We are officially in the middle of Q2 with the start of May, and it is also the earnings season for companies reporting their Q1 figures. Even though the market right now is not at its best, with bearish sentiments casting a dark cloud over Wall Street, I believe this is a good time to establish positions in some sturdy long-term stocks that can deliver “exponential” gains.

These stocks have grown along with the broader economy, and some have consistently beaten the S&P 500‘s returns, proving their mettle as steady compounders. As the old saying goes, “Time in the market is better than timing the market.” Any portfolio should contain at least a few of these stocks in their core to add ballast and significant upside potential in the long run. While the bears may continue to growl in the near term, these resilient picks have the fundamental strength to weather the storm and emerge victorious.

Of course, the bearishness could cause some of these stocks to decline in the near term, as they often get caught in the undertow of market sell-offs. However, if you are looking to hold for the long run and have the patience to let the compounding work its magic, all of these long-term stocks are great buys right now at discounted valuations.

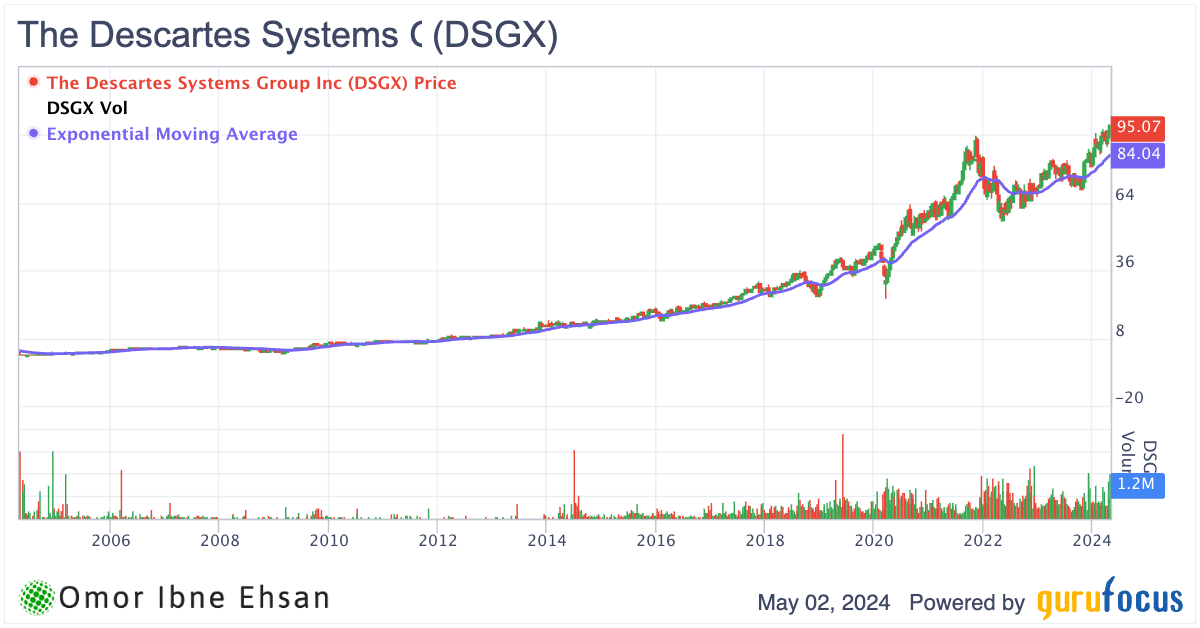

Descartes Systems Group (DSGX)

Descartes Systems (NASDAQ:DSGX) is a Canadian company specializing in logistics software, supply chain management software, and cloud-based services for logistics businesses. Even though the supply chain took many hits in the past few years and has been volatile, this company has continued to deliver consistently in the long run. It did have short-term selloffs in 2021, along with the broader market, but the long-term trend here has been stellar.

Click to Enlarge

The company provides software to the logistics industry, so it generates revenue from the booming logistics industry while being cushioned from direct shocks in the industry.

The stock is up 132% in the past year. It is one of the safest stocks you can buy, as it has 46 times more cash than debt, and its Altman-Z score of 22.2 puts it firmly in the “safe” category. Moreover, it had a 20.2% net margin last year, which is better than 91.5% of industry peers. The company has a growing cash pile, and I expect it to pay dividends in the coming years, further sweetening the pot for long-term investors.

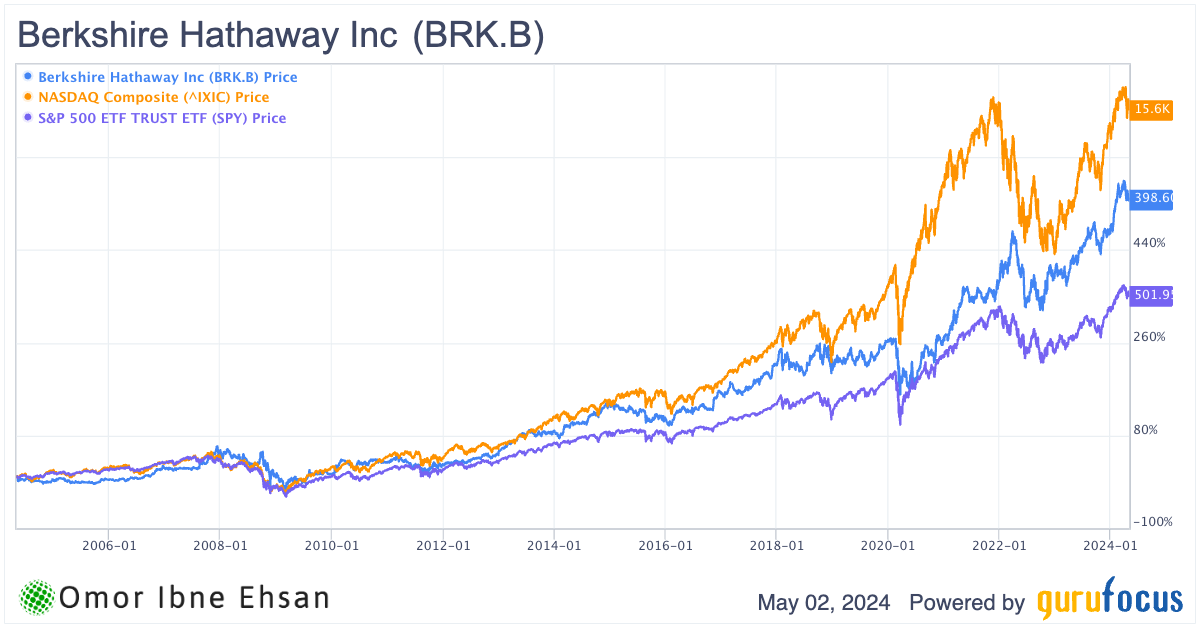

Berkshire Hathaway (BRK-A, BRK-B)

Berkshire Hathaway (NYSE:BRK-A, NYSE:BRK-B) is a no-brainer company, and I think it should be one of your biggest core holdings by far, if not the biggest. This company’s biggest asset is Warren Buffett, of course. However, even if he were to not be with us in the coming years, I expect Berkshire to continue performing well. It has been the most stable major public holding company and has outperformed most of its peers by significant margins, including outperforming the S&P 500.

Click to Enlarge

Charlie Munger’s passing did not impact the stock as much as I previously thought it would, and I also believe that the portfolio and wisdom left by Warren Buffett would continue to make this business shine.

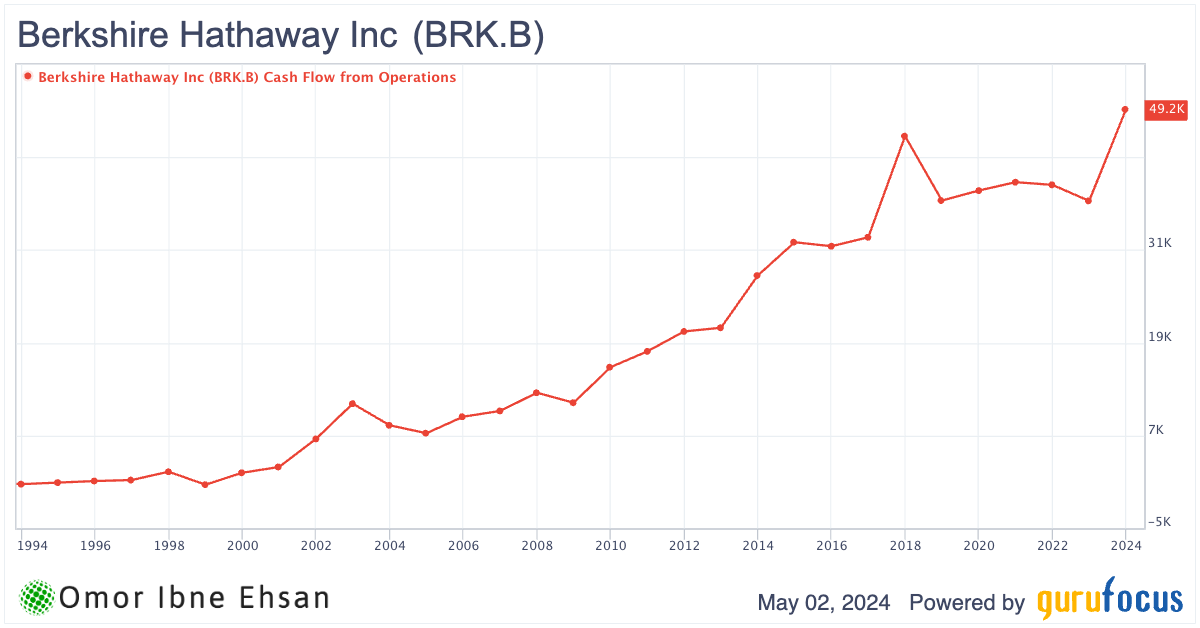

Since Buffett is still alive, Berkshire has exceptional confidence in the market due to his reputation. This is simply an S-tier stock that you can comfortably hold and see it compound over the years. The cash flow here makes it one of the best long-term stocks to hold.

Click to Enlarge

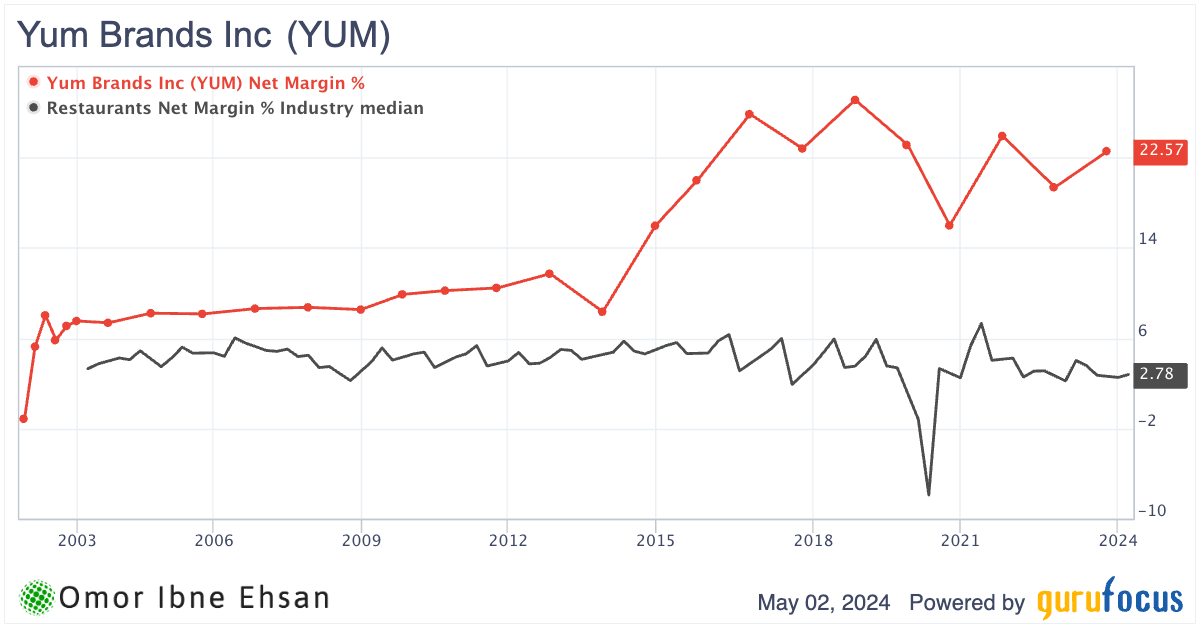

Yum! Brands (YUM)

In my articles, I often discuss McDonald’s (NYSE:MCD) as one of the best compounders that are also recession-resistant. One company that comes pretty close is Yum Brands (NYSE:YUM), which owns KFC, Pizza Hut, Taco Bell, and The Habit Burger Grill, among others. This company has been delivering solid returns decade after decade, and I also think it has similar upside potential.

The debt here is $12 billion compared to $512 million in cash, so it has been affected by rate hikes. However, margins have held up, and the company has continued to post solid earnings. The net margin was 22.6% last year, which is better than 97% of restaurant companies.

Click to Enlarge

Moreover, its 3-year revenue growth rate remained above double digits at 10.5%. The restaurant brands owned by this company are unlikely to go away anytime soon, making Yum Brands a tasty addition to any portfolio centered around long-term stocks.

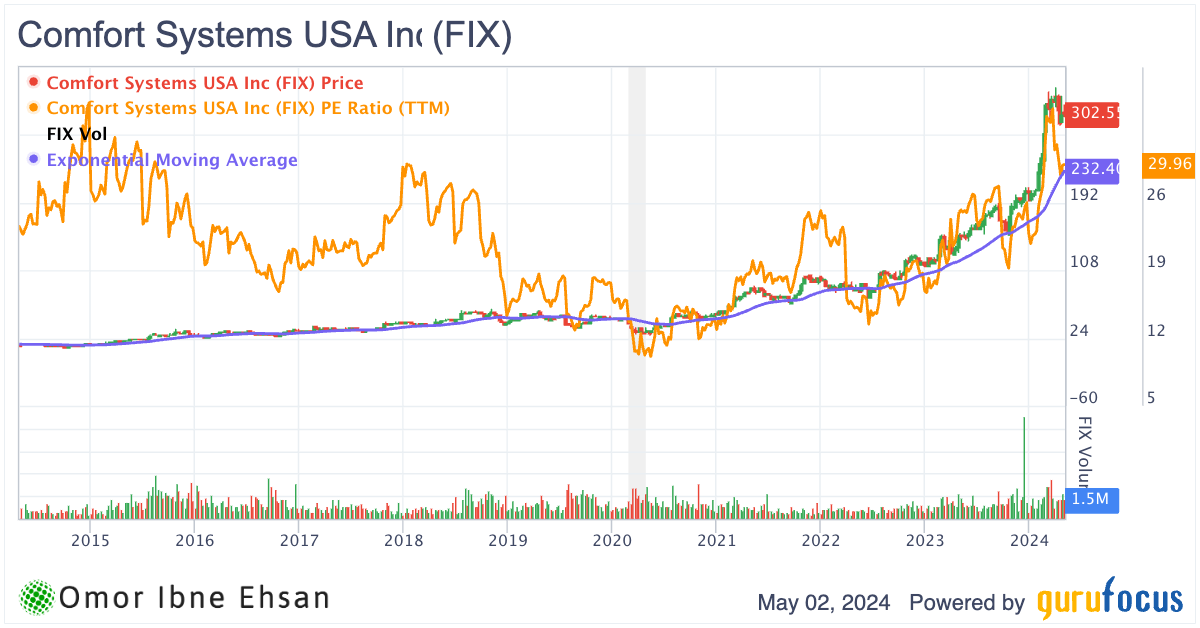

Comfort Systems (FIX)

HVAC stocks have been booming in recent quarters due to persistent heat waves across the world. If we see a heat wave in the U.S. similar to the one we saw last year, I believe investors who have their money in air conditioning companies will be laughing their way to the bank. As the old saying goes, “Make hay while the sun shines,” and Comfort Systems (NYSE:FIX) is well-positioned to capitalize on the sweltering conditions.

Of course, I don’t expect a multibagger upside from these well-established companies, but they can deliver 30-40% in gains this year if it is particularly hot. The performance here has been stellar already. It has been up 472% in the past five years and almost 100% in the past year. I think it can perform even better in the summer.

Click to Enlarge

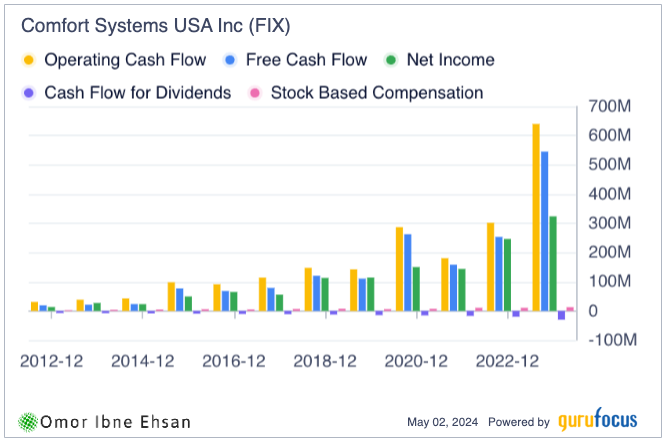

The company beat EPS and revenue by nearly 30% and 5%, respectively, in its Q1 report. It also raised its quarterly dividend last week to 30 cents per share. Operating cash flow more than doubled from $302 million to $640 million from 2022 to 2023. Definitely one of the best long-term stocks!

Click to Enlarge

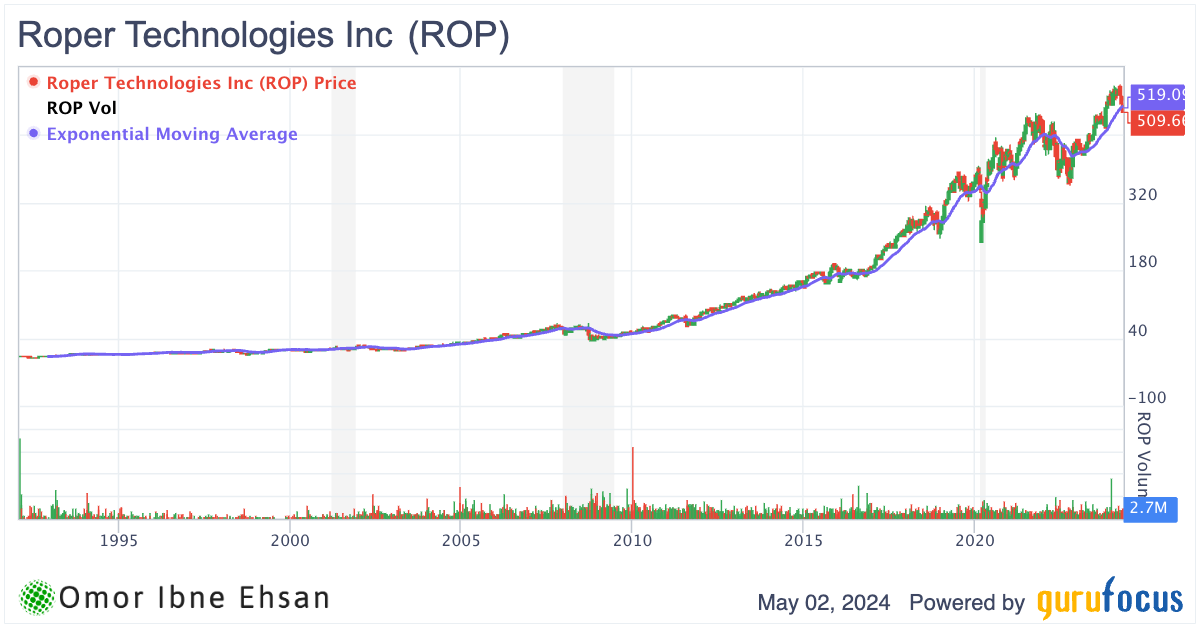

Roper Technologies (ROP)

Roper (NASDAQ:ROP) manufactures and distributes industrial equipment. It is a very well-diversified business that has its hands on multiple industries. Roper also has shifted its focus to vertical SaaS businesses, resulting in higher margins and more predictable revenue.

Click to Enlarge

The biggest windfall for the company has been the infrastructure spending and onshoring trends. Roper has seen significant growth in the post-COVID era due to this. EBITDA has recovered from $1.57 billion in 2020 to $2.67 billion in 2023, and stimulus and spending for infrastructure have seen no end in sight.

The 3-year EPS growth (minus non-recurring items) is almost 38% annually on average. Analysts expect continuous EPS growth over the next decade from an estimated $18.2 in 2024 to $67 in 2033, which should lead to hefty compounding of its stock.

Woodward (WWD)

Woodward (NASDAQ:WWD) provides control system components for aircraft engines, industrial engines and turbines, power generation, and similar industrial equipment. As I have said before, on-shoring trends have been fueling infrastructure companies, and industrial companies have also been benefiting massively. In my opinion, Woodward is well-positioned to ride this wave of domestic manufacturing and infrastructure investment.

Click to Enlarge

Woodward finally surpassed its 2019 sales peak with a record $2.9 billion in revenue in 2023. However, margins are yet to catch up, but I am sure they will this year, as EPS is expected to increase by 42% along with 13.6% sales growth.

Woodward also had its price target raised to $200 from $182 at Deutsche Bank and raised to $200 from $191 at UBS. Both maintained a “Buy” rating on the stock, which is up a solid 46% in the past year. It also beat Q1 top-line estimates by 3.3% and EPS estimates by 21.1%, and I expect it to continue beating sales estimates, as it has done so since Q4 2022.

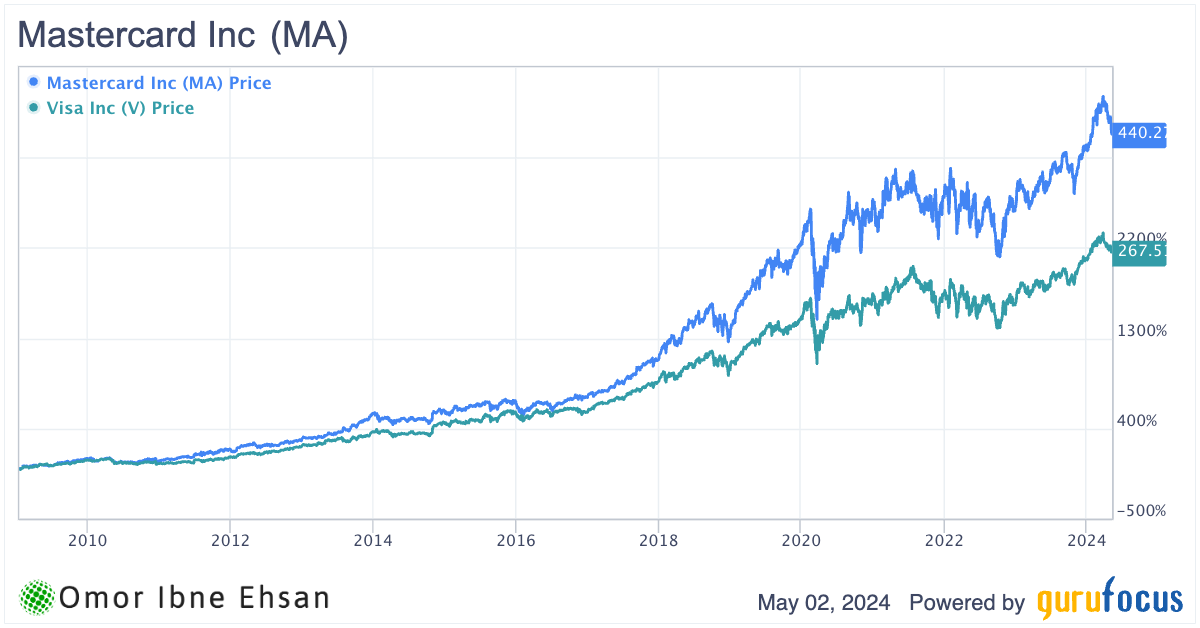

Mastercard (MA)

Mastercard (NYSE:MA) is a well-known business, and it shouldn’t take much explaining as to why this company is seeing consistent and stable growth that is “exponential.” It has been growing along with the economy for years. That’s because both Mastercard and Visa (NYSE:V) have an extremely profitable duopoly. Mastercard’s dominance among the two has remained steadfast.

Click to Enlarge

Mastercard had a staggering net margin of 44% last year, which was better than 82% of its peers. The company also had a solid cash position of $9.2 billion, and it benefits no matter the macroeconomic environment as long as people make transactions. Mastercard benefits from high interest rates when rates are high, and it also benefits from the increased transaction volumes when rates are cut and people start spending again.

It might be a boring pick for many, but in my opinion, it is an essential one that you should hold and let it compound, as it is a true “cash cow.”

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.