At the beginning of the month, Netflix, Inc. (NASDAQ:NFLX) reported stellar earnings results. Revenue, domestic subs and international subscribers all beat expectations. Admittedly, earnings did come in a tad light. The NFLX stock price has had a modest 9%-plus rally since, but is having trouble finding traction over $200.

No one will argue with Netflix’s subscribers growth rate. Analysts were looking for 4.5 million new subscribers last quarter. Coming in at 800,000 more than expected, the 5.3 million new subs wowed analysts. Expectations for 6.3 million more next quarter only made it more exciting. That also made it easier to overlook the company’s budget for 2018. Management expects to spend somewhere between $7 billion-$8 billion on content next fiscal year. Whoa!

How should we trade NFLX stock now and what risks lie ahead?

Impressive Cash Flow

Netflix is growing sales at an impressive clip, as estimates call for 32% growth this year. But with forecasts calling for sales of “just” $15 billion next year, the midpoint ($7.5 billion) of its content budget would represent half of Netflix’s revenue.

Understandably, content drives subscriptions. No one wants to use Netflix if it has no content and licensing has proved expensive (not that they won’t license going forward). The point is, content drives subs and subs — for now — drive NFLX stock. More content also makes the platform “stickier” and less likely for subs to ditch. It also allows Netflix to up the price, as it recently raised domestic prices by $1 for its standard service.

This will add an extra $600 million to $700 million to its annual revenue and help ease the burden of that content costs. The analysts have been out in droves since the report, with many assigning price targets from $225 to $250. Pivotal Research owns the Street-high call for $270 per share.

Free-cash flow expectations call for a $2 billion to $2.5 billion deficit this year. In May, NFLX raised $1.56 billion in senior debt, with added another $1.6 billion in October. Before the raise, total debt had more than doubled year-over-year from $2.4 billion to $4.9 billion.

Competition is Just Getting Started

Technology is forcing a massive (and fast) shift in traditional industries. It’s throwing the retail sector into chaos as e-commerce solutions remove the middleman. It’s happening with content now, too. Why pay Charter Communications, Inc. (NASDAQ:CHTR) or Comcast Corporation (NASDAQ:CMCSA) $100 or more per month when you can pay $10 for Netflix, $15 for HBO and add a few other subscriptions for half the price?

Roku Inc (NASDAQ:ROKU) devices have kept the TV relevant with these services. And while Netflix is certainly leading the cord-cutting charge, others are threatening to bust it wide open. Amazon.com, Inc. (

NASDAQ:AMZN) broadcasting Thursday night NFL games shows tech is taking that step. So, too, does Alphabet Inc (NASDAQ:GOOGL) and its YouTube TV package for $35 per month.

For the record, I use YouTube TV. I can watch all my local sports teams in real time. I have unlimited DVR and can watch it on any device I want. Add in HBO and Netflix and we’re talking $60 per month — 40% cheaper than my cable bill (not including its HBO!). Arguably, the content is better anyway.

Facebook Inc (NASDAQ:FB) could be an issue, too. Will it be free to use for its 2 billion users and make money from advertising? I would guess so. Apple Inc. (NASDAQ:AAPL) has dabbled in content too. It also has a wide reach like Facebook. These could be potential competitors to Netflix down the line.

This is why Netflix is spending so much. It goes hand in hand. Netflix needs to continue gaining and retaining customers so that 10 years, 20 years from now Netflix is just a constant in users’ lives that they don’t think twice about paying for each month.

Trading NFLX Stock

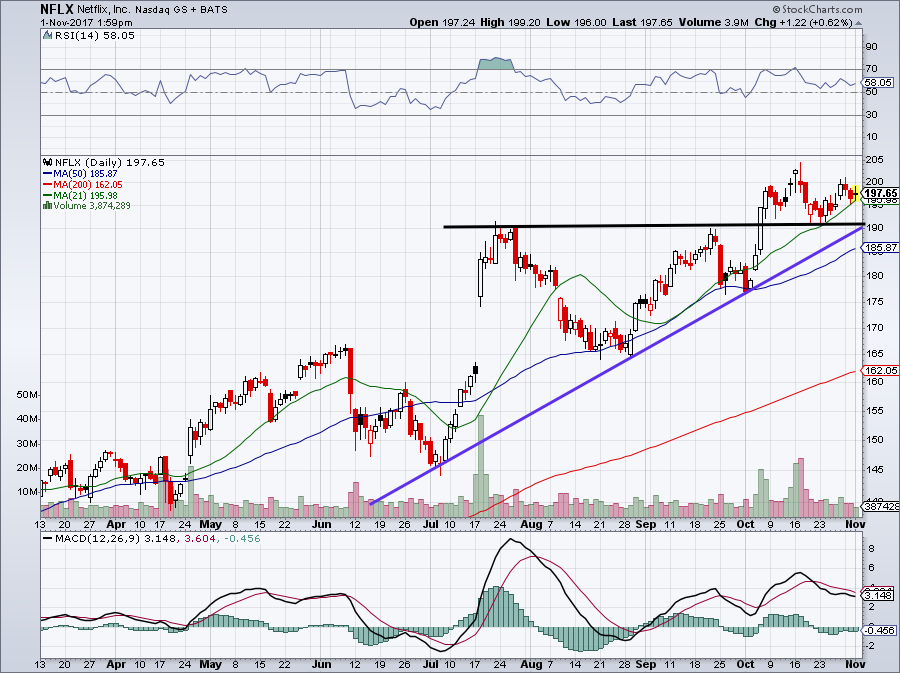

Click to Enlarge

The debt is certainly a concern and the fact that Netflix is burning through billions in free-cash flow isn’t comforting. Robust sales growth and strong subscriber numbers are promising. Investors just need to keep certain things in perspective.

For now and likely into the future, NFLX stock will not trade with a normal valuation. Critics will point out the flaws in its balance sheet, much like they did with Amazon’s income statement (high valuation, no profit).

In all likelihood though, the market will shrug off these concerns. NFLX stock will have its stumbles, but for now the direction is higher.

On that note, look at the chart (above). There’s been steady trend support (purple line) since July. Further, $190 was previous resistance (black line). It now serves as support. Should NFLX stock price break through $205, it could kickstart a further rally. Traders can go long NFLX stock at current levels, and use a close below $190 as their stop-loss.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.