The recent carry trade scare sent Japanese stocks into a tailspin, and the contagion spread to other markets faster than a juicy rumor in a high school cafeteria. Even stocks that were already in correction mode got hammered even harder. Some analysts warn that the carry trade debacle could just be the tip of the iceberg for stocks to sell.

As if that wasn’t enough to give investors heartburn, the macro picture also looks pretty grim. All the usual recession red flags are waving – the inverted yield curve, rising unemployment, and now the ominous-sounding Sahm indicator. You don’t have to be an economist to read the writing on the wall.

In times like these, taking a hard look at your portfolio and considering trimming some of your riskier positions is prudent. High-risk, high-reward stocks can be exciting when the market is soaring, but they can also be a one-way ticket to Painsville when things go south. I’m not saying abandon them entirely, but it’s a good idea to dial back your exposure a bit.

Tech stocks, in particular, could be in for a world of hurt. They’ve had an incredible run over the past two years. However, if the market really takes a nosedive, tech could bear the brunt of it, just as they have contributed to most of its rally.

As such, I believe now is a good time to consider selling these seven tech stocks before the potential 2024 tech selloff worsens.

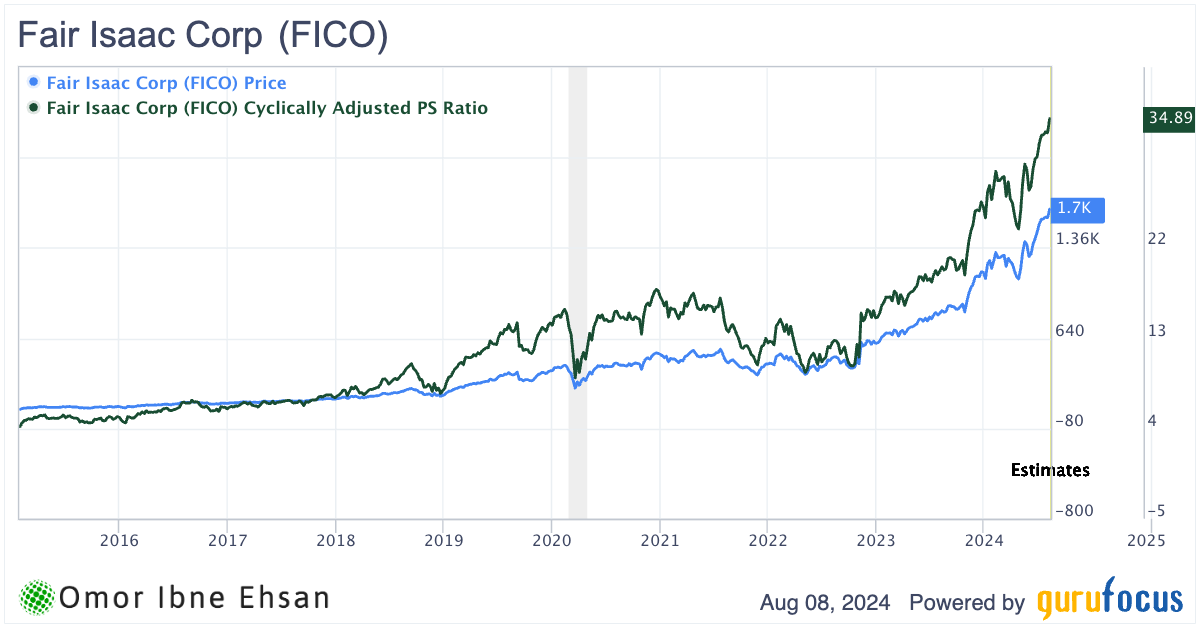

Fair Isaac Corporation (FICO)

Fair Isaac Corporation (NYSE:FICO) develops analytic, software, and data management products that enable businesses to automate and improve decisions. The company recently reported mixed Q3 2024 results, with revenue growing 12% year-over-year to $448 million but EPS missing expectations by 7 cents.

While FICO is thriving in the booming data analytics industry, I believe now is the time to take profits and sell the stock before the tech selloff worsens. Shares have skyrocketed 95% over the past year and an eye-popping 357% in the last five years, trading at nosebleed valuations of nearly 24x forward sales and 70x forward earnings. Its cyclically adjusted price-sales ratio is at its highest ever.

Click to Enlarge

You’d think those multiples would be justified by explosive growth, but analysts only expect around 13% annual revenue growth and 20% EPS growth going forward. That’s simply not enough to warrant such a premium price tag, in my view.

With recession fears mounting and interest rates still elevated, I worry that Wall Street will sour on pricey tech stocks like FICO in the coming months. It might be better to lock in your gains now before market sentiment potentially shifts to risk-off mode. The risk/reward is just not favorable at these levels, putting it among stocks to sell.

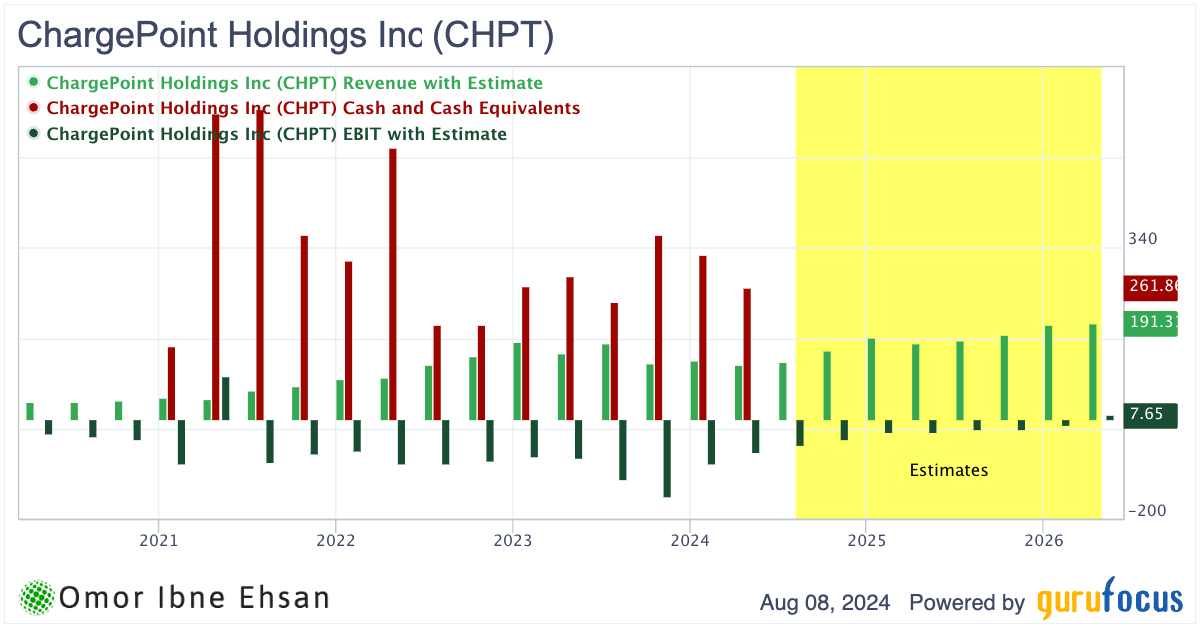

ChargePoint Holdings (CHPT)

ChargePoint (NYSE:CHPT) provides electric vehicle charging solutions, but the company has been struggling mightily lately. Even before the recent tech selloffs, ChargePoint was facing major headwinds, reporting an 18% year-over-year revenue decline to $107 million and widening losses in its latest quarter.

I believe the ongoing tech rout could greatly exacerbate ChargePoint’s dire situation. The entire EV sector has been sliding over the past two years as high interest rates weigh on demand. Bigger players like Tesla (NASDAQ:TSLA) are already eating ChargePoint’s lunch, and the company is being forced to dilute its stock to keep the lights on.

Even if rates are drastically cut, I think ChargePoint’s losses are simply too steep to overcome anytime soon. A recovery in the EV market will likely be prolonged, and a potential Trump administration could make matters even worse for the industry.

Click to Enlarge

And if the cash balance doesn’t go to zero until analysts think it hits profitability, the sales growth would be too sluggish to maintain the current premium.

In my view, you should steer clear of this sinking ship.

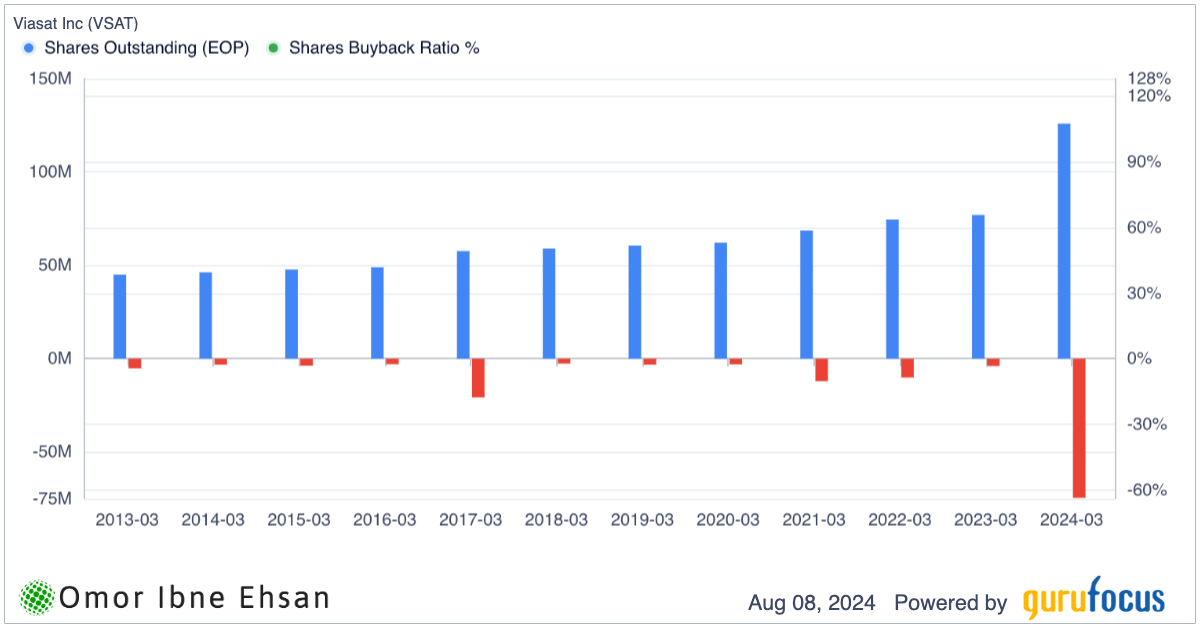

Viasat (VSAT)

It seems like Elon Musk is eating everyone’s lunch these days, and Viasat (NASDAQ:VSAT) is no exception. Despite Viasat’s best efforts, I believe the writing is on the wall – unless they can pivot to a completely new business model, bankruptcy may be inevitable. After all, why would anyone choose Viasat’s sluggish, high-latency service when Starlink offers a superior alternative?

Viasat’s most recent earnings report paints a bleak picture, with revenue growth expected to remain in the low single digits for the foreseeable future. However, I suspect even those modest projections are overly optimistic. As Starlink continues to scale and Amazon (NASDAQ:AMZN) prepares to enter the fray, Viasat’s market share will likely erode faster than anticipated, potentially pushing sales growth into negative territory.

In addition, the dilutive track record is pretty concerning.

Click to Enlarge

With the tech sector already in the midst of a major selloff, Viasat’s precarious position looks even more dire. Unless management can pull off a miracle, I fear this once-promising company may not survive the coming storm for stocks to sell.

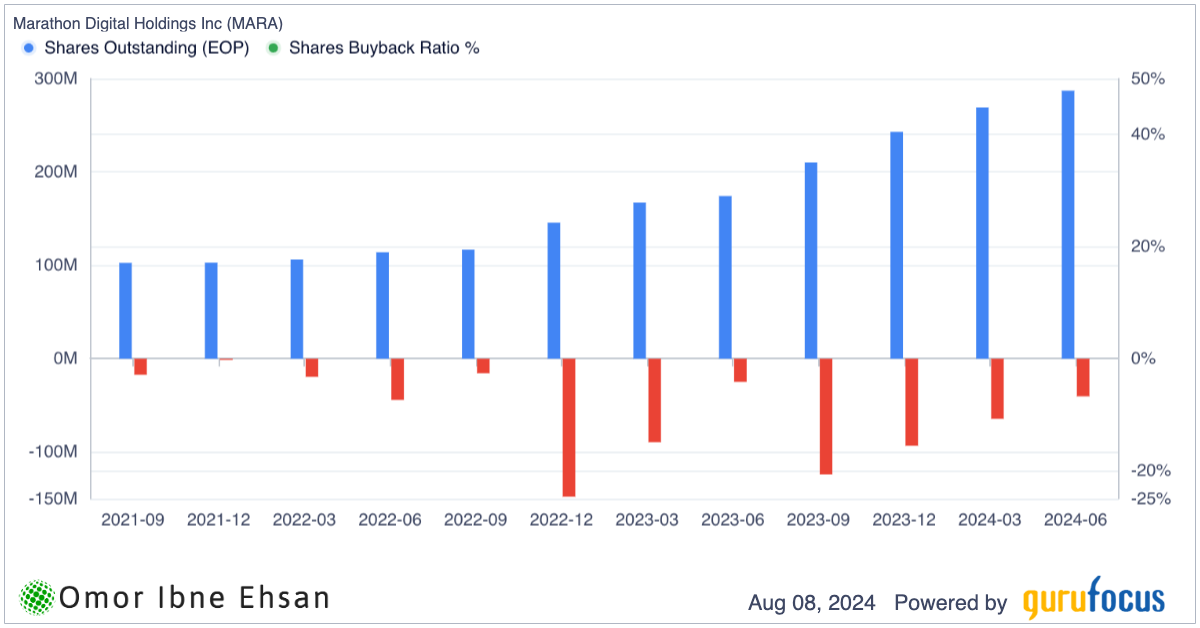

Marathon Digital (MARA)

Marathon Digital Holdings (NASDAQ:MARA) operates as a digital asset technology company that mines cryptocurrencies, primarily Bitcoin (BTC-USD). The company has been struggling lately, with its recent Q2 2024 earnings missing expectations and showing a significant net loss of $200 million, largely due to lower Bitcoin production and the decreased value of its digital assets.

Bitcoin mining businesses have been a major letdown in the current cycle. Sure, Bitcoin’s price more than doubled from its low point in the last crypto winter, but the rally happened well before the halving event that slashed mining rewards in half. Miners had years to prepare for this, yet they’re still posting massive losses and can’t seem to mine Bitcoin profitably.

Now, some folks think Bitcoin’s price could keep climbing, but I’m not convinced. We haven’t seen how Bitcoin will fare during a serious recession, and its performance is increasingly tied to the broader market. With a major tech downturn looming, I think Bitcoin could be in for a rough ride – and that spells trouble for Marathon Digital. The crushing dilution also makes a long-term position in MARA untenable.

Click to Enlarge

I’d steer clear.

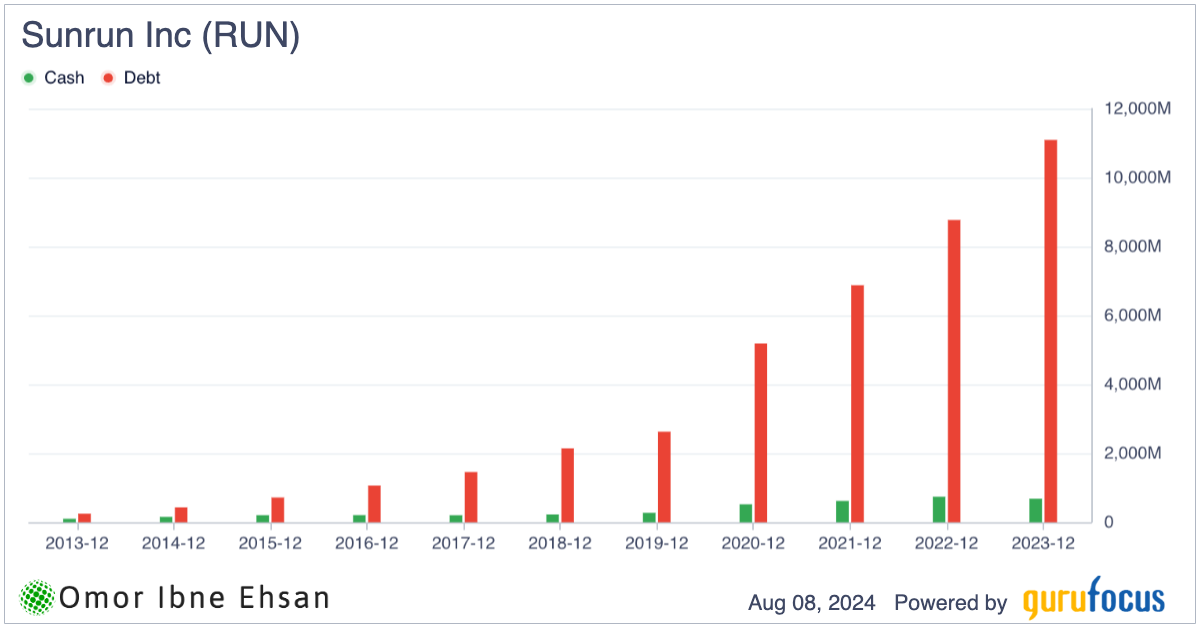

Sunrun (RUN)

While some solar stocks have surprisingly weathered rising interest rates and market volatility, Sunrun (NASDAQ:RUN) has been delivering the opposite performance. The company reported an 11% year-over-year revenue decline in Q2 2024, and analysts don’t expect it to achieve consistent profitability until at least 2028. I’m skeptical that Sunrun has the cash reserves to sustain itself that long. The debt-powered growth has now turned into Sunrun’s main cause for concern after interest rate hikes.

Click to Enlarge

Looking ahead, Sunrun’s projected sales growth also appears lackluster. As I mentioned earlier in this article, a potential Trump presidency could further dampen the outlook for stocks like Sunrun. Jefferies analyst Dushyant Ailani lowered his price target on RUN from $32 to $26, citing concerns about the company’s path to profitability.

Given these risks and uncertainties, I believe it’s prudent to consider removing Sunrun from your portfolio.

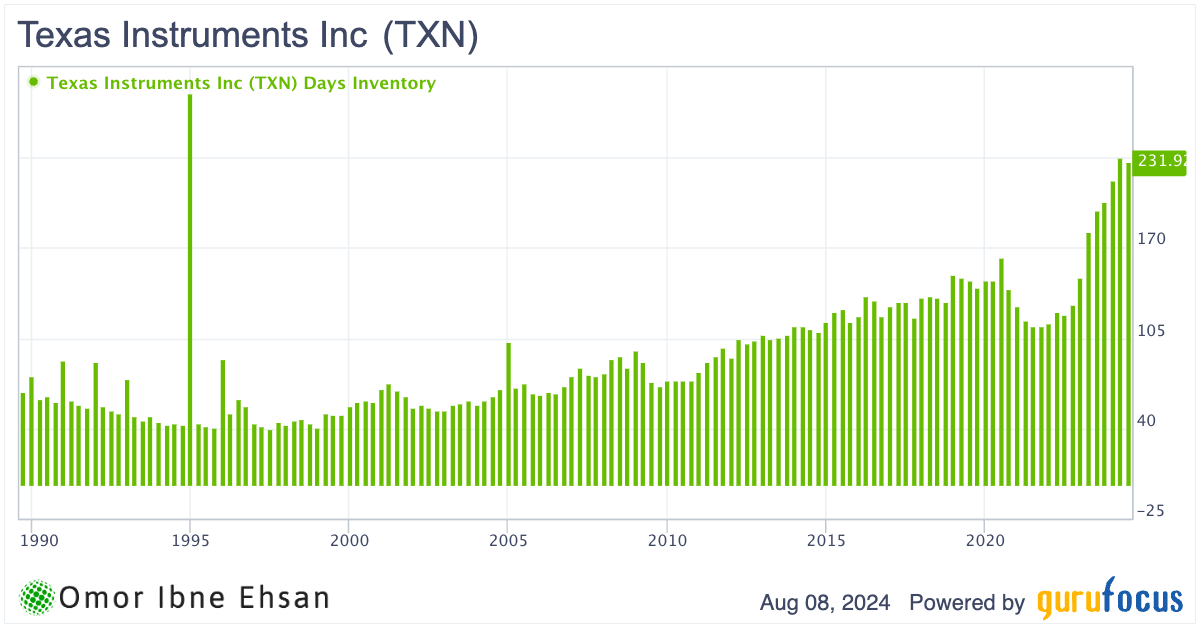

Texas Instruments (TXN)

Texas Instruments (NASDAQ:TXN) designs, manufactures, tests, and sells analog and embedded semiconductors. The company has been navigating a challenging environment, with revenue declining 16% year-over-year in Q2 2024 to $3.82 billion, marking the seventh consecutive quarter of sales and profit declines. While TI beat earnings estimates by $0.02 and matched on revenue, the cyclical slump in demand is expected to persist for at least another quarter.

I’ve long considered TI one of the best semiconductor stocks, and I believe its long-term prospects remain bright, given its strong position in the crucial industrial and automotive markets. However, the recent Q2 report gives me pause in the near term. Missing earnings estimates by even a small amount seem out of character when most peers have been handily exceeding expectations. The recent increase in inventory is also concerning.

Click to Enlarge

With TI trading at a lofty 11 times forward sales and analysts projecting low double-digit growth after this year’s sales decline, I worry the stock has gotten ahead of itself. If TI can’t execute on those modest estimates, shares could be vulnerable to a pullback.

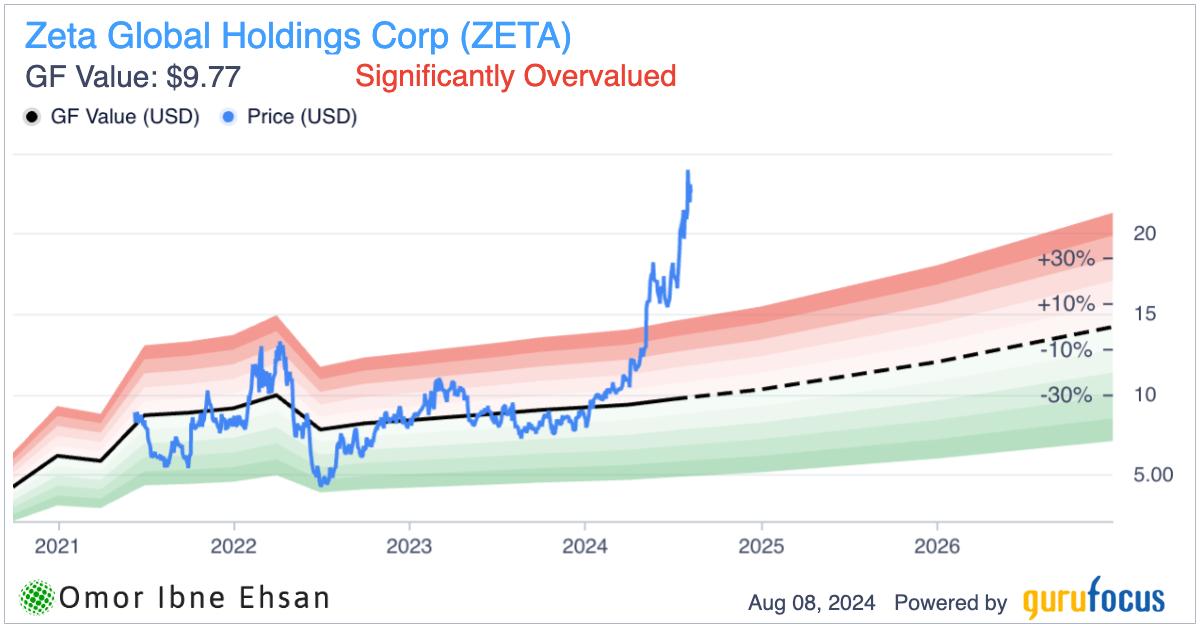

Zeta Global Holdings (ZETA)

Zeta Global Holdings (NYSE:ZETA) operates an AI-powered marketing cloud platform. The company has been on an absolute tear lately, with its stock price soaring 168% year-to-date on the back of stellar earnings results.

In Q2 2024, Zeta’s revenue jumped 33% year-over-year to $227.8 million, beating estimates by over $15 million. The company is nearing profitability as it emerges from its startup phase, with adjusted EBITDA surging 44% to $38.5 million. However, it is still loss-making if you look at it from a GAAP perspective. The Sloan Ratio still points to the quality of its earnings as “low.” Moreover, GuruFocus’ DCF model shows the stock as “Significantly Overvalued.”

Click to Enlarge

Most stocks on this “stocks to sell” list are struggling with deteriorating fundamentals, but that’s certainly not the case with Zeta. Analysts have been rushing to raise their price targets, with the average now sitting at $21. Zeta was even named a Leader in Forrester’s 2024 Email Marketing Service Providers report.

However, I think it’s time to start taking some chips off the table. If the widely anticipated recession hits, marketing and ad budgets could be the first to get slashed, putting Zeta’s growth story at risk. The stock’s huge run-up leaves plenty of room for a pullback.

Of course, I wouldn’t dare short a stock with this much momentum. But if you’re sitting on big gains, now is a good opportunity to do some trimming before we enter a trickier phase of the market cycle.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or

indirectly) any positions in the securities mentioned in this article.