Even if you’re more of a short-term thinker when it comes to investing, it’s still a good idea to put some money into blue-chip stocks that have been around forever and will likely be around forever into the future. Many stocks these days can fizzle out soon, and most of the hot new tech names today probably won’t stand the test of time like firms that have been steady performers for generations. Time is the real boss, and not many businesses can stay on top indefinitely.

On the other hand, companies with deep roots and proven staying power are very unlikely to go anywhere in the next 50 to 100 years. Their stock prices will probably keep growing along with the overall economy for years to come. So, putting a little cash into those reliable old standbys gives your portfolio a solid backbone for the long haul. You’re betting that society and markets will keep chugging ahead century after century.

So, let’s check out seven of those time-tested blue-chip stocks to buy and hold that could anchor part of your investments for the next 50 years or more. Their track records through good times and bad says a lot about how they’ve adapted over the decades.

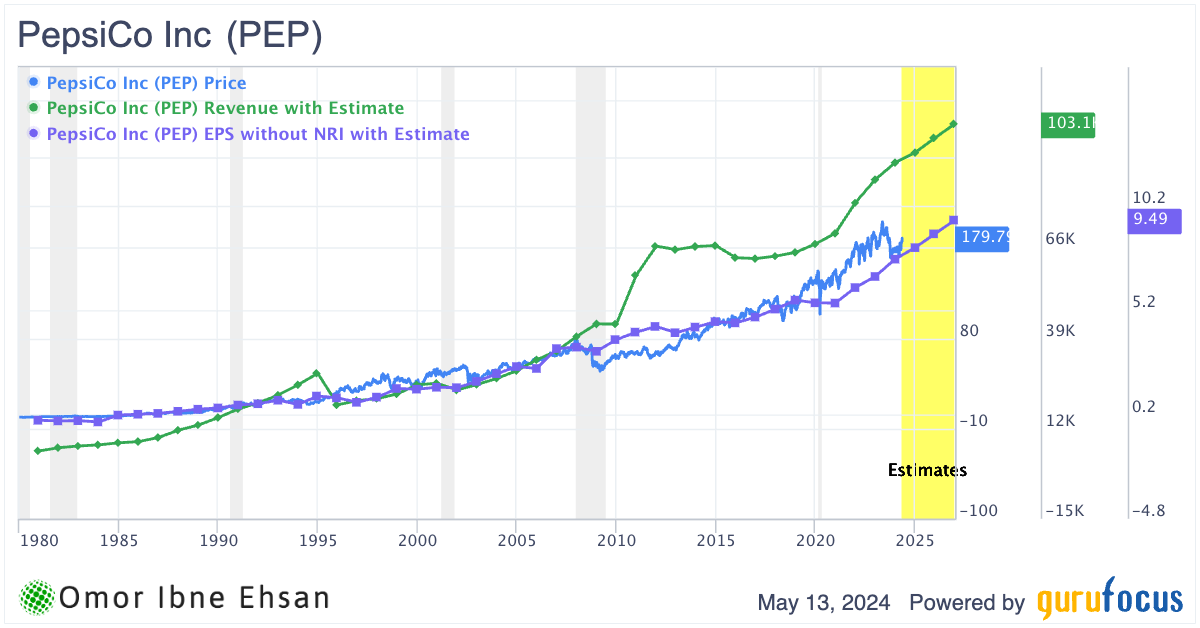

PepsiCo (PEP)

PepsiCo (NASDAQ:PEP) kicked off 2024 with a strong first quarter. Revenue rose nearly 2.3%, fueled by robust pricing actions across its portfolio. The snack and beverage giant showed its ability to push through price hikes without significantly denting volumes. Its brands hold considerable pricing power, and consumers are willing to pay up for marquee offerings like Lays, Doritos and Pepsi Cola.

PepsiCo also benefited from rebounding foot traffic as consumers returned to pre-pandemic routines. However, the stock did underperform, much like many other retail and consumer staples stocks. I think it is unlikely to go down from here unless there is a broad downturn, and buying now is likely a good idea before it recovers.

PepsiCo reiterated full-year guidance, calling for 4% revenue growth. You should also watch operating margins closely, as the company laps last year’s dramatic cost inflation.

Click to Enlarge

It’s a mature company you should sit back and let it compound for the coming decades. The dividend yield here is over 3%, and it is also a Dividend King. It’s definitely one of the top blue-chip stocks you can buy.

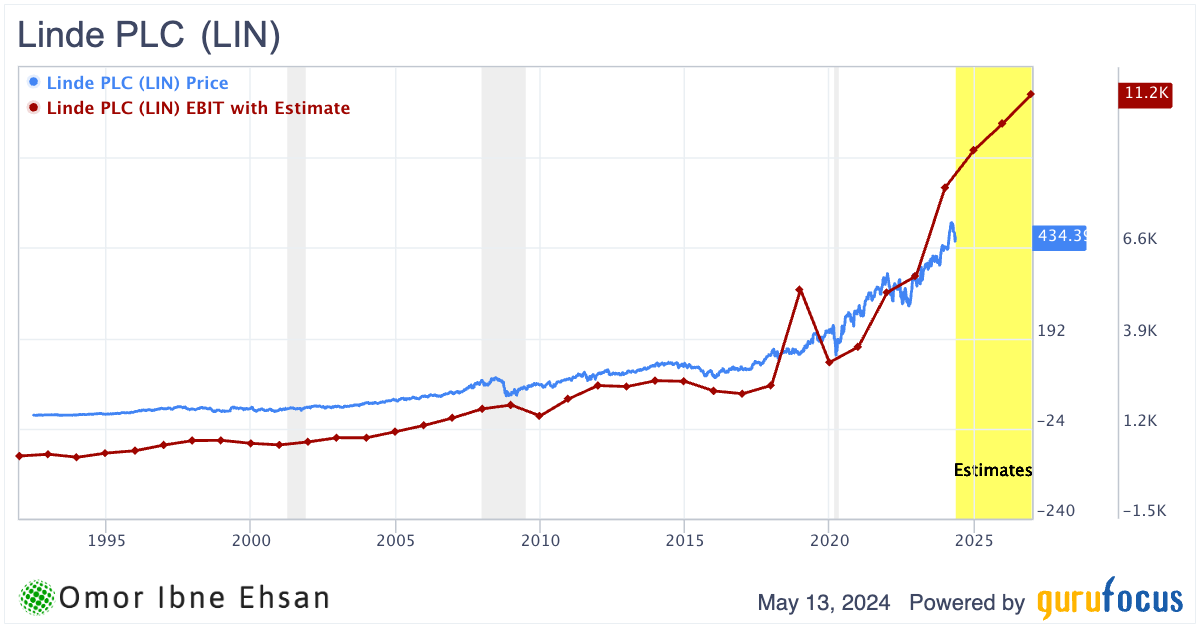

Linde (LIN)

Industrial gas supplier Linde (NASDAQ:LIN) delivered another rock-solid quarter. EPS jumped 9.5% year-over-year (YoY) as the company pushed through higher prices. However, revenue declined slightly by 1.14%.

Linde stands apart through its incredible cash generation and operating discipline. Management also provided EPS guidance of $15.30 to $15.60 for the period, compared to the consensus earnings per share estimate of $15.41. Thus, I think the stock could continue climbing due to solid earnings growth.

Click to Enlarge

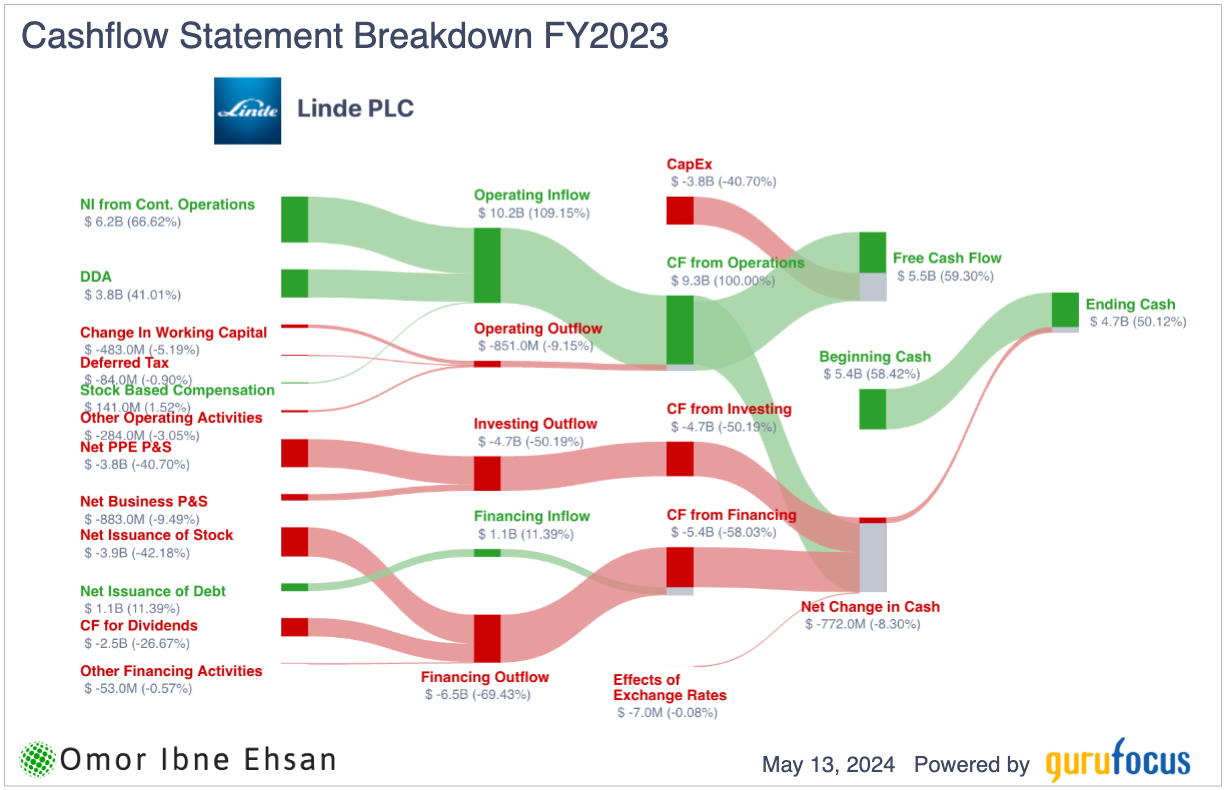

The company remains a defensive cash flow compounder levered to secular growth drivers like clean energy transition initiatives.

Click to Enlarge

Linde’s pricing power and cost control should help navigate any potential economic turbulence ahead.

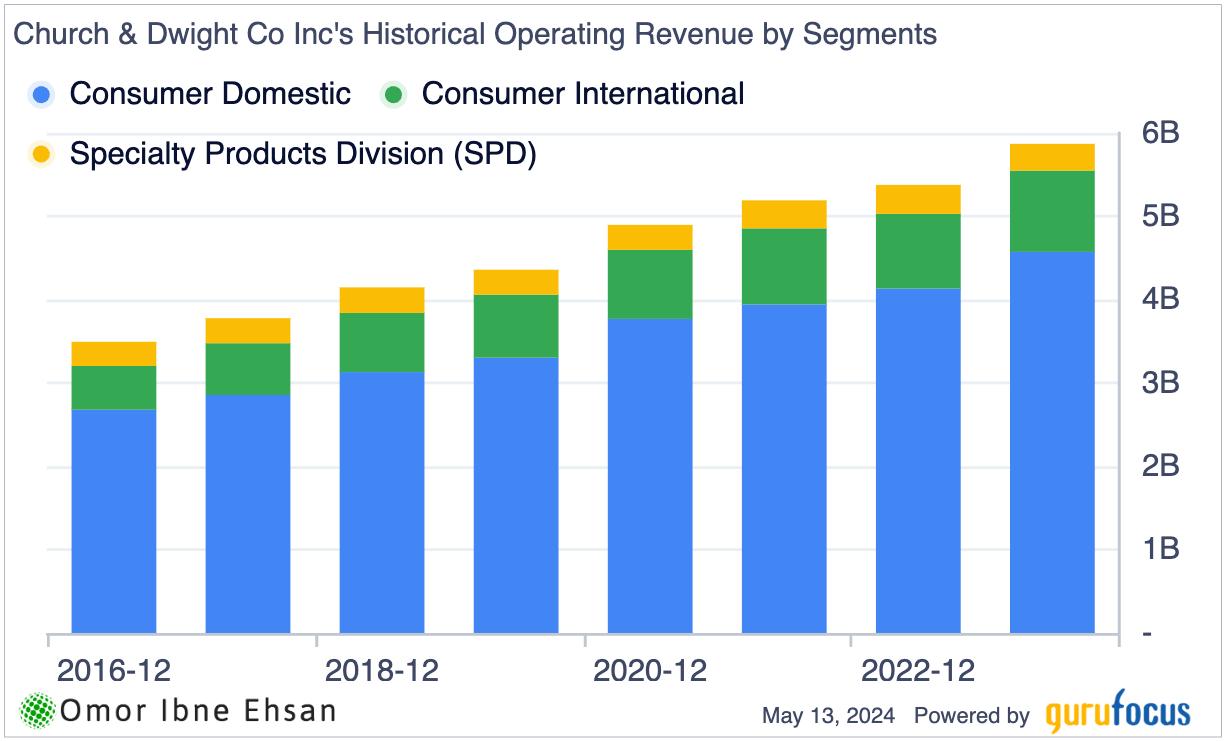

Church & Dwight (CHD)

It was a mixed bag for Church & Dwight (NYSE:CHD) in Q1. The consumer products maker posted 5.1% sales growth, exceeding the 4% guidance.

However, Church & Dwight is swimming against stiff currents as consumers turn increasingly cost-conscious. Brands like Arm & Hammer and OxiClean face intensifying private label competition. Still, the metrics were strong in household and personal care categories due to new launches.

The SPD segment has continued to remain flat and has actually declined in recent quarters.

Click to Enlarge

However, new offerings like Arm & Hammer bathroom cleaners (core consumer) and Batiste dry shampoo (specialty) are gaining traction, with consumption up 19% in Q1 and a growing share of 47.5%. That could drive a lot of growth in the future.

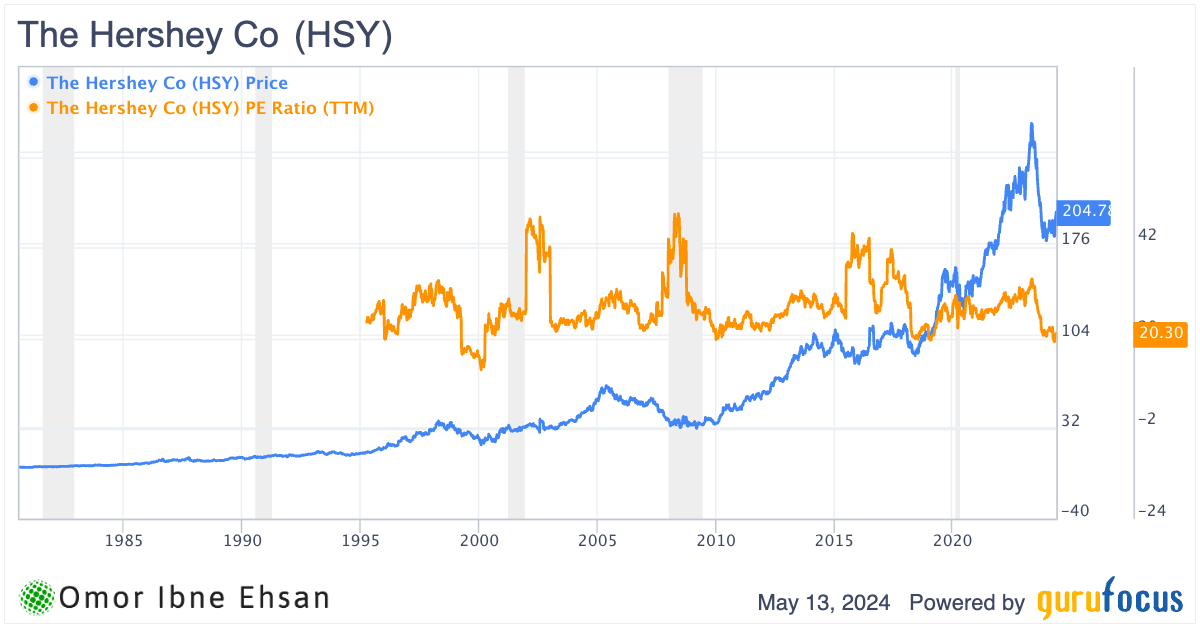

The Hershey Company (HSY)

Chocolate maker Hershey (NYSE:HSY) enjoyed a delicious first quarter, beating estimates on both the top and bottom lines. The Easter and Valentine’s Day seasons delivered a solid sales boost as Hershey’s seasonal chocolate offerings flew off shelves. Innovations like Reese’s Peanut Butter Caramel Cups and strong merchandising support boosted market share.

Within the core confectionery portfolio, Hershey appears to be gaining pricing traction compared to recent share softness. Management expects volume trends to improve throughout the year as consumer elasticities recover from last year’s price hikes. Retailers are also granting more display space and promotion support after last year’s inventory flow issues.

Click to Enlarge

The stock itself is down over 25% in one year, but a rebound is underway, and I think buying the stock at a discount now will set you up for juicy gains in the decades ahead.

Operating margins compressed due to high input costs and trade investments. However, Hershey remains confident that stronger productivity savings in the latter half will help offset pressures. It is one of the most discounted blue-chip stocks right now.

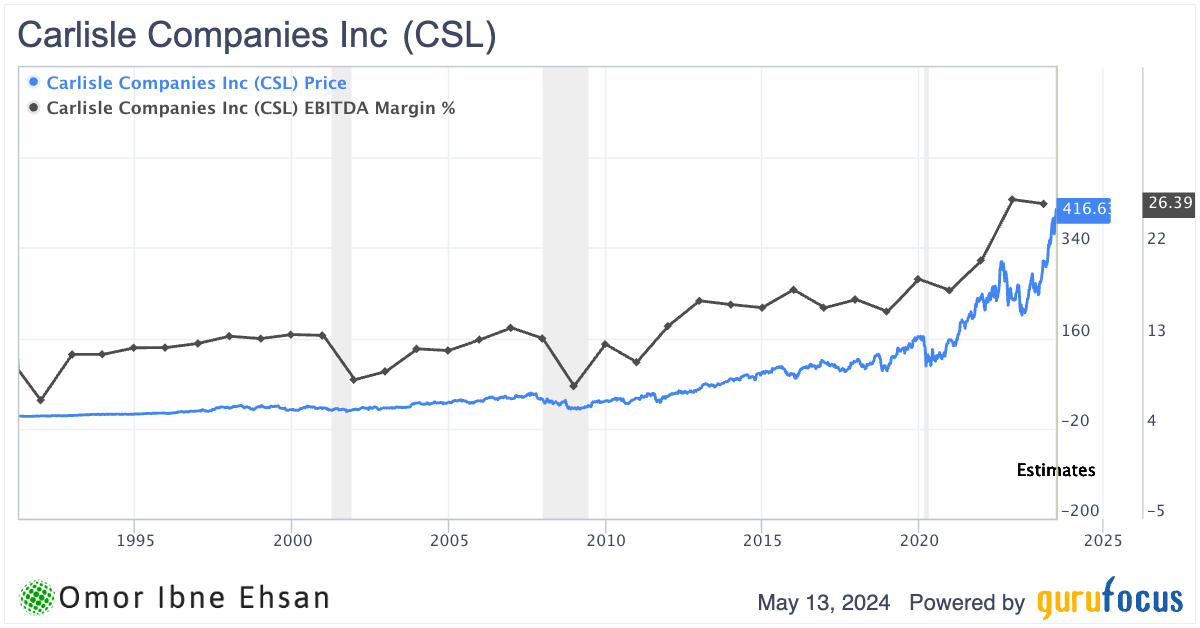

Carlisle Companies (CSL)

Carlisle Companies’ (NYSE:CSL) sales grew strongly again after slowing for a bit, surging an excellent 23% YoY in Q1. It’s also encouraging that pricing seems to be holding steady despite rising costs across the industry.

What I truly admire about Carlisle is its world-class operations relying on the Carlisle Operating System approach. The COS method is really paying dividends — the company lowered expenses so much while increasing production that margins jumped over 530 basis points to 24.2%. That led to earnings growing by 85% per share after adjusting for special items.

I’m confident Carlisle can keep growing revenues and profits by strong double-digit percentages. Factors like long-awaited roof replacements, a hot housing market and continued refinements should fuel the momentum. It seems they also have an advantage as others raise prices, too.

Click to Enlarge

However, what excites me most is where they’re taking the company long-term. When the CEO outlined the strategy shift towards pure-play building products through strategic deals and integrated offerings, it made a lot of sense. The planned MTL buy fits perfectly to strengthen its lead in architectural metals while enhancing value. Selling off Carlisle Interconnect Technologies will also generate about $2 billion to invest and create even more shareholder wealth.

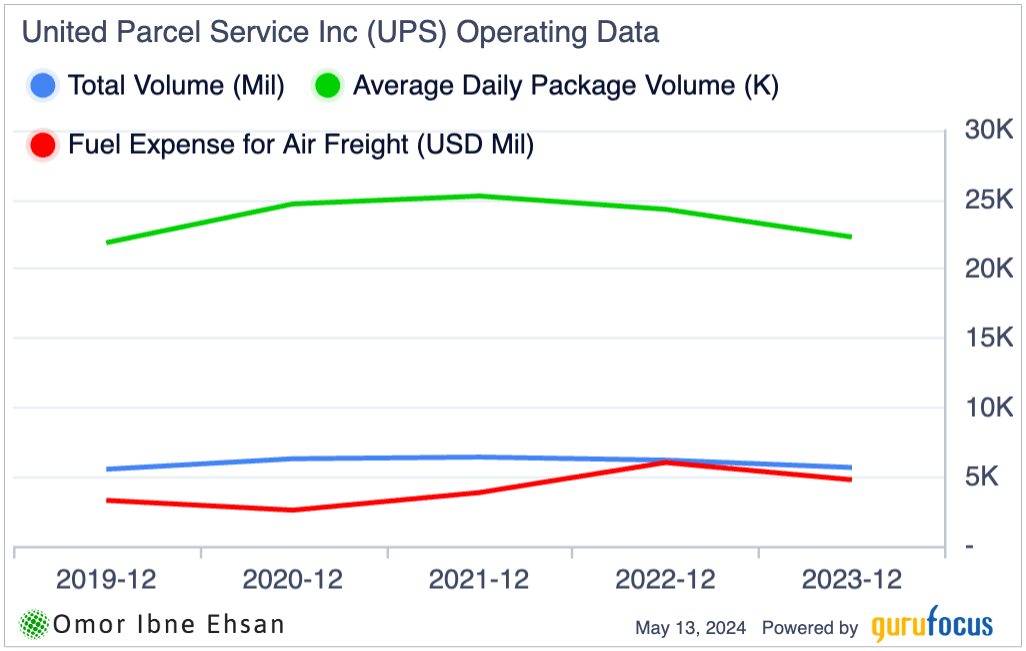

United Parcel Service (UPS)

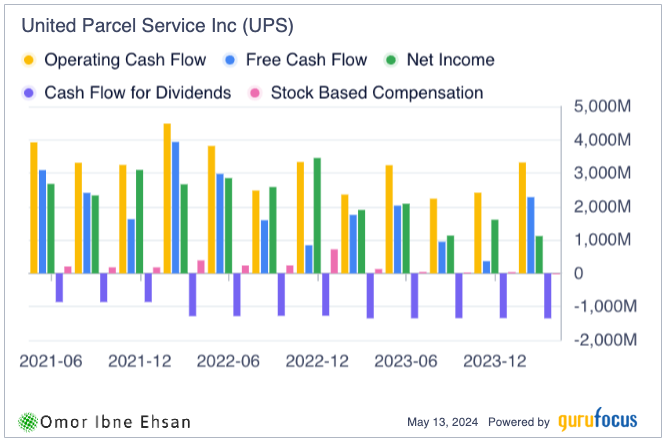

United Parcel Service (NYSE:UPS) did not have the best quarter, but I still think it’s a good long-term bet. The average daily package volume was down by 3.2%. Revenue came in at $21.7 billion, down 5.3% YoY, and missed analyst expectations by $232 million.

Click to Enlarge

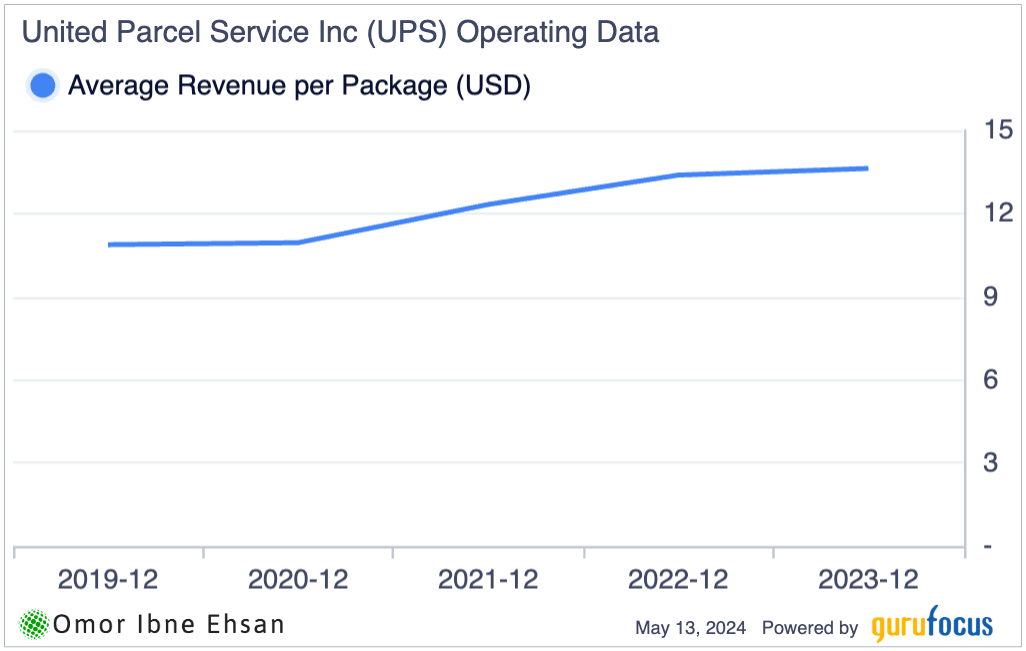

Despite the decrease in package volume, revenue per package has held up quite well.

Click to Enlarge

The tighter margins did make me pause, though, with operating profits down 31.5% from the previous year. The company shed some 5,400 management positions but it wasn’t entirely offset. Still, as pricing moves take hold, I expect to see expenses turn around sharply. With less spending and more leverage from experience, profits should strengthen meaningfully going forward.

Cash flow has already started to improve on a quarterly basis.

Click to Enlarge

Regardless, this iconic delivery company is well set up to drive compounding earnings, and we can overlook near-term worries if we are talking about decades. At the current valuation, the stock looks fair compared to the quality of the business and market position. The 4.42% dividend yield is why I think jumping on board is worth it. It is one of the highest-yielding blue-chip stocks you will find.

Alamo Group (ALG)

First off, Alamo Group’s (NYSE:ALG) top-line growth of 3.4% to $425.6 million is impressive given the challenging demand in Vegetation Management — its largest division. Industrial Equipment shined with a 30% revenue spike, buoyed by robust government and infrastructure markets. However, Vegetation Management slumped, with a 13% sales drop due to higher rates constraining forestry and agricultural equipment purchases.

However, management’s capacity rightsizing efforts are preserving profitability. EPS of $2.67 beat by 14 cents despite the headwinds. Revenue also surprisingly beat by almost $15 million. Analysts seem quite bullish now.

Click to Enlarge

Plus, the backlog of $831 million provides solid visibility, even after dropping 16% YoY. With a 1.3x bank leverage ratio and $246 million trailing EBITDA, the balance sheet remains sturdy to pursue M&A. All things considered, while a choppy road likely persists in the near future, I see Alamo emerging stronger as rates eventually subside and demand normalizes.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.