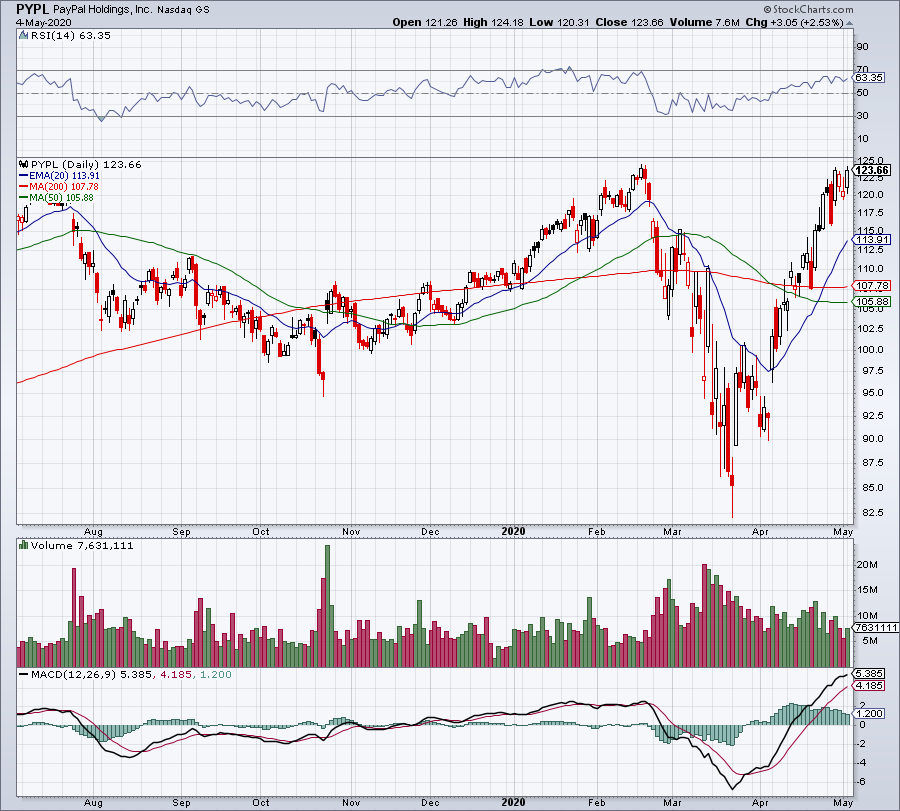

Like many other stocks in the market, PayPal (NASDAQ:PYPL) has rebounded with a vengeance. However, it’s outpacing the broader market. At last week’s high, PYPL stock was up more than 51% from the lows. That’s obviously more impressive than the market’s recent rally of ~35%.

It goes much further than that, though. PayPal stock not only rallied 50%-plus from the lows, but it recovered virtually all of its losses.

On Feb. 19 — the same day the S&P 500 peaked — PYPL stock hit a new all-time high. At last week’s high on April 29, PayPal came within 42 cents of that mark. Now some stocks have new all-time highs amid the selloff, like Amazon (NASDAQ:AMZN) and Netflix (NASDAQ:NFLX), but for PayPal to recoup virtually all of its losses is very impressive.

Why We Like PYPL Stock

The rebound is a double-edged sword though. On the one hand, this relative strength is an enormous win for bulls. That is, if they’re already long. Those who missed the boat are kicking themselves, wondering if they no longer have an opportunity in PayPal.

As great of a company as PayPal is, its stock is unlikely to hold up against the strong forces of the broader market. Otherwise, shares wouldn’t have fallen 34% from the February high to March low.

If we can get another pullback in PYPL stock, investors would be wise to buy the dip.

Click to Enlarge

PayPal has been and is the future of payments. It, along with Visa (NYSE:

V), MasterCard (NYSE:MA) and Square (NYSE:SQ), continue to fuel the transition of payments. They offer safe and secure methods of commerce, broadening how consumers can pay for goods and services.

In all of their cases, they simplify the transition of contactless, digital and cashless payments. The trend from cash and check to credit and debit has been underway for some time now. But the addition of these companies, along with alternative platforms like e-commerce and money-sending, has only fueled the transition.

Why do we want to buy PayPal on the dip? Because its growth remains so strong. Estimates have been trimmed a bit due to the economic hit from the novel coronavirus. Despite this, PayPal is forecast to grow.

Revenue estimates call for 12.3% growth in 2020 to $19.96 billion. Next year, revenue estimates accelerate back up to 18% growth. Earnings estimates for this year are a bit less impressive, with analysts expecting growth of just 4.5% to $3.24 per share. On the plus side, estimates for 2021 call for earnings growth of 23.1% to $3.99 per share.

Throwaway Year?

Should stocks be granted a so-called throwaway year? In other words, should investors simply stop focusing on this year and start focusing on 2021?

Tempting as it may be, I don’t think so.

The reasoning is simple, and that’s because there are too many unknowns. If the virus dies down into summer and either never comes back or comes back in a much more subdued manner, and consumers quickly get back into action, we have little to fear. But we don’t know that that will be the case.

We don’t know that 2021 won’t have another wave of Covid-19 or that the fourth quarter will be immune to the virus. There’s no way to accurately measure 2021 growth estimates when we have no idea how 2020 will ultimately turn out.

Many will undoubtedly look at PYPL stock trading at 37 times this year’s earnings estimates and say, “no way.” However, I would argue that the stocks still able to churn out growth are now worth a premium. Those are companies like Microsoft (NASDAQ:MSFT) and Facebook (NASDAQ:FB) too, which we also like after earnings. Most companies are experiencing a contraction in profit and sales. So those that aren’t failing to grow are now worth more and are in demand among investors.

The valuation is a little lofty for PYPL stock, but if we get a correction in PYPL this month — say back into the $90s — it looks like a very solid buying opportunity.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.