from astronomical highs only to crash-and-burn unfortunate retail investors left holding the bag.

But Robinhood’s seemingly noble calling came into question on Jan. 28, when the company halted trading in Gamestop. In doing so, it prevented many retail investors from reaping profits. In February, the House Financial Services Committee summoned the main players involved in the meme-stock frenzy. Not surprisingly, their attention was centered on Robinhood’s potential misalignment with its customers.

Rep. Alexandria Ocasio-Cortez (D-NY) asked Robinhood CEO Vlad Tenev “[w]ould you commit to voluntarily pass on the proceeds from payment for order flow to Robinhood customers?” Tenev’s response? No.

“Robinhood is a for-profit business and needs to generate some revenue to pay for the costs of running … [the] business,” Tenev explained.

It’s Time for Robinhood to Buckle Down

Last month, Gensler said the SEC was reviewing payment for order flow. This fueled speculation that PFOF could be banned. While a ban wouldn’t destroy Robinhood’s business, it would mean the company would have to compensate for the loss of this revenue stream with a new revenue source. As a consequence, it would likely charge a commission on trades.

The combination of intense regulatory scrutiny and several class-action lawsuits caused Robinhood to buckle down by placing trading restrictions on purchase size and options contracts in select securities. The company has also steadily expanded its list of restricted stocks. It has since reversed some of its more restrictive policies, particularly around securities like GME. And adventurous investors should take note: short selling is not permitted on the platform.

The Bottom Line on Robinhood Stock

Whichever way the PFOF controversy shakes out, one thing is clear: Robinhood stock looks fairly valued at these levels.

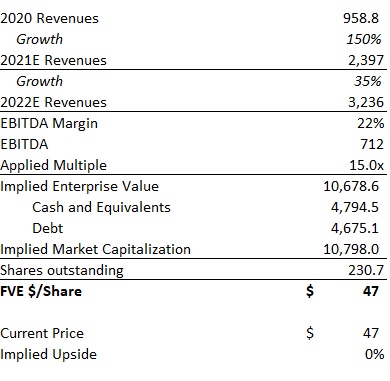

Here’s my quick back-of-the-envelope valuation analysis.

Click to Enlarge

Based on estimated 2022 revenues of $3.2 billion and an EBITDA margin of 22%, Robinhood would generate $712 million in EBITDA in 2022. Applying a 15x multiple to estimated EBITDA implies an enterprise value of $10.7 billion for HOOD, or a fair value estimate of $47 for the stock (based on the latest balance sheet).

That’s 25% below the shares’ current price ($62 as of this writing) and well above the IPO price of $38. As a comparison, Fidelity (NYSE:FIS) and SCHW trade at EV/EBITDA multiples of 18x and 12x, respectively.

Putting all of this together, I suggest that prospective Robinhood stock investors stay on the sidelines for now.

Reader Question of the Week: What About the ‘Damn’ Cars?

From the article Lucid Motors Has the Guts. But CCIV Stock Hasn’t Earned the Glory.

Hope all is well! I’m still HODL’in Lucid (NASDAQ:LCID) for dear life hahaha. I have a question. Right now one of the biggest knocks on Lucid is that it hasn’t delivered a damn car yet. Let’s say they start doing that and start delivering. That will be one of the biggest concerns that will be put to bed. What will the next biggest negative sentiment be?

Hi! LCID stock has indeed sputtered since its public debut, and is currently trading sideways around $23. The next catalyst: firing up that $700 million manufacturing plant in Casa Grande, Arizona, and producing cars in volume.

But just because they turn the lights on doesn’t necessarily mean Lucid will ramp to commercial volumes without any hiccups. Remember Elon’s words about “[eating] a lot of glass” and “manufacturing hell.” Tesla isn’t the only EV manufacturer to go nearly bankrupt while trying to scale. The same challenges plagued Nio (NYSE:NIO). LCID has the advantage of a $4 billion chunk of cash burning a hole in its pocket (thanks to retail investors who bought into the company’s promise). But there’s meaningful risk to the company’s ability to ramp up this year. I see meaningful downside risk to the stock if the company ships anything less than than its previous target, which calls for 577 Lucid Airs.

Then there’s the recent confirmation in Lucid’s latest SEC filing of its intention to build a manufacturing plant in Saudi Arabia, which I discussed some time ago. How will Lucid plan to fund that build? It’s certainly no secret that Saudi Arabia lacks the manufacturing footprint necessary to build automobiles at scale. The country has been trying to persuade an automaker to build an assembly plant on its home turf since a fizzled deal with Jaguar Land Rover, owned by India’s Tata Group (NYSE:TTM). Given the Saudi’s limited resources, this will certainly be an expensive undertaking.

Your comments and feedback are always welcome. Let’s continue the discussion. Email me at jmakris@investorplace.com.

Disclosure: On the date of publication, Joanna Makris did not have (either directly or indirectly) any positions in the securities mentioned in this article.

Click here to track her top trades of the week, where she sheds light on market psychology and momentum, while leveraging her deep knowledge of fundamental analysis to deliver event-driven trading strategies.