Retail is being hit very hard right now, and trust me, J.C. Penney (NYSE:JCP) is no exception in this case. While the rest of the market bottomed back in March, JCP stock hit a new low just last week.

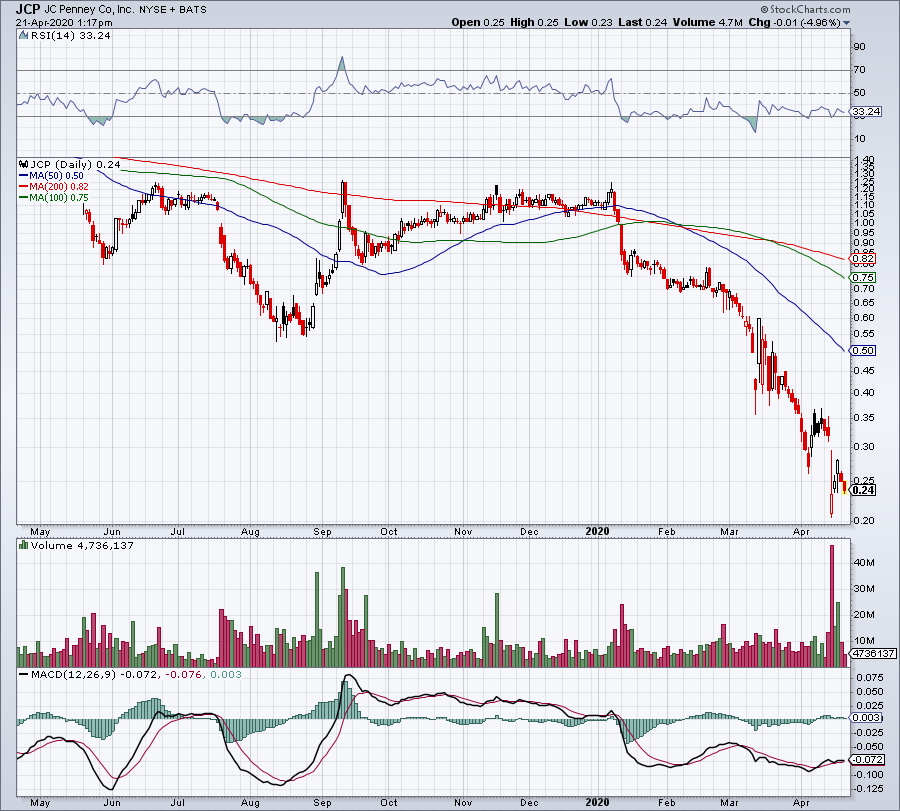

Now trading for just 25 cents per share, it’s certainly not out of the woods yet at just a nickel above its current all-time low. There’s no other way to say this but, overall, bankruptcy is not off the table when it comes to J.C. Penney.

The retailer has been struggling for years. And had the U.S. not gone through such a strong economic period, it’s unlikely JCP stock would even be around at this point. But the economic landscape is quickly shifting, and it’s very possible that J.C. Penney lacks the resources necessary to survive.

Coronavirus Wreaks Havoc

The novel coronavirus is wreaking havoc on the retail space. Reports circulated this weekend that Neiman Marcus is exploring its bankruptcy options. So is Lord & Taylor. Last month, Cheesecake Factory (NASDAQ:CAKE) said it won’t make rent for April. Moreover, REIT stocks — particularly those with retail exposure — have been decimated.

We’re in unprecedented times when it comes to investing in the retail space, and it’s becoming very clear that not every outfit is properly equipped to handle the situation. A recession is bad for retail — that doesn’t need much explanation. But we do not normally go from a decent economy to slamming on the brakes virtually overnight.

At the snap of one’s fingers, we’ve found our country — and much of the world — under lockdown and stay-at-home orders. With that, it’s going to be hard enough for decent operators like Macy’s (NYSE:M) to survive, let alone retailers that were already on the brink — like J.C. Penney.

I’m not rooting against JCP stock, or any other retailer for that matter, but the situation is quickly turning dire for those that are struggling. But for investors that want exposure though, there are options.

Amazon (NASDAQ:AMZN) continues to burn higher, as shares recently hit new all-time highs. The e-commerce giant is on a multi-month hiring spree as it tries to keep up with increasing demand. Also,

Walmart (NYSE:WMT), Target (NYSE:TGT) and Costco Wholesale (NASDAQ:COST) are all high-quality big-box retailers that have seen increased demand from consumers and are holding up amid the storm.

So investors can buy selectively in retail, but JCP stock shouldn’t be on the list.

Valuing JCP Stock

Click to Enlarge

At the end of the day, J.C. Penney just doesn’t have the resources or the strategy to survive for the long term. It’s had negative income in each of the last three years, which continues to worsen as time goes on. The company lost $116 million in 2017, $255 million in 2018 and $268 million in 2019.

The retailer also carries $147 million in current debt, and more than $3.5 billion in long-term debt. So for a company with a $89 million market capitalization, this simply an unbearable weight. With little to no cash coming in and the company doing its best to mitigate expenses, the prospects don’t look good for an entity that’s on the ropes. Man, the company just skipped $12 million worth of interest payments last week.

With all that in mind, J.C. Penney is looking at various liquidity and debt solutions for its current problem. However, bankruptcy is reportedly on the table. That right there should be all investors need to know about JCP stock, particularly when they still have the option to buy high-quality retailers that aren’t in such a binary situation.

Is it possible that J.C. Penny stock could double or triple from the 20 to 25 cent range? Of course it is — anything is. But banking on that action is gambling, not investing. We’re here for the latter, and the talk of bankruptcy doesn’t do anything for us but send us running in the opposite direction.

That said, I wish JCP stock good luck and take a hard pass.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.