Morgan Stanley put out an interesting note in recent days which broadly outlined a handful of stocks to buy given their robust exposure to SHEconomy tailwinds.

If you had to do a double-take there, don’t worry. SHEconomy is not a commonly used term in the financial world, or any world for that matter. But, it is a term that you should get comfortable with, and quickly. Understanding the SHEconomy could help you pick winning stocks for the next several years.

Broadly speaking, the SHEconomy is the part of the U.S. economy that is driven by women (hence the “SHE”). Morgan Stanley argues that this part of the economy is booming, and driving much more economic growth than the part driven by men.

They are right. The data here is indisputable (sourced from here and here). There are three big factors at play here:

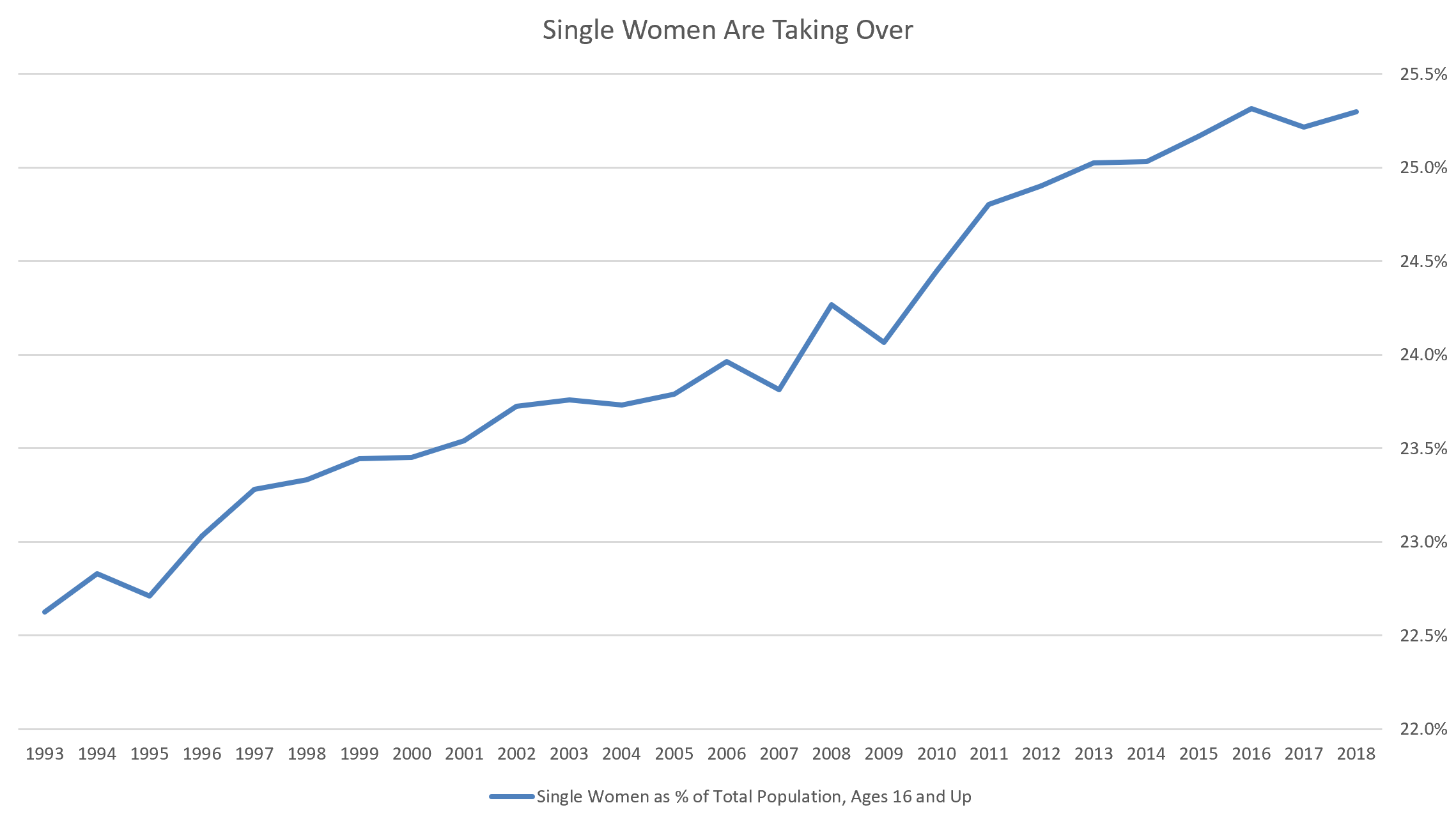

- Single women are taking over. The number of single women in the U.S. (never married, divorced or widowed) has

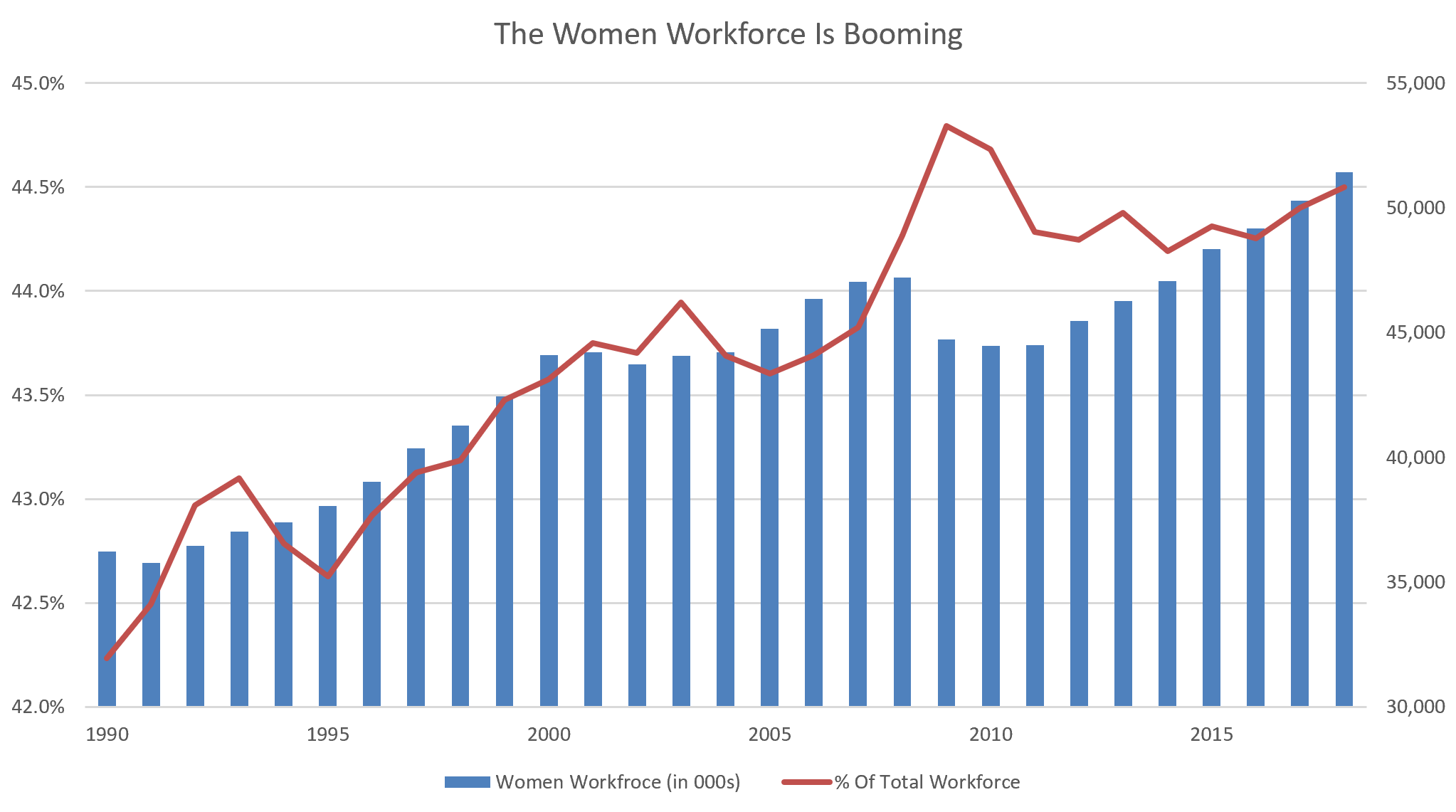

grown at a 1.6% compounded annual growth rate since 1990. Single women as a percentage of the total U.S. population, ages 16 and up, has risen from ~23% in the 1990s, to ~24% in the 2000s, to ~25% in the 2010s. - The women workforce is expanding. The number of working women in America, ages 16 and up, has grown at a 1.3% CAGR since 1990, while as a percentage of the total workforce, women have gone from ~43% representation in the 1990s, to ~44% in the 2000s, to ~44.5% in the 2010s.

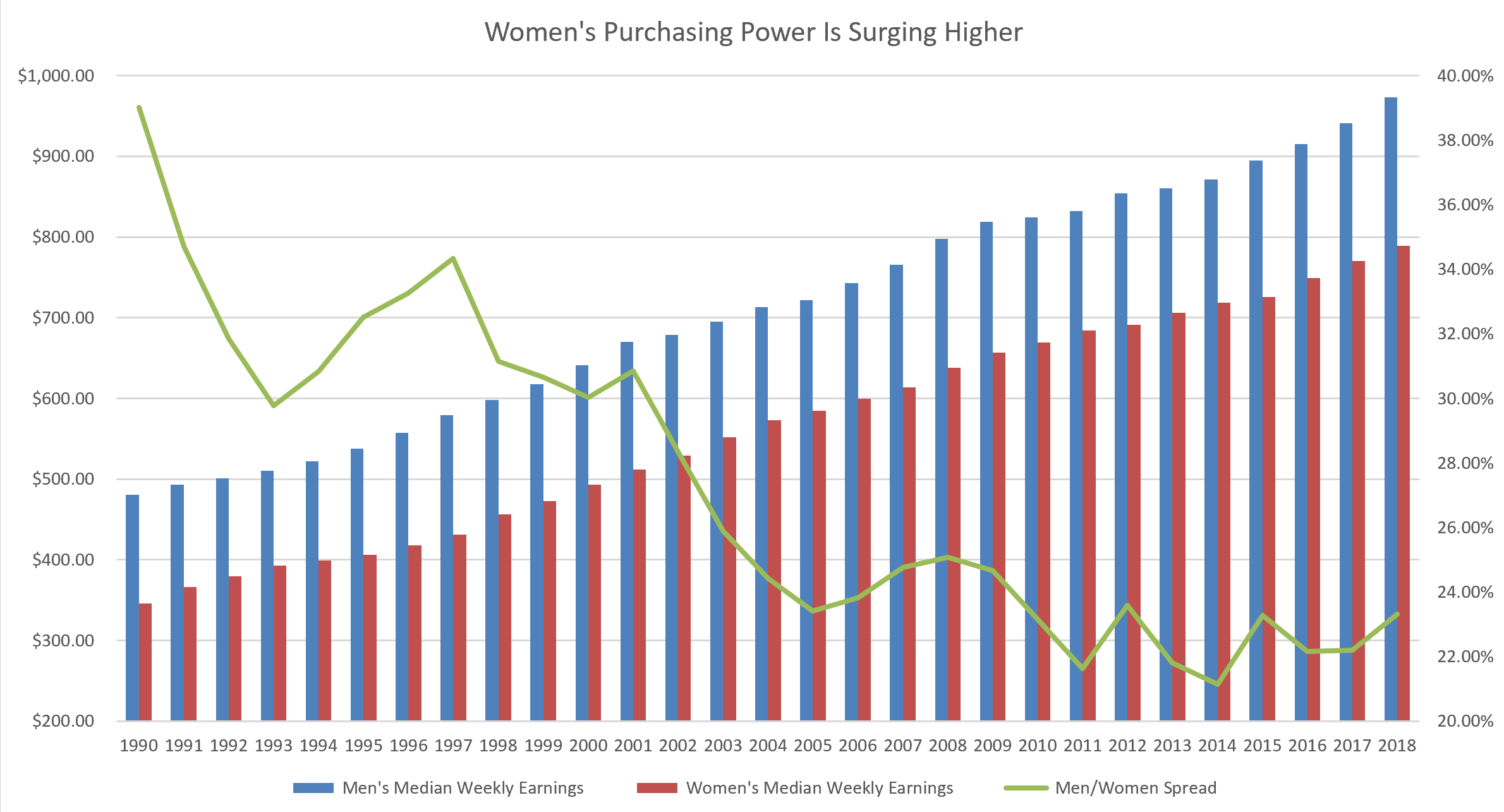

Click to Enlarge - Women’s purchasing power is growing. Weekly average earnings for women in the U.S. have grown at a 3% CAGR since 1990 (versus 2.5% for men), while women have gone from earning 30% less than men in the 1990s, to ~25% less in the 2000s, to ~22.5% less in the 2010s.

In other words, these are three secular demographic trends that have been in play for nearly three decades. They will remain in play for the next several decades, too, given current societal constructs pushing towards greater gender equality and female empowerment.

As such, the SHEconomy will continue to be the “growth” part of the U.S. economy for the foreseeable future, and will provide meaningful tailwinds for companies that female consumers love.

With that in mind, here’s a list of eight SHEconomy stocks to buy to play this demographic mega-trend, according to Morgan Stanley.

Lululemon (LULU)

One of Morgan Stanley’s top SHEconomy stocks to buy is Lululemon (NASDAQ:LULU), and I couldn’t agree more with this pick.

Anyone who knows the athletic apparel market will tell you that women everywhere are obsessed with Lululemon. Why? It’s a fashion statement item in the athletic apparel space. Basically, it’s that brand in the athletic apparel space that is the perfect combination of expensive and superior quality to where if you wear it, you’re cool.

Don’t believe me? Believe Piper Jaffray’s bi-annual Taking Stock With Teens Survey, which has consistently found over the past several years that Lululemon is one of the — and often, the single most — in-demand clothing brand among young female consumers. Or, better yet, believe Lululemon’s comparable sales growth rates, which above consistently north of 10% for the past several quarters now.

In other words, Lululemon is one of the SHEconomy’s most-beloved brands, and the numbers support this. SHEconomy tailwinds should continue to propel Lululemon’s revenues and profits higher over the next several years, which should in turn lead to big gains for LULU stock.

Nike (NKE)

Another one of Morgan Stanley’s top SHEconomy picks that I 100% agree with is Nike (NYSE:NKE).

Sure, Lululemon is the coolest athletic apparel brand for women. But, Nike is a close second, and Nike is often way more affordable and accessible. Plus, Nike dominates in the athletic performance market, including in the ultra-valuable women’s soccer and basketball markets where Lululemon has no presence.

More than being a popular brand among women, Nike is a very smart company that understands just how quickly the women’s athletic apparel market is growing. That’s why they are doubling down on the women’s market.

In other words, Nike is not just naturally levered to benefit from SHEconomy expansion, but will doubly benefit from said expansion because management is focused on optimizing the women’s opportunity. This combination sets the company up nicely for big revenue and profit growth over the next several years, the sum of which should power NKE stock higher.

Ross Stores (ROST)

Morgan Stanley thinks the SHEconomy will create sizable tailwinds for discount retailers, and in that group, it names Ross Stores (NASDAQ:ROST) as one of its favorite stocks.

I also fully agree with this pick. All consumers love a good discount. Women consumers are no different. Whether they are looking for a last minute dress, want to upgrade their wardrobe on a budget, or are looking for cute, small house decorations, female consumers are constantly finding reasons to visit Ross Stores.

The bull thesis on ROST, though, is that this isn’t just a girl thing. Guys love Ross, too, whether it be for a last-minute shirt, new shoes or new ties, they also are constantly finding reasons to visit Ross Stores.

That’s why — amid the turbulent retail environment that has persisted for most of this decade — Ross Stores has reported largely positive comparable sales growth with healthy margins and strong profit growth. In response, ROST stock has risen 800% — yes, 800% — over the past 10 years.

This trend of operational and stock price out-performance will persist. As such, not only is ROST stock a great SHEconomy stock to buy, but it’s also a great retail stock to buy.

TJX Companies (TJX)

In the discount sector, Morgan Stanley thinks that TJX Companies (NYSE:TJX) will similarly benefit from SHEconomy tailwinds over the next several years, and I again fully agree.

The bull thesis here is very similar to the bull thesis on ROST. All consumers — female and male — love discounts, and are constantly finding excuses to shuffle their way into discount stores like TJX and ROST. On the SHEconomy side, though, TJX has a bigger home furnishings presence than Ross Stores, and this larger home furnishings presence more broadly exposes it to SHEconomy tailwinds over the next several years.

So, while I like both ROST and TJX as SHEconomy stocks to buy over the next several years, I like TJX slightly better for its broader home furnishings exposure.

Much like ROST, TJX has reported largely positive comparable sales growth for several years, alongside healthy margins and big profit growth. This has led to strong stock price performance, with TJX stock up over 500% over the past decade. All of these dynamics will persist — big revenue growth, big profit growth and big share price gains — meaning TJX stock is a great stock to buy and hold for the long run.

Ulta (ULTA)

What would this list be without including beauty retail giant Ulta (NASDAQ:ULTA)?

Perhaps one of the more obvious choices on this list, Ulta is naturally set to benefit from SHEconomy tailwinds because what they sell — cosmetics — is exactly what women spend a ton of money on. Indeed, according to a Groupon survey, women spend about 25% more than men on beauty products and services.

Also helping Ulta is the fact that an overwhelming majority of its consumers skew young, meaning that these are the consumers who are going to be earning incomes (and spending money) for a lot longer. Ulta seems supported by multiple favorable demographic trends, all of which seem to have long runways.

Given these circumstances, Ulta looks positioned to grow revenue and profits at a fairly robust rate for the foreseeable future. At 25-times forward earnings, ULTA stock is priced for some of this growth — but not all of it. As such, this stock has compelling multi-year upside from current levels.

Chipotle (CMG)

Morgan Stanley included two restaurant stocks in its list of SHEconomy stocks to buy. The first of those restaurant stocks is Chipotle (NYSE:CMG).

I get the thesis here. Consumers are increasingly obsessed with eating healthy, especially female consumers. Chipotle dominates in the restaurant overlap of healthy and affordable. As such, the company has ample exposure to SHEconomy tailwinds over the next few years and those tailwinds — coupled with other tailwinds, like digital business expansion, new menu innovations and unique marketing campaigns — should drive robust revenue and profit growth, the sum of which should propel CMG stock higher.

That all makes sense. But, that thesis misses the biggest point about CMG stock: it is the most richly valued restaurant stock out there. The stock trades at over 60x forward earnings. That’s right. With CMG stock, you have a restaurant stock trading at more than three times the S&P 500 index forward earnings multiple.

Sure, bulls will argue that the premium valuation is warranted by big profit growth potential, which is powered by strong comps and a huge recovery in margins. I understand that. I also understand that analysts are modeling for ~20% EPS growth in the long run and that lines up with my modeling, too. A 60x forward earnings multiple for about 20% EPS growth just seems like too much.

As such, while I get the qualitative SHEconomy bull thesis here, I don’t think the numbers add up.

Starbucks (SBUX)

The second SHEconomy restaurant stock Morgan Stanley recommends to buy is Starbucks (NASDAQ:SBUX). But, much like CMG stock, I don’t agree with a “Buy” rating on SBUX stock.

Here’s the thing with Starbucks: They are caught between a rock and a hard place long term. Right now, they dominate the retail coffee game, and they do so at high prices. That’s rare. Normally, consumer-facing markets have the market share leaders (which have big market shares because of their low prices) and the premium players (which have small market shares because of their high prices). Think groceries, with Kroger (NYSE:KR) versus Whole Foods. Or think fast food, with McDonald’s (NYSE:MCD) versus Shake Shack (NYSE:SHAK).

The coffee retail market is an exception to this trend. For now. Over time, it will start to look like all those other markets. Indie coffee shops will enter at premium price points and dominate the high-end of the market. Fast casual chains like McDonald’s will expand their breakfast offerings and dominate the low-end of the market. In that world, where is Starbucks? Somewhere in the middle — and I’m not convinced the middle ground will be as big as everyone seems to think it will be.

As such, the current 35-times forward earnings multiple on SBUX stock seems way too high to me. I don’t see this company as much more than a 10-15% profit grower in the long run. That’s pretty much the market-average EPS growth rate, and the market trades at 15x, not 35x, forward earnings.

Tesla (TSLA)

Last, but not least, on Morgan Stanley’s list of SHEconomy picks is premium electric vehicle manufacturer Tesla (NASDAQ:TSLA).

I agree with this pick. But not for the SHEconomy demographic tailwinds. Rather, for the Generation Z demographic tailwinds. In the Generation Z demographic, the most talked about, popular, and relevant car brand is Tesla — and it’s not close. According to TotalSocial data, teens are talking about car brands less and less on social media, with one notable exception — Tesla, whose daily social mentions rose more than 100% from 2013 to 2018.

Tesla is the car brand of choice for most young consumers. That’s important, because those young consumers are in the process of growing up. Soon, they’ll be earning steady incomes, which will give them enough purchasing power to buy their own car. When they do that, chances are pretty high they will buy a Tesla, given their infatuation with the brand relative to other auto brands.

Net net, Tesla seems poised to benefit from demographic tailwinds which will increase the company’s market share in the auto market dramatically. As that happens, revenues, profits, and the stock price will all move higher in the long run.

As of this writing, Luke Lango was long LULU, NKE, TJX, KR, MCD and TSLA.