About a year ago, I coined the high-growth STARS acronym on InvestorPlace, saying that these five growth stocks — Shopify (NYSE:SHOP), The Trade Desk (NASDAQ:TTD), Adobe (NASDAQ:ADBE), Roku (NASDAQ:ROKU), and Square (NYSE:SQ) — are the high quality, big return potential stocks that investors want to buy now and hold for the next several years.

The idea behind the STARS acronym was simple. The market’s favorite high-growth acronym — FANG, which comprises Facebook (NASDAQ:FB), Amazon (NASDAQ:AMZN), Netflix (NASDAQ:NFLX), and Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL) — was becoming increasingly obsolete for investors. That’s not to say that FANG companies have peaked. They haven’t. They are still doing very well. But, they are such large companies and long FANG is such a crowded trade, that the long-term return potential in these names isn’t what it used to be. It almost certainly isn’t the best return potential investors can find in the overlap of growth and technology.

STARS is exactly that. Each one of the STARS stocks is supported by huge secular growth trends, is small relative to their addressable markets, is unknown relative to the FANG stocks, and has huge upside potential in a multi-year window. That’s why I told investors to forget FANG and buy the STARS stocks a year ago.

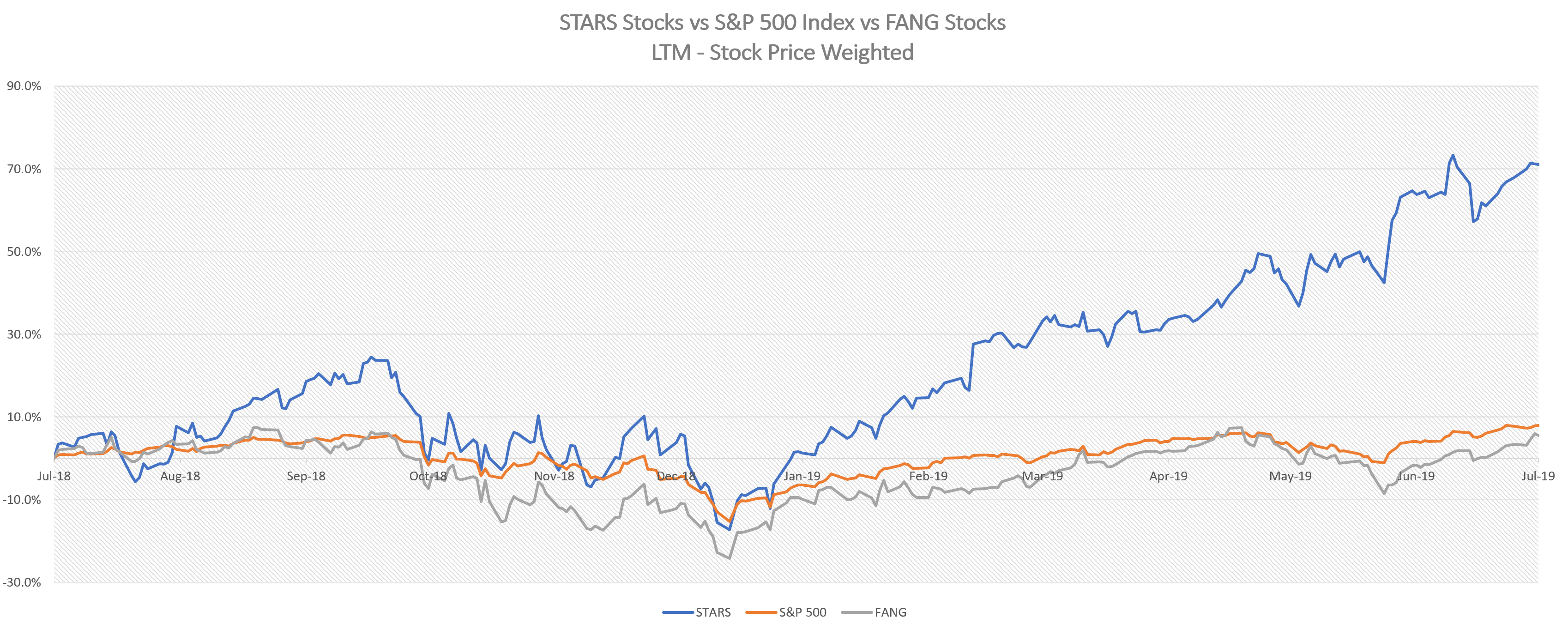

The results speak for themselves. Over the past year, the S&P 500 is up about 7.5%. Had you bought one share in each of the FANG stocks, you would be up just 5% over the past year. But, had you bought one share in each of the STARS stocks, you would be up more than 70% over the past year.

Click to Enlarge

In other words, STARS stocks have generated more than 60 points of alpha over both the S&P 500 and FANG stocks over the past twelve months.

This out-performance from the STARS group will continue. Without further ado, let’s take a deep look at why you should buy each one of these high-quality growth stocks.

STARS Stocks to Buy for the Long Run: Shopify (SHOP)

Trailing 12-Month (TTM) Gain: 90%

The Bull Thesis Tag Line: “The Next Big Thing in Commerce”

Core Bull Thesis: The secular bull thesis on e-commerce solutions provider Shopify is simple. Thanks to the widespread proliferation of the internet, the commerce world is two doing things: One, it’s pivoting into direct retail, wherein brands and merchants are selling to and communicating with customers. Two, it’s also pivoting into a decentralized model, wherein anyone can sell anything to anyone else.

Shopify is at the heart of both these pivots, providing the tools which allow any seller to sell any item through any direct channel, and is thus levered to benefit from the expansion of these two huge secular tailwinds.

These tailwinds are still in their early innings. Shopify’s gross merchandise value represents less than 1.5% of global e-retail sales, and is growing at a steady 50%-plus pace. Further, Shopify just started to jump into the physical retail world, dramatically expanding this company’s addressable market.

As such, SHOP has the necessary room and firepower to keep growing at a robust rate for a lot longer.

Key Growth Projections:

- Shopify goes from 1.5% e-retail market penetration today, to 7.5% penetration by 2030, as direct decentralized retail trends gain mainstream traction.

- Shopify goes from about 0% physical retail market penetration today, to about 0.5% penetration by 2030, as Shopify finds some success in the physical retail world.

- Total gross merchandise volume (GMV) and Merchant Solutions revenue grow at about 30% annualized pace into 2030.

- Subscription Solutions revenue grows at a high teens annualized pace, as Shopify continues to grow its merchant base.

- Total revenue grows at a 25%-plus pace over the next decade.

- Operating margins scale from 1% today, to 25% by 2030, as robust revenue growth drives significant operating leverage on already huge gross margins.

- 2030 EPS settles around $25, versus projected EPS in 2019 of $0.60.

Long-term Price Target: About $750, based on a commerce platform average 30-forward multiple on projected fiscal 2030 EPS of $25.

Present Value: About $300, based on a 10% discount rate and a 2029 price target of $750.

The Trade Desk (TTD)

The Bull Thesis Tag Line: “The Future of Advertising”

Core Bull Thesis: The secular bull thesis on The Trade Desk centers around something called programmatic advertising. Programmatic advertising is essentially automation in the ad industry. Before, ad spend allocation was largely a guess-and-check effort, while ad transactions were conducted between two human parties. Programmatic advertising automates both of those processes, leveraging AI and big data to optimize ad spend allocation and dynamically transact ads based on those optimal allocations. In this sense, programmatic advertising is the future of advertising.

The Trade Desk is one of the most important players in the programmatic advertising world, and one of the fastest growing, too. But, ad spend through the TTD platform measures less than 1% of the near $300 billion global digital ad market. That market is rapidly marching towards $500 billion-plus levels. Eventually, most of that $500 billion-plus worth of spend will be transacted programmatically, and the lion’s share of that programmatic spend will happen through TTD.

As such, The Trade Desk has huge growth potential over the next several years through automation in the ad world, and if all that growth potential materializes as expected, TTD stock will fly higher from here.

Key Growth Projections:

- The global advertising market measures around $1 trillion by 2025, up from $650 billion-plus this year.

- The digital ad market grows to around $650 billion by 2025, representing 65% share versus 45% share in 2018, as engagement and ad dollars continue to flow into the digital channel.

- TTD grows its share in the digital ad market from less than 1% in 2018, to 2-2.5% by 2025, as programmatic advertising becomes more widely used across various ad formats and channels.

- Gross spend on TTD and revenues grow at a 25%-plus pace into 2025.

- Profit margins gradually move higher as robust revenue growth drives positive operating leverage on healthy gross margins.

- 2025 EPS comes in around $15, versus 2019 estimates of $2.90.

Long Term Price Target: About $375, based on a digital ad average 25-forward multiple on projected 2025 EPS of $15.

Present Value: About $230, based on a 10% discount rate and a 2024 price target of 375.

Adobe (ADBE)

The Bull Thesis Tag Line: “The Cloud Giant in a Visually Dominated World”

Core Bull Thesis: The secular bull thesis on cloud giant Adobe is predicated on two very simple ideas: First, the world is becoming increasingly obsessed with visuals. Consumers are increasingly engaged in visual-first social media apps, like Instagram and Snapchat. They are also spending more time on visual-content-heavy streaming platforms like Netflix. At the same time, businesses are increasingly using visuals to communicate with their customers, since these forms of communication are what resonates most deeply with today’s consumer. Thus, both consumers and enterprises are shifting to a more visually-focused world.

Second, Adobe is the unrivaled king in delivering visual solutions. Sure, there are a ton of Adobe competitors out there, but none really rival Adobe. They are all just knock-offs. Long story short, Adobe dominates the visual-focused industry, and when it comes to creating visuals on both the consumer side (e.g. editing a photo for Instagram) and the enterprise side (e.g. creating a visually aesthetic ad campaign), everyone turns to Adobe solutions.

Put those two ideas together, and it becomes increasingly obvious that Adobe has plenty of room to grow over the next several years as both consumers and enterprises increasingly adopt visual-focused cloud solutions.

Key Growth Projections:

- Adobe’s Document Cloud, Creative Cloud, and Experience Cloud businesses continue to grow at a robust pace over the next several years given digital and visual related tailwinds, and ultimately power about 15% annualized revenue growth into 2025.

- Gross margins expand gradually towards 90% as Adobe benefits from steady but small price hikes given lack of competition.

- Operating margins expand towards 50% as 15% revenue growth drives healthy operating leverage on huge gross margins.

- EPS settles around $23 by fiscal 2025.

Long Term Price Target: About $460, based on a growth average 20 forward multiple on projected fiscal 2025 EPS of $23.

Present Value: About $290, based on a 10% discount rate and a fiscal 204 price target of $460.

Roku (ROKU)

TTM Gain: 111%

The Bull Thesis Tag Line: “The Cable Box of the Streaming World”

Core Bull Thesis: When I first created the STARS acronym, the most controversial stock on the list was Roku, given what many perceived as huge competition risks. But, ROKU stock is up 111% over the past year as the company’s secular bull thesis has drowned out competition risks.

The core bull thesis here is that Roku is becoming the central access point (or “cable box”) of the streaming world — a platform which consumers everywhere rely on to access their favorite streaming services like Netflix, HBO, Amazon Video, and the like.

A year ago, there were concerns that Roku couldn’t maintain this “cable box of the streaming world” positioning because bigger competitors would come in and gobble up its customer base. But, those concerns missed three big things: 1) Roku is content-neutral, it’s competitors aren’t, and this content neutrality ultimately makes for a more friction-less viewing experience; 2) Roku is already the runaway leader in this space, and consumers like the intuitive Roku UI; and 3) the streaming space will big enough to accommodate more than one service platform aggregator.

As such, Roku has done nothing but rattle off big-growth quarter after big-growth quarter over the past year, and ROKU stock has more than doubled in the process. The streaming market globally is still relatively nascent, and ad dollars are just now starting to follow consumers into the streaming channel, so Roku’s long-term growth narrative is in its first few innings. Over the next several years, the company will continue to rattle off big-growth quarters and ROKU stock will trend higher.

Key Growth Projections:

- The global streaming-video-on-demand (SVOD) market grows from roughly 300 million households today (25% TV household penetration), to around 600 million households by 2025 (35% TV household penetration, assuming mild global TV household growth).

- Roku’s platform goes from about 30 million accounts in 2018 (about 10% market share) to about 100 million by 2025 (about 17.5% share).

- Average revenue per user rises at roughly 15% per year into 2025, as unit SVOD revenue moves higher due to higher streaming service prices and more streaming service subscriptions per account, and AVOD revenue moves higher from a higher inflow of ad dollar volume.

- Total revenues rise at a 25%-plus pace into 2025.

- Platform gross margins scale towards 70%, while player gross margins stay around 5%.

- The opex rate drops to 40% as robust revenue growth drives significant operating leverage.

- EPS settles around $5.50 by 2025.

Long Term Price Target: About $165, based on a big growth 30-forward multiple on projected fiscal 2025 EPS of $5.50.

Present Value: About $100, based on a 10% discount rate and a projected 2024 price target of $165.

Square (SQ)

TTM Gain: 22%

The Bull Thesis Tag Line: “The Backbone of Modern Commerce”

Core Bull Thesis: The secular bull thesis on Square is based on the idea that Square is transforming into the backbone of the the modern commerce world by creating a payments ecosystem tailored to 21st century consumption and retail habits.

Consumers globally are pivoting away from cash transactions towards non-cash transactions, because non-cash transactions are significantly more convenient and more levered to digital shopping. As such, global non-cash transaction volume has risen at a steady 10%-plus clip for the past several years.

Over the next several years, non-cash payments volume is expected to run at a 10%-plus pace, driven by heavier card usage in developed economies and broader urbanization and digitization in developing economies.

Square has built a payments platform which helps merchants of all shapes and sizes process these non-cash transactions. On top of that, the company has developed a myriad of tangential solutions – such as a digital peer-to-peer payments app, an enterprise payroll app, and lending services – all of which are tailored to the consumption and retailing habits of the 21st century.

Square is developing a payments ecosystem which is built for modern commerce. Yet, the platform still only accounts for 0.35% of all global retail sales. As such, the trends and addressable market here imply that Square has a lot of room and firepower to grow over the next several years.

Key Growth Projections:

- Global retail sales grow at a 5% compounded annual growth rate into 2025 to nearly $34 billion, due to inflation and global urbanization trends.

- Square’s market share of the global retail sales pool rises from 0.35% in 2018, to 1% by 2025, as the company expands its reach in the physical retail world from micro-merchants to bigger merchants, and as the company takes a deeper dive into the e-commerce world.

- Square GPV grows at a 20%-plus annualized pace into 2025, while revenues grow at at 25%-plus annualized pace, driven by incremental revenue from hardware and ancillary solutions.

- Profit margins move steadily higher over the next several years as increased scale drives positive operating leverage.

- EPS settles around $4.50 by fiscal 2025.

Long Term Price Target: About $135, based on a payments stock average 30-forward multiple on fiscal 2025 EPS of $4.50.

Present Value: About $85, based on a 10% discount rate and a fiscal 2024 price target of $135.

As of this writing, Luke Lango was long FB, AMZN, NFLX, GOOG, SHOP, TTD, ADBE, ROKU, and SQ.