In the wickedly competitive world of chip-making, it’s good to have a stock like Intel Corporation (NASDAQ:INTC) in your portfolio. It no longer has the “wow factor” of a Facebook Inc (NASDAQ:FB) or an Amazon.com, Inc. (NASDAQ:AMZN), but INTC is still very much relevant. Many of the technologies and conveniences we take for granted have been pioneered by the semiconductor giant. As an overall investment, Intel stock has been stellar.

Still, does that translate into profits moving forward?

The conventional wisdom says yes, and I don’t necessarily disagree. On the immediate front, Intel stock carries a tremendous brand and world-class assets. Definitely, there are competitors like Advanced Micro Devices, Inc. (NASDAQ:AMD) making waves in the markets. However, no one ponders whether or not Intel stock has been the more reliable of the two.

And according to NDTV, the company has been ranked among the top ten most powerful brands in the world, right behind International Business Machines Corp. (NYSE:IBM) and Alphabet Inc (NASDAQ:GOOG, NASDAQ:GOOGL).

Plenty of Positives for Intel Stock

Perhaps one of the biggest nearer-term catalysts for INTC stock is the rumor that Apple Inc

. (NASDAQ:AAPL) will manufacture its ever-popular iPhone in the U.S. From the Nikkei Asian Review, a “key Apple assembler” Hon Hai Precision Industry Co., Ltd.-ADR (OTCMKTS:HNHPF) is exploring the idea of shifting the smartphone production stateside. If true — lips are currently sealed — that would be a boon for the upcoming Donald Trump presidency, and Intel stock.

Interestingly, for the company’s third quarter of fiscal year 2016 earnings report, INTC lowered fourth-quarter revenue due to “next-generation manufacturing capabilities.” Normally, an investment for the future would be considered a positive thing. However, Wall Street punished Intel stock at that time. Apparently, investors were looking for an immediate play.

It does seem strange, though, that INTC would deliberately lower guidance — unless, of course, they had a major ace up their sleeve. A closer relationship with AAPL would do the trick.

The report also telegraphs just how important the “Internet of Things” is to INTC. With everything in our world steadily becoming digitalized, technology companies have to adapt, or risk obsolescence. It’s to Intel’s credit that they’re making tough choices now to reap the reward later. This runs contrary to what most organizations in the tech sector are doing.

INTC Stock Is Raising Eyebrows

Of course, when all is said and done, it boils down to individual buyers. Industry tailwinds and high-performing financials are wonderful, but they don’t always translate well in the markets. Yes, a powerful argument can be made that Intel stock is being gutted for no good reason. The company’s data center business is rapidly increasing. It’s relatively undervalued against projected earnings.

It also pays a handsome dividend while being a reliable investment.

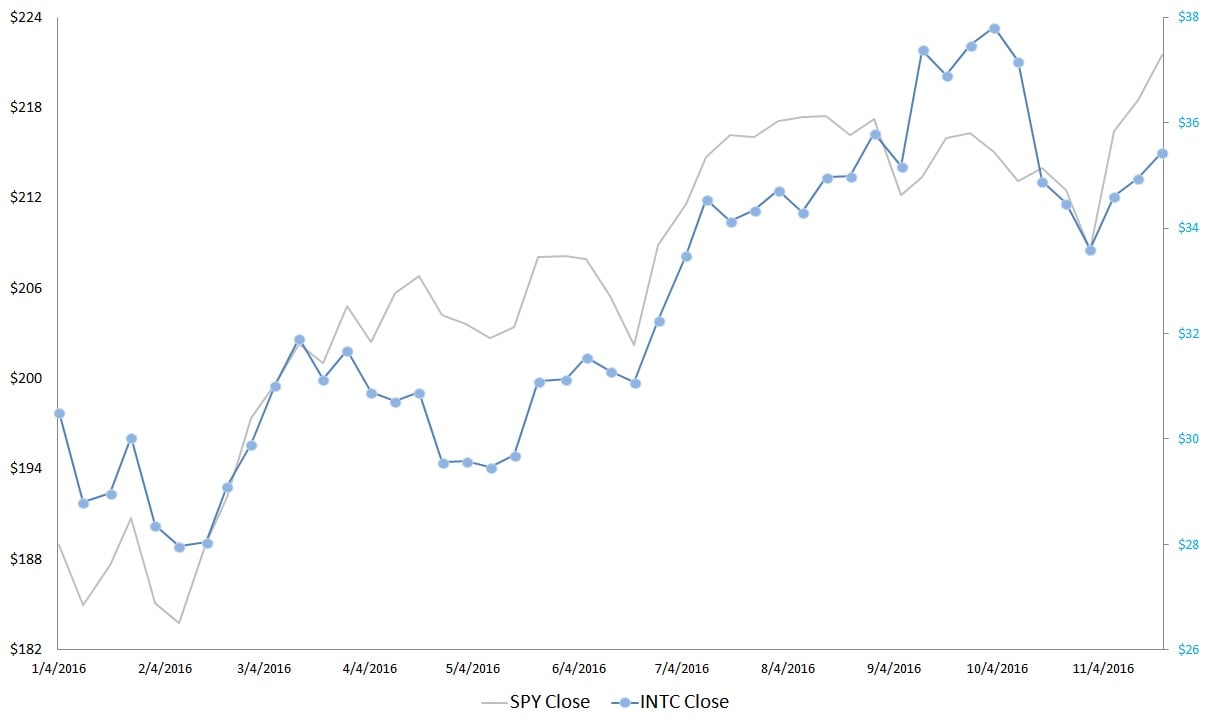

But none of these bullet points are yet filtering through to buyers. Year-to-date, INTC stock sits up about 1.5%. Meanwhile the benchmark SPDR S&P 500 ETF Trust (NYSEARCA:SPY) is nearly raking in 8.5%.

Click to Enlarge

The flipside risk to the “everybody is getting it wrong” argument is that everybody could be getting it right. In other words, it’s a tough game to suggest that the masses are just not seeing the opportunity.

For limited markets like silver coins in the late 1990s, or low-volume penny stocks, I completely understand. But for Intel stock? This is a company that has been analyzed and reanalyzed seven ways to Sunday. Like polling the audience in “Who Wants to Be a Millionaire?,” it’s usually best practice to go with the consensus answer if the question has broad appeal.

Bottom Line for INTC

With the risks being considered, there’s no justification for shorting Intel stock at this juncture. It’s riding a long-term bullish trend channel that doesn’t show signs of faltering. Plus, should the rumors of stateside Apple production pan out, INTC is in prime position to maximize the opportunity.

Even if the rumors are just that, the next-gen businesses should make up for the painful shortfall in the personal computer sector.

Where I am cautious is that Intel stock has lost its sex appeal. Annual returns this decade are averaging less than 13%, well below its lifetime average of 22%. Furthermore, the highest returns of the prior three decades averaged 114%. This decade, the highest so far is 45%, set in 2014. True, profits are made in the future, not the past. But it would also be foolish to expect something when the hard data indicates otherwise.

INTC stock will be relevant for years to come. There’s too much going on, and too many critical investments made to state the contrary. Nevertheless, you have to keep Intel stock in perspective.

If you want a legacy investment, few others will fit the bill. But if you want profits now, any tech stock but INTC may be a better choice.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.