Growing your portfolio at 20% per year with high CAGR stocks is difficult. Indeed, most hedge funds fail to come close to even 10%. The Warren Buffett Portfolio obtained a 9.91% compound annual return, with a 13.66% standard deviation, in the last 30 years. This is better than the S&P 500 but below that of the Nasdaq. Anyone growing their portfolio at 20% per year would have to significantly outperform the Nasdaq. It would also mean doubling your money every 3.6 years.

However, such a task isn’t impossible. I have highlighted the above metrics to clarify that even if you invest in very good companies, it would be difficult to consistently achieve 20% annual portfolio growth. You also need to invest in more than just growth stocks for a well-rounded portfolio.

Regardless, there are some stocks that can help you achieve those returns. These quality growth stocks are likely to compound around 20% annually going forward, as long as the market holds up their premium valuations. A portfolio consisting only of these seven stocks will likely yield significant gains. That’s as long as the rally continues.

I would still recommend you invest in defensive and dividend stocks alongside high CAGR stocks for ballast. That said, investors looking for outsized gains may want to dive into these stocks right now!

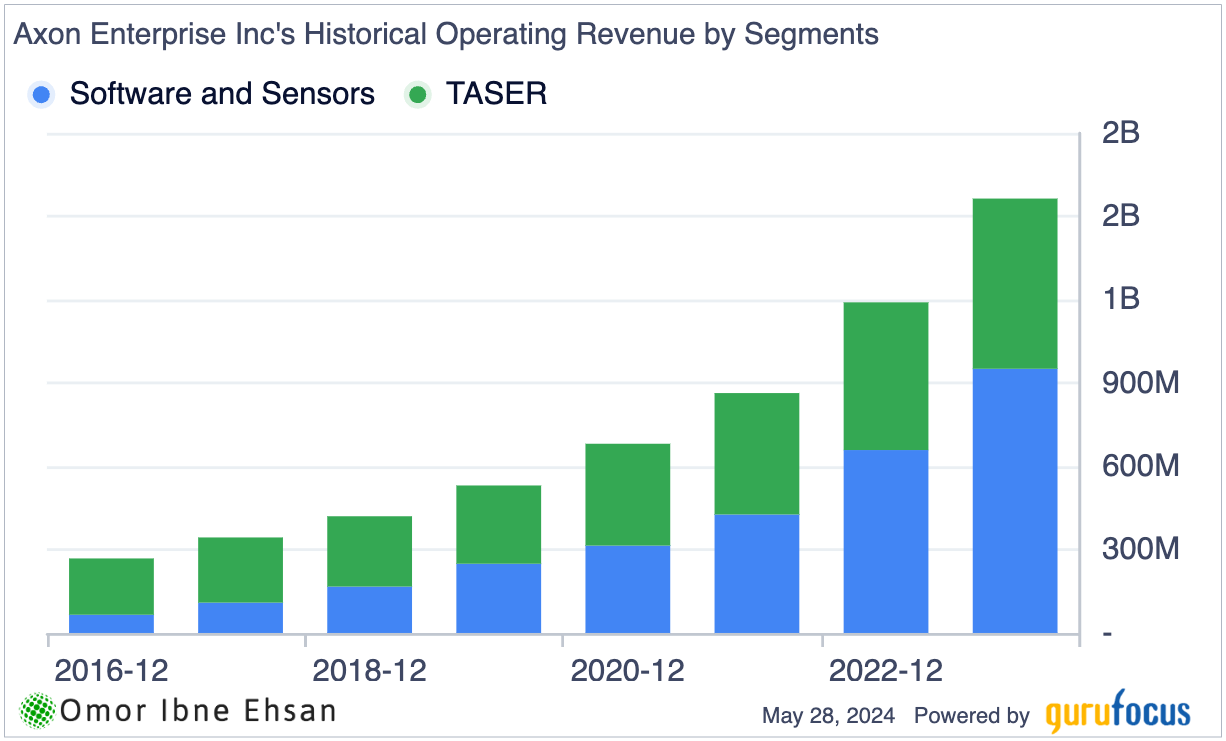

Axon Enterprise (AXON)

Axon Enterprise (NASDAQ:AXON) makes equipment to support law enforcement and public safety personnel. Its tasers are very well-known, and as social disorder increases, I see much more demand from law enforcement agencies in the coming years. Looking at the stock’s recent performance, and it becomes clear it is one of the best high CAGR stocks to buy right now.

Click to Enlarge

In fact, the demand for its products so far has been stellar. I’m very optimistic about where Axon is headed after the company reported their strong financial results for Q1 2024. Revenue increased 34% to $461 million, blowing past analysts’ estimates by more than $19 million. Earnings per share came in at $1.15, which also significantly exceeded projections.

Beyond the impressive headline numbers, I’m excited about some of Axon’s transformational projects that could truly be game-changers in their industry. Their planned acquisition of Dedrone aims to enable law enforcement agencies to deploy drones for emergency response in a big way while overcoming current limitations set by the FAA.

Additionally, Axon’s new AI-assisted software, Draft One, also shows tremendous potential to save officers around 15 hours each week on paperwork and administrative tasks. That freed-up time could be reallocated to valuable community engagement and professional development work.

I think Axon has the potential for some truly massive growth over the long-term. Axon appears well-positioned to deliver strong returns for investors seeking high annual returns of 20% or more. Analysts expect the top and bottom lines to grow around 20% annually over the coming years. So as long as the market premium holds, AXON stock should perform just fine.

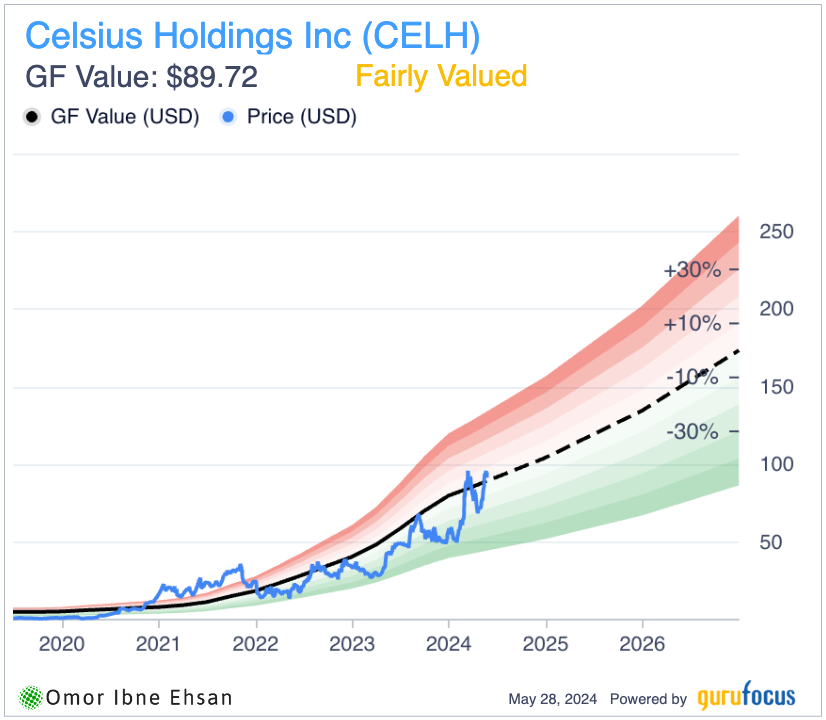

Celsius Holdings (CELH)

Celsius Holdings (NASDAQ:CELH) is an up-and-coming beverage company. This company also reported outstanding first-quarter results, with revenue soaring 37% year-over-year to a record $355.7 million. Notably, Celsius is among the key contributors to the impressive 47% growth seen in the entire energy drink segment. That’s because the company’s market share climbed to 11.5%, up a full point.

While temporary fluctuations at their largest distributor created some noise, the underlying demand pattern remains robust. Celsius is executing and innovating well, with promising new introductions like Galaxy Vibe and the CELSIUS Essentials line gaining traction. Management also highlighted that they expect their best product placement gains once spring resets fully roll out to stores.

In my view, Celsius has significant potential for growth ahead as the company works towards its ambitious goal of becoming the world’s top energy drink brand. That will take time to materialize, but you can ride the growth in the meantime. You’re definitely paying a premium for this stock, but as long as the company executes and Wall Street holds up the premium, this is a stock that can deliver 20%-plus annual gains.

Click to Enlarge

Howmet Aerospace (HWM)

Howmet Aerospace (NYSE:HWM) manufactures advanced solutions for the aerospace and transportation industries. This stock has been one of the most flashiest names in the market recently. Notably, HWM stock is up by nearly 95% in the past year, and I think it fits the bill among high CAGR stocks with the potential to see this trend continue.

I’m very optimistic about Howmet’s future prospects. The company’s revenue hit a record high of $1.82 billion, up an impressive 14% from last year. The remarkable 23% growth in the company’s commercial aerospace segment was especially notable. Private and commercial aerospace are areas that are booming, and will continue to boom, due to Trump’s tax cuts, which allow these jets to be written off as business expenses.

But what really caught my eye was the stunning 21% jump in EBITDA and 150 basis point margin expansion seen this past quarter. This company seems to be performing exceptionally well across the board.

Management has done a flawless job, with 12 straight quarters of robust gains in aerospace supplemented by smart decisions to increase their transportation market share. The company’s financial position is incredibly strong, with the ratio of their net debt to EBITDA at a record low of only 2 to 1. It’s clear that Howmet’s excellent operational execution also translates to the bottom line, as earnings per share grew 36%. The company is also deleveraging fast and could become a cash cow.

Given the outstanding first-quarter results and various tailwinds from the rebound in air travel, I believe Howmet is well-positioned to deliver 20% annual returns.

PDD Holdings (PDD)

PDD Holdings (NASDAQ:PDD) operates a leading online marketplace in China and abroad. You likely have heard of Temu and their bargain prices. Temu is now one of the most downloaded apps on the App Store.

I’m very impressed by the company’s strong results reported last quarter, with revenue increasing an incredible 131% over the same period last year to reach 86.8 billion yuan ($11.99 billion), handily surpassing analysts’ projections by $1.41 billion. This is definitely one of the most high CAGR stocks in the market right now. Analysts are bullish in their near-term projections, too.

PDD is wisely dedicating resources to offering more selection to shoppers, partnering with top global brands, and providing merchants with digital tools to help lower costs. This balanced approach should support continued growth as Chinese consumers increasingly demand higher-end goods.

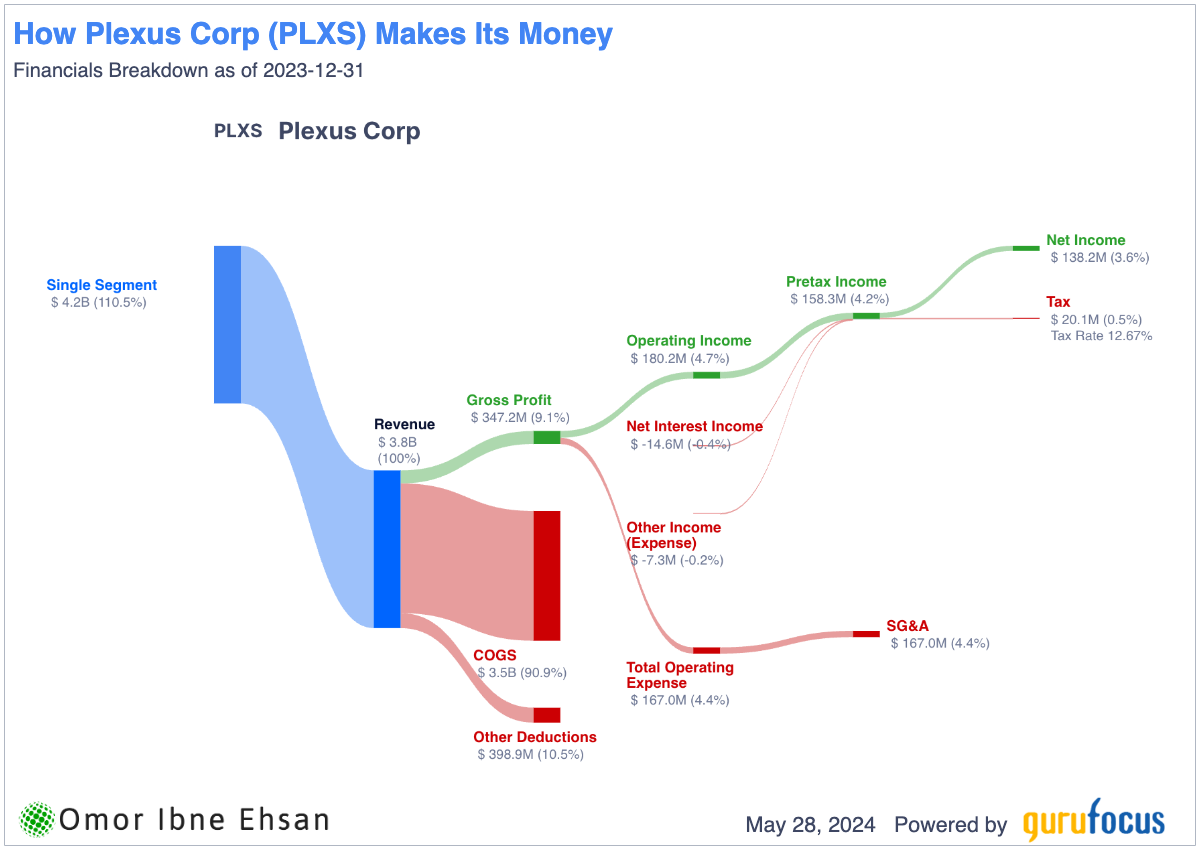

Plexus (PLXS)

Plexus Corp. (NASDAQ:PLXS) provides design, manufacturing, and aftermarket services to companies in the industrial, healthcare/life sciences, aerospace/defense, and communications markets. This stock has consistently delivered returns that are around 20% annually on average. In fact, the stock is up over 128% over the past five years, and I think it is possible for Plexus to repeat this performance.

The company’s fiscal Q2 results were impressive, with Plexus reporting revenue of $967 million and non-GAAP EPS of 94 cents that beat expectations. Management’s go-to-market strategy is clearly paying off, with $255 million in new program wins signaling robust demand and market share gains.

The company now seems focused on expanding margins, with a target of 5.5% GAAP operating margin (over 6% non-GAAP) by late fiscal 2025. Initiatives to align operations and control costs are taking hold. Plexus also flexed its cash generation muscle this quarter, producing $65 million in free cash flow. I see lots of room for margins to expand.

Click to Enlarge

Given management’s increased fiscal 2024 FCF forecast of $100 million and plans to return excess cash to shareholders, I believe Plexus is well-positioned to deliver outsized returns. This under-the-radar mid-cap is worth a closer look for growth-oriented portfolios.

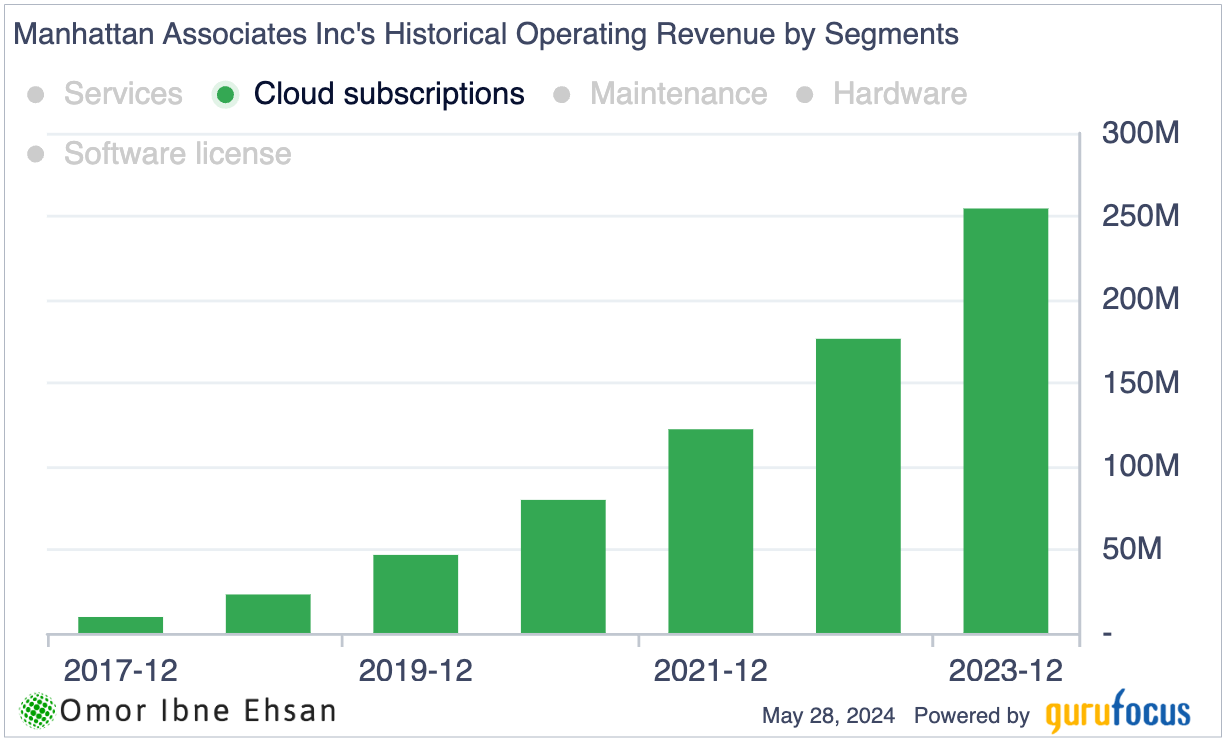

Manhattan Associates (MANH)

Manhattan Associates (NASDAQ:MANH) provides cloud-based supply chain and online shopping solutions to many companies. The company is off to a great start in 2024, with first-quarter revenue growing 15% to $255 million and adjusted earnings per share surging 29% to $1.03, both beating analyst estimates. I’m especially impressed by the 36% growth in cloud revenue and 14% growth in services revenue, which helped drive the higher-than-expected total revenue number this past quarter. The top line beat expectations by 4.6%, while earnings beat by 18.4%.

Even with uncertainty in the global economy, Manhattan’s underlying business fundamentals remain strong. The company’s backlog increased 31% to over $1.5 billion due to increasing demand for its cloud solutions.

Click to Enlarge

Manhattan appears well-positioned for sustained growth with a full pipeline of potential new projects, over 100 implementations completed in the first quarter, and continued investment in innovation and hiring. This stock is also down around 14% from its March peak, so I see big upside in the coming quarters as it makes a recovery.

Booking Holdings (BKNG)

Even though we may no longer be in a travel boom, don’t count out travel stocks just yet. Booking Holdings (NASDAQ:BKNG) operates popular travel websites such as Booking.com, Priceline, and Kayak. It had a very strong start to the year. In the first quarter, revenue grew 17% to reach $4.4 billion compared to last year’s period. Adjusted EBITDA surged even more, with a 53% increase to $900 million. Furthermore, the company beat earnings per share expectations by 43.66%, and revenue beat estimates by 3.74%.

The stock is up 129% over the past five years, and you also get a 0.9% dividend yield here. Analysts expect around 20% annual EPS growth over the next five years. If this company continues to beat estimates like this, I expect BKNG stock to deliver well over 20% gains annually.

Booking.com recently saw a huge jump in the number of “connected transactions,” which are when travelers book multiple travel needs like flights and hotels during the same trip. This connected trip option is still new, but is gaining popularity quickly.

With summer travel looking healthy so far and the connected trip feature helping to boost revenue, I believe Booking Holdings is well-positioned for a good year in 2024. Room bookings over the next few months may slow down some due to issues in the Middle East and travelers booking closer to their travel dates. However, as a leader in the market with improved profitability and share repurchases boosting earnings per share, I think any dips in the stock price present a buying opportunity for this high-quality growth stock.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.