While Apple Inc. (NASDAQ:AAPL) held up for most of Monday, it ultimately fell 0.73% in the session. This is far from a crisis, but the swift decline in tech has many feeling uneasy. However, the AAPL stock price still looks fine on the back of its strong iPhone performance.

Everyone and their brother will want the new iPhone this year, be it the older iPhone 7 and 7 Plus, new 8 and 8 Plus or the face-scanning iPhone X. There’s a few reasons why I think Apple’s iPhone will drive AAPL stock to all-time highs.

iPhone Sales Will Drive Record Results

According to IHS Markit, Apple will likely ship about 89 million iPhones in the fourth quarter. My guess is that that figure would be higher if not for the supply constraints Apple has faced, particularly with the iPhone X.

While that may not make for a blow-the-roof-off quarter, it will extend Apple’s sales and earnings. Why? Because very few customers, in my view, will opt for an in-stock Android device if they went to Verizon Communications Inc. (NYSE:VZ) or AT&T Inc. (NYSE:T) looking for an iPhone.

According to IHS, Apple would need to ship about 31 million iPhone X units to drive its average selling price (ASP) north of $700 for the first time ever. Its data says iPhone X activations are strong.

But don’t forget about the memory. While the iPhone 8 and X come standard with 64 GB of storage, the next option for 256 GB is only $150.

With T-Mobile Us Inc (NASDAQ:TMUS), Sprint Corp (NYSE:S) and AT&T offering various buy-one-get-one iPhone deals, this is sure to tempt some consumers into higher-memory phones. And why not? The worst thing is buying a new phone, only to have it run out of space in a year or two.

Admittedly, 64 GB is a lot of space. But with 4K filming, high-def photos and various augmented reality applications, 64 GBs could be gone sooner than you think. Plus, $150 to quadruple your storage is a relatively cheap price to pay.

Why Does This Matter?

An extra $150 on an iPhone 8 Plus drives the cost up to $949, close to that of an iPhone X. For the record, if IHS is correct in that Apple will sell 88.8 million iPhones this quarter, and we use $700 as the ASP, we come up $62.1 billion in revenue — from the iPhone alone!

IHS says Apple will likely have record-breaking iPhone shipments

in 2018, a stand I tend to agree with as well. I think there will be a greater makeup of 8 Plus, X and higher-memory iPhones than investors currently expect.

Analysts expect quarterly earnings of $3.77 per share on revenue of $86.2 billion. This trumps last year’s first quarter results of $3.36 per share on revenue of $78.4 billion by 12.2% and 9.9%, respectively. But the best part? These metrics should accelerate throughout 2018 because Apple was supply-constrained to begin the fiscal year.

Further, AirPod sales are expected to double, a product that runs for $150. The Apple HomePod, which will retail for $349, will become available in 2018, too. The new Apple Watch is leaps and bounds better than the last iteration, and services revenue should continue growing handsomely.

All of these carry high margins, so while they may not move the sales needle that much, it has a larger impact on the bottom line.

That’s why year-over-year earnings and sales are forecast to grow 24.2% and 19.65%, respectively in 2018 vs. 2017. That’s monster growth for a stock like Apple.

Trading AAPL Stock

It’s hard to believe AAPL stock trades with a trailing price-to-earnings (P/E) ratio of 19 and a forward P/E ratio of 14. Even despite its world-renowned brand and its impenetrable fortress of a business, the numbers are incredible.

AAPL is growing sales 20% and its earnings 24% this year, and all it gets is a 14x multiple? That makes no sense.

In fact, Apple’s revenue and earnings growth for the next 12 months is roughly on par with Alphabet Inc (NASDAQ:GOOGL, NASDAQ:GOOG), Paypal Holdings Inc (NASDAQ:PYPL) and salesforce.com, inc. (NASDAQ:CRM). Yet those stocks trade with a forward P/E ratio of 24, 31 and 58, respectively. Although the AAPL stock price is up 46% so far in 2017, one could make a case that it’s actually undervalued.

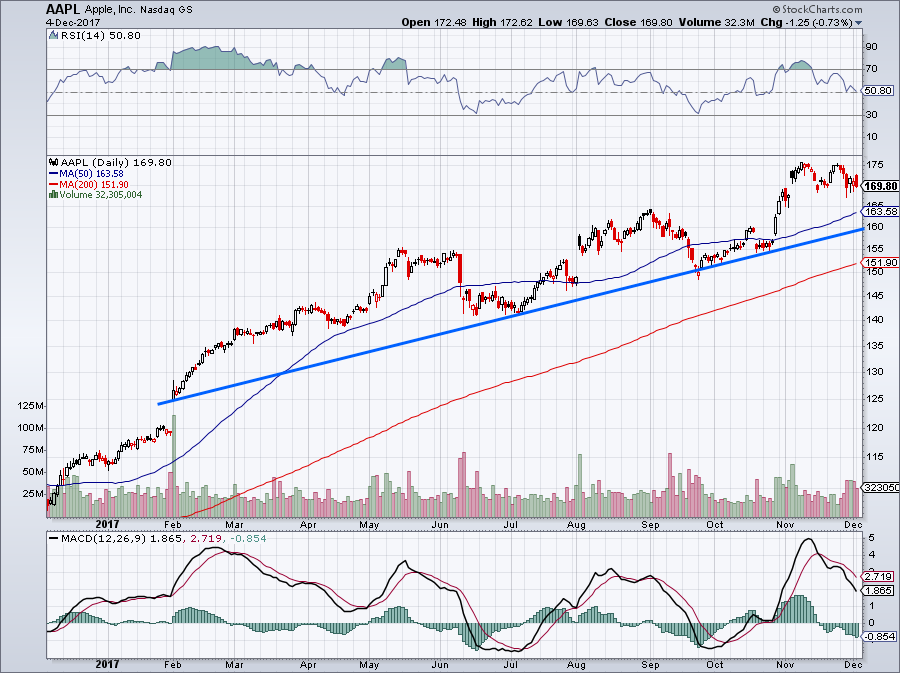

Click to Enlarge

Let’s keep it simple with AAPL stock. The AAPL stock price is moving from the lower left to the upper right. Apple’s trend line has been in place since the stock broke out in February. If it retests, which is currently at $160 but could be in the lower to mid-$160s on a correction, AAPL stock is a buy.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell held a position in CRM.