AT&T Inc. (NYSE:T) stock is down 10% year-to-date. At first glance, T stock doesn’t look like a clear buy or a clear sell, but its strengths are undeniable: a high dividend yield, modest valuation and a low beta –AT&T boasts a 5.1% yield during a time of low interest rates.

Not to mention, the modest valuation is stable during a time when the market is getting a bit frothy.

AT&T stock fluctuates less than the broader market, meaning it would fall less if the market fell, and stocks have been going up for a few years now; there could always be a pullback.

But the strength in T stock is balanced out by some weaknesses. The telecom industry isn’t the most attractive. Growth in developed markets like the U.S. is slow, competition is fierce and the industry is capital-intensive; telecoms must invest billions each year on wireless and wireline networks. Carriers haven’t been able to profit from the explosion in data usage, which instead went to tech companies like Facebook Inc (NASDAQ:FB) and Alphabet Inc (NASDAQ:GOOG, NASDAQ:GOOGL).

Furthermore, AT&T stock has a weak balance sheet and it recently lost a bidding war that might give Verizon Communications Inc. (NYSE:VZ) an advantage in rolling out 5G networks. With all of these pros and cons in mind, let’s examine them further.

AT&T Stock Pros

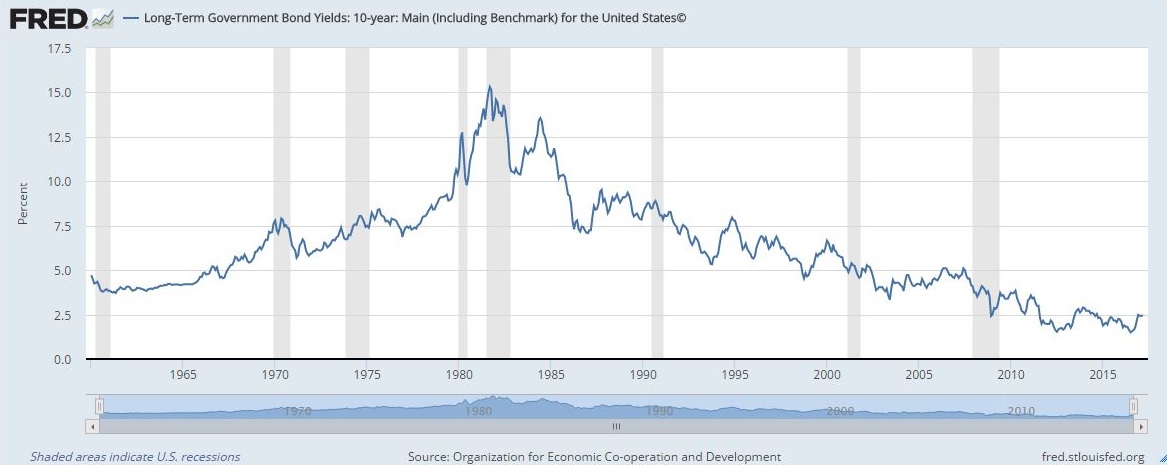

AT&T’s High Dividend Yield: Since the yield on a 10-Year Treasury note remains 2.4%, T’s 5% dividend yield is nothing to sneer at. As of today, the 5% dividend yield puts it in 9th place on the S&P 500.

And AT&T has a track record of increasing dividends, having done so almost every year since 1984 (Note: AT&T stock split in 1987, 1993 and 1998; 2004 looks like the only year dividends fell).

Dividend stocks like T stock have historically been favored by income-seeking investors, such as pensioners and insurance companies.

AT&T’s Modest Valuation: On the surface, AT&T stock doesn’t look overvalued. T stock trades at 18.7 times earnings, 13 times forward earnings, 1.9 times book value and 1.45 times sales. T’s EV/EBIT and EV/EBITDA multiples also look inexpensive.

All of his means that the market does not expect much from AT&T stock, and if a correction occurred tomorrow, the stock wouldn’t be hammered too hard.

Defensive, Low-Beta Stock: Telecom and utility stocks like T stock tend to be low-risk, since people always will need to use electricity and water and make phone calls, even during recessions.

According to Google Finance, AT&T stock is less volatile than the broader market, with a beta of 0.39. This makes T a defensive stock. If the broader market, such as the S&P 500 or the Dow Jones Industrial Average falls 10%, the stock will fall only 3.9%. Likewise, if the market goes up 10%, the stock will rise 3.9%.

Admittedly, this means that AT&T stock will lag during bull markets, but during downturns, it should outperform the market by falling less.

Indeed, this was the case from October 2008 to October 2009, a time of economic turmoil. Major banks went bankrupt and automakers needed to be bailed out. T stock fell less than the market, which bottomed in March 2009 and didn’t catch up with the stock until October 2009.

If you hold bearish views about the stock market and think it is overvalued, you could add AT&T stock to your portfolio to reduce your losses if and when stocks tank.

AT&T Stock Cons

Tough Industry: Telecom isn’t a very attractive industry.

Data usage has exploded since 2000, but the phone companies failed to capture much of the value, which went to tech companies, including Apple Inc. (NASDAQ:AAPL) and Amazon.com, Inc. (NASDAQ:AMZN). U.S. carriers have stagnated, with average revenue per user actually falling since 2006.

And these tech companies have added insult to injury. Phone companies lost revenue from text and voice services to apps such as WhatsApp, Facebook Messenger, Viber and Skype. Also, as I discussed in March, Alphabet and Facebook threaten carriers with projects to use drones and balloons to provide internet access.

Click to Enlarge The U.S. market for telecom services is saturated, with wireless penetration passing 100% in 2011. This means that there is little room for growth, and that AT&T must battle rivals like Verizon, Sprint Corp (NYSE:S

), and T-Mobile US Inc (NASDAQ:TMUS). Telecoms have resorted to buying customers, enticing them to switch by offering to pay early termination fees — Verizon claims that you can get up to $650 for switching.

Competition from T-Mobile has forced major carriers in the U.S. to offer subscribers unlimited data plans. If that weren’t enough, cable companies like Comcast Corporation (NASDAQ:CMCSA) and Charter Communications, Inc. (NASDAQ:CHTR) are looking to offer customers cellular data and phone services.

AT&T’s Balance Sheet: As a result of AT&T’s big acquisitions, it’s debt has gone up. T’s debt-to-equity ratio went up from 0.82 in 2013 to 1.00 in 2016. The company bought DirecTV in 2014 for $48.5 billion, issuing $17.5 billion in bonds in 2015 to finance the deal.

Click to Enlarge Last year, AT&T purchased media giant Time Warner Inc (NYSE:TWX), which owns CNN, for $85 billion. This deal, which Wall Street issued $40 billion in debt to finance, makes T one of the most debt-laden companies in the world. The combined company will hold $175 billion in debt, the New York Times says this making AT&T “the largest nonbank corporate issuer”. Rating agency Moody’s issued a warning and put AT&T on a watch list. A SeekingAlpha contributor wrote that the combined company would have a tangible book value of negative $185 billion.

This high debt load could endanger the AT&T dividend, which is one of the main arguments given by the stock’s bulls.

Lost Straight Path to Verizon: Carriers like AT&T are racing to transition from 4G to 5G networks, and T plans to roll out 5G in two cities this year, Austin and Indianapolis. But Verizon successfully outbid AT&T for Straight Path Communications Inc (NYSEMKT:STRP), which holds high-frequency spectrum licenses covering most of the United States. This will give Verizon an advantage over T in the race to 5G, helping it develop a fast and reliable network, while AT&T will have to look elsewhere.

Bottom Line on T Stock

When you look at the whole picture, AT&T stock doesn’t look so enticing.

One of its greatest strengths, its dividend, looks fragile when examined closer.

First, can T sustain a 5% dividend yield given its mountain of debt and the need to invest in 5G technology? InvestorPlace contributor Aaron Levitt warned that if the company’s push into media fails, the AT&T dividend would be in jeopardy.

Also T has piled up this debt while interest rates were relatively low. If interest rates rise and the company has to refinance its debt at higher rates, what might happen? This could be dangerous

And some think dividend stocks are a bubble. Interest rates were very low from 2009 on, meaning that if you bought a bond, you wouldn’t get much of a return. This led to yield-seeking behavior among investors who normally would have invested in bonds, but instead turned to dividend stocks like T as an alternative.

Click to Enlarge

After all, AT&T’s 5% dividend yield beats the yield on a 10-year note.

If interest rates rise, perhaps some of that money will flow out of T stock and into newly issued bonds offering higher returns.

And low valuation alone isn’t a reason to buy AT&T stock. A stock could always be valued low for a good reason; the market isn’t always wrong. Warren Buffett wrote in 1989 that “It’s far

better to buy a wonderful company at a fair price than a fair company at a wonderful price.”

Ultimately, AT&T’s pros don’t look so strong, while the cons look like real concerns. For these reasons, I would stay away from T stock.

As of writing, Lucas Hahn did not hold a position in any of the aforementioned securities.