The Magnificent 7 stocks have continued to dominate the market, and while I think you should buy into those, there are also many other good stocks you should consider for a perfect portfolio. As the legendary Charlie Munger once advised his partner, Warren Buffett, it’s wise to buy wonderful businesses at fair prices instead of the other way around.

However, Big Tech plus Nvidia (NASDAQ:NVDA) and Tesla (NASDAQ:TSLA) aren’t the only “wonderful” businesses out there. If I were to pick only seven perfect portfolio stocks, I would include just one from the Mag 7, complementing it with a diverse basket of quality businesses that’ll set the portfolio up for good performance in the coming decades.

Here are the only perfect portfolio stocks you’d need.

Berkshire Hathaway (BRK-A, BRK-B)

If you haven’t figured it out from the Munger quote already, I’m a big Berkshire Hathaway (NYSE:BRK-A, NYSE:BRK-B) fan. This is especially true nowadays due to the uncertainty about when rate cuts are going to come. The company simply has a lot of flexibility that other companies don’t. And if you’re building a perfect portfolio, buying up another near-perfect portfolio is a good idea.

Berkshire Hathaway has a boatload of cash ready to invest if there is a downturn, and if there isn’t, it has plenty of exposure to quality businesses. Investor confidence in Warren Buffett is as solid as ever, and you can see that with how much better the stock has performed compared to other asset managers.

I have no doubt Berkshire Hathaway will continue to outperform the benchmark S&P 500 moving forward.

Microsoft (MSFT)

Microsoft (NASDAQ:MSFT), along with Berkshire, should give you more than enough tech exposure. This is my favorite tech company, as the white-collar sector won’t survive without it. People may make do without any other Big Tech company, but Microsoft has made itself essential, especially with its smart AI investments.

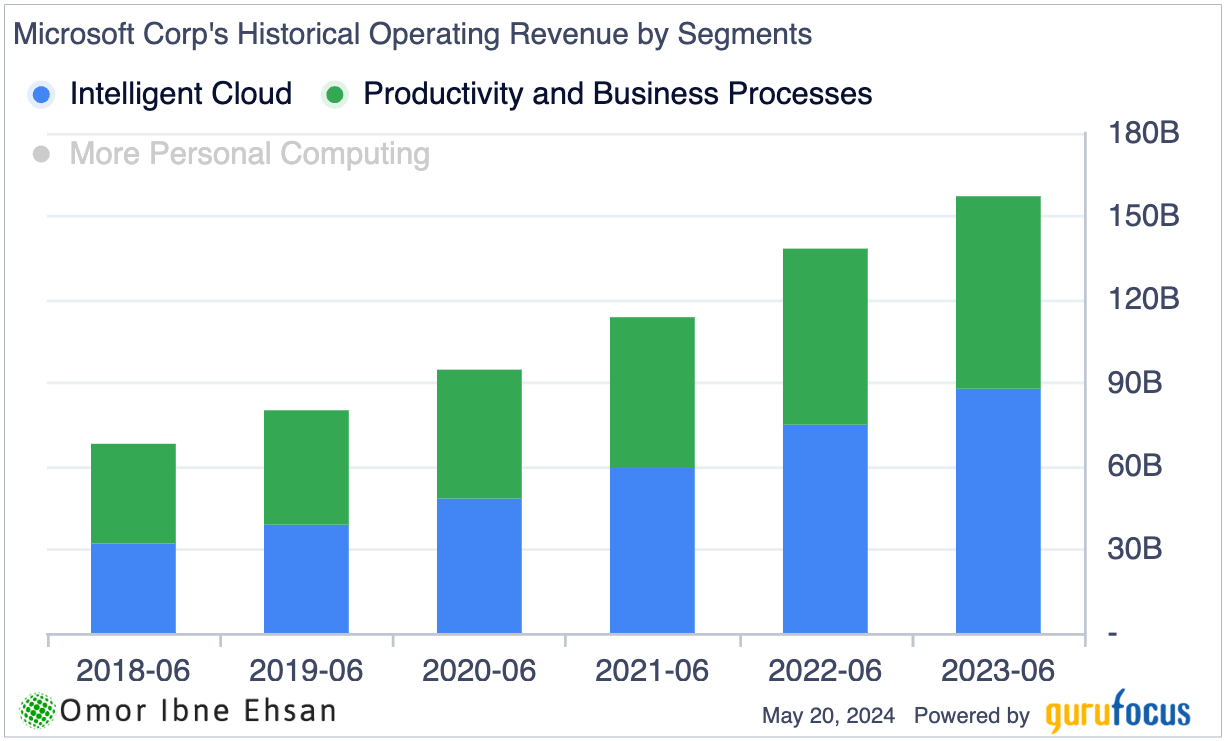

The company reported highly positive quarterly results, surpassing projections on both revenue and earnings. Total revenue grew 17% to reach $61.9 billion, fueled by a 23% rise in Microsoft Cloud revenues to $35.1 billion.

Revenue from Azure rose 31%, with AI-related services accounting for approximately 7 points of that increase. Remove the Personal Computing segment, and the revenue trend here has been very solid.

Click to Enlarge

Positive signs for Microsoft’s ongoing digital transformation were reinforced by a 29% increase in bookings, driven by longer-term commercial commitments to Azure. This suggests that its “cloud flywheel” of mutually reinforcing cloud and AI businesses is working. The 0.71% yield sweetens the deal.

Itochu (ITOCF)

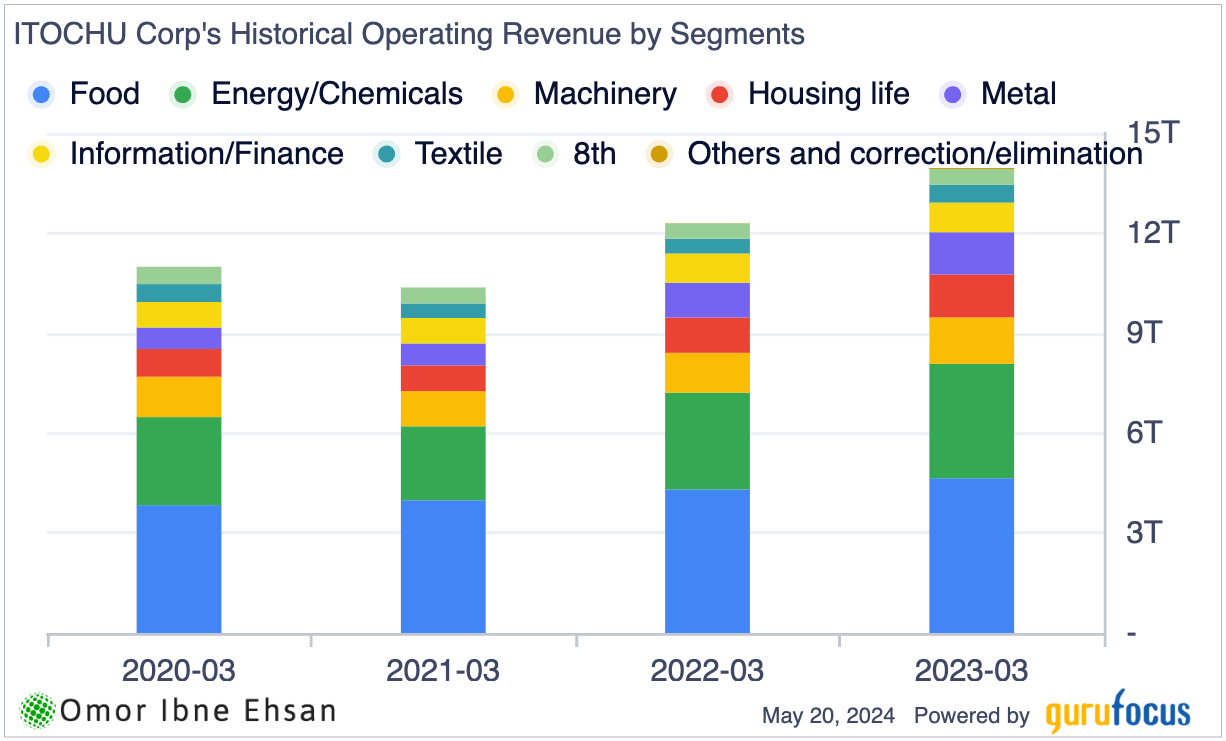

Itochu (OTCMKTS:ITOCF) is not that well-known, but it is a very well-diversified company that I think deserves more attention. I believe it is the Berkshire Hathaway of Japan. The diversification here is some of the best you can find in one business.

Click to Enlarge

However, near-term trends haven’t been the best. Management did report positive growth in FY2024, with revenues increasing slightly by 0.6% and net income growing marginally by 0.2%. Unfortunately, Itochu’s Energy & Chemicals segment experienced double-digit declining revenues because of lower prices.

However, I don’t see any long-term problems here. The yen’s devaluation is causing near-term problems, but the stock’s performance shows that investors remain confident Itochu will keep compounding.

It has been a very stable company. Plus, the dividend is scheduled to rise to a record high of 200 yen per share, but the payout ratio will be a modest 32.5%.

Procter & Gamble (PG)

Procter & Gamble (NYSE:PG) is a consumer goods giant known for brands like Tide, Bounty and Pampers. The stock will act as a great ballast for your portfolio, as Procter & Gamble has a very sticky demand for its products.

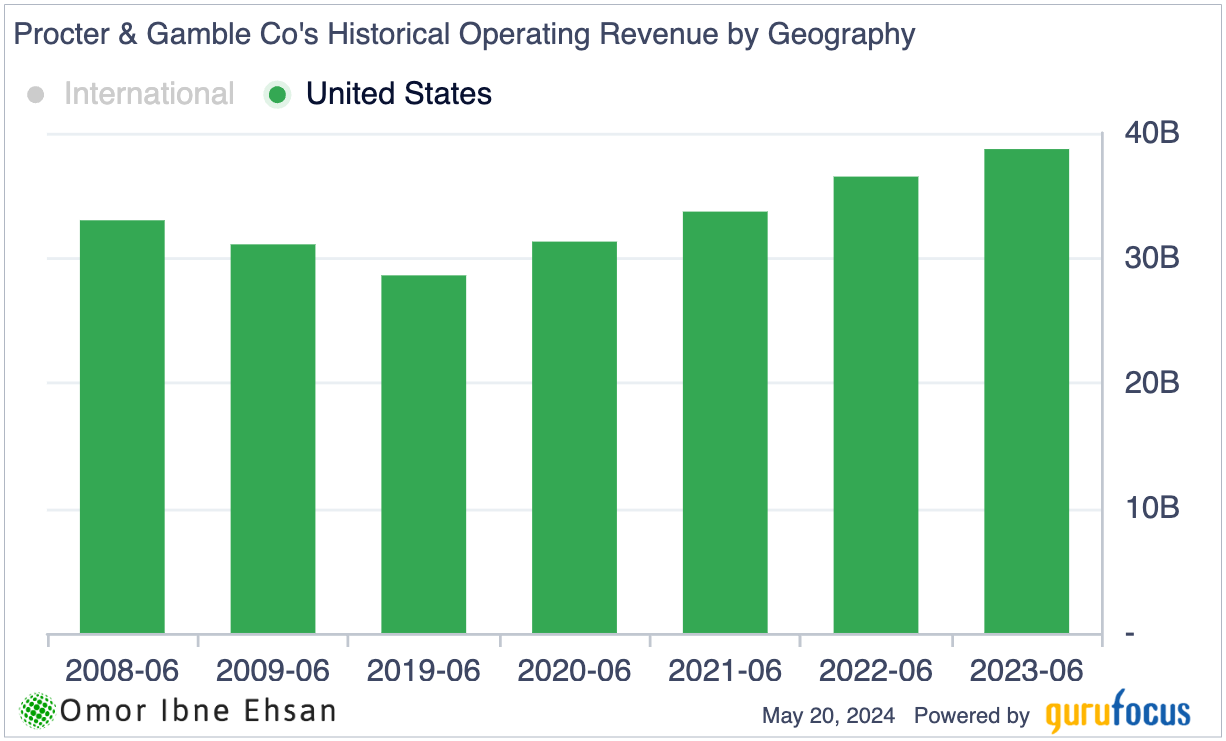

Its earnings per share of $1.52 was above analysts’ estimates, up 11% year-over-year (YOY). However, PG’s total revenue of $20.2 billion missed Wall Street’s forecast by $241 million.

Results took a hit from the weakness seen in China, where business was down 10%. On a more positive note, the United States market stayed very strong, with consumption growing by 5% and P&G gaining additional market share.

Click to Enlarge

Management adjusted their prediction for higher full-year earnings, and they are now expecting growth in the range of 10% to 11%. This is enabled by expense savings, allowing over 300 basis points of margin expansion. The company’s guidance for organic sales growth through the end of the fiscal year was left at 4% to 5%, disappointing some investors who may have been hoping for an increased projection. While near-term headwinds from places like China are ongoing issues, Procter & Gamble’s overall strategy is still seen as on the right track.

Pressure on the top line appears to be slowing its momentum somewhat, but this is a surefire long-term bet for any perfect portfolio. The dividend yield is at a solid 2.4%.

Linde (LIN)

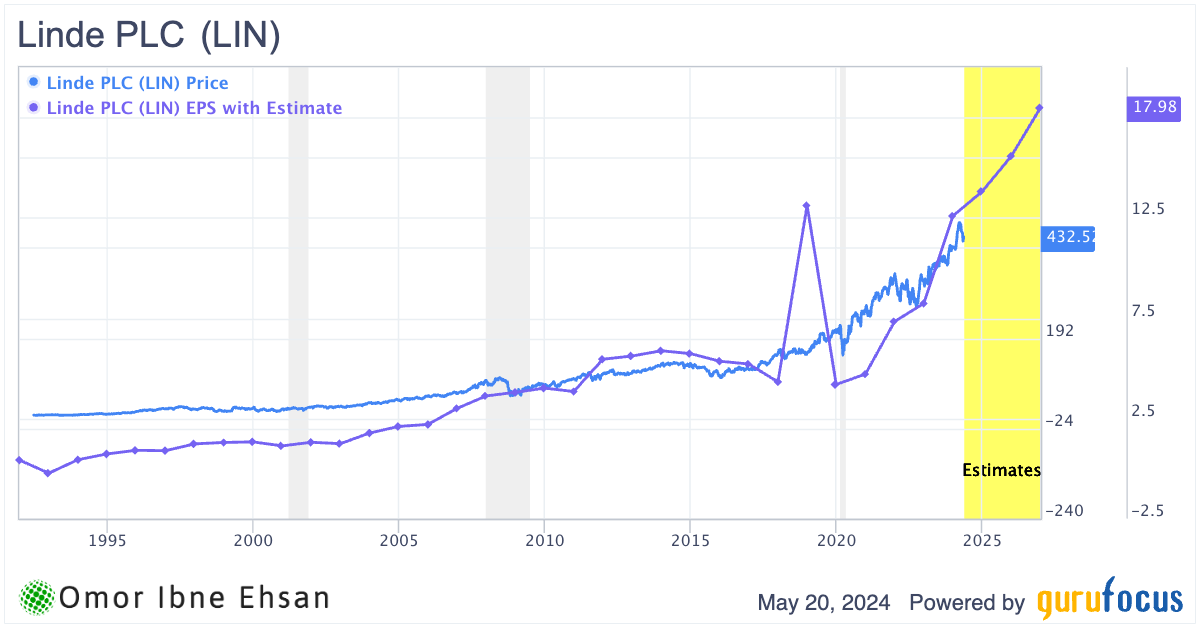

Linde (NASDAQ:LIN) is a German chemical company. It also had a mixed earnings season, and its Q1 result was similar to that of Procter & Gamble. EPS beat, but revenue missed.

Earnings per share grew 10% to reach $3.75, benefiting from higher prices and good cost management. Operating margins set a new record at 28.9%. However, total sales declined by 1% as volumes fell by 1% due to weak industrial activity in Europe over the past few months. However, long-term trends look very promising.

Click to Enlarge

Management expects demand to remain sluggish for now, particularly in Europe. They do not see any changes on the immediate horizon that would spark a global industry recovery. As a result, management has reaffirmed its full-year EPS guidance from $15.30 to $15.60. That’s still an 8% to 10% growth.

The company also has a $5 billion backlog to work with. Linde seems well-positioned to deliver continued mid-single-digit EPS expansion over the long run. The stock is down ~8% from its March high, and I think buying the dip is a good idea. There’s also a 1.3% dividend yield here.

O’Reilly Automotive (ORLY)

O’Reilly Automotive (NASDAQ:ORLY) has experienced some softening after a disappointing Q1. Revenue did not meet expectations due to unpredictable demand from do-it-yourself consumers impacted by delays in tax reimbursements and inclement weather. Earnings per share of $9.2 also lagged the estimated targets. However, it was missed by a hair on both the top and the bottom line — an 11 cents EPS miss and a revenue miss of less than $5 million.

Management maintained the full-year sales guidance, calling for a 3% to 5% comparable stores growth rate, though EPS guidance was a bit below expectations. Executives anticipate sales patterns will stabilize as weather conditions return to a more typical pattern. Demand for fundamental automotive supplies like oil and filters appears to be holding steady.

The average car on the road is approaching 13 years old, and that aging fleet is only going to bring more business with time. Analysts expect EPS to grow from $42 to $112 from 2024 to 2033.

Click to Enlarge

Buying the dip seems wise.

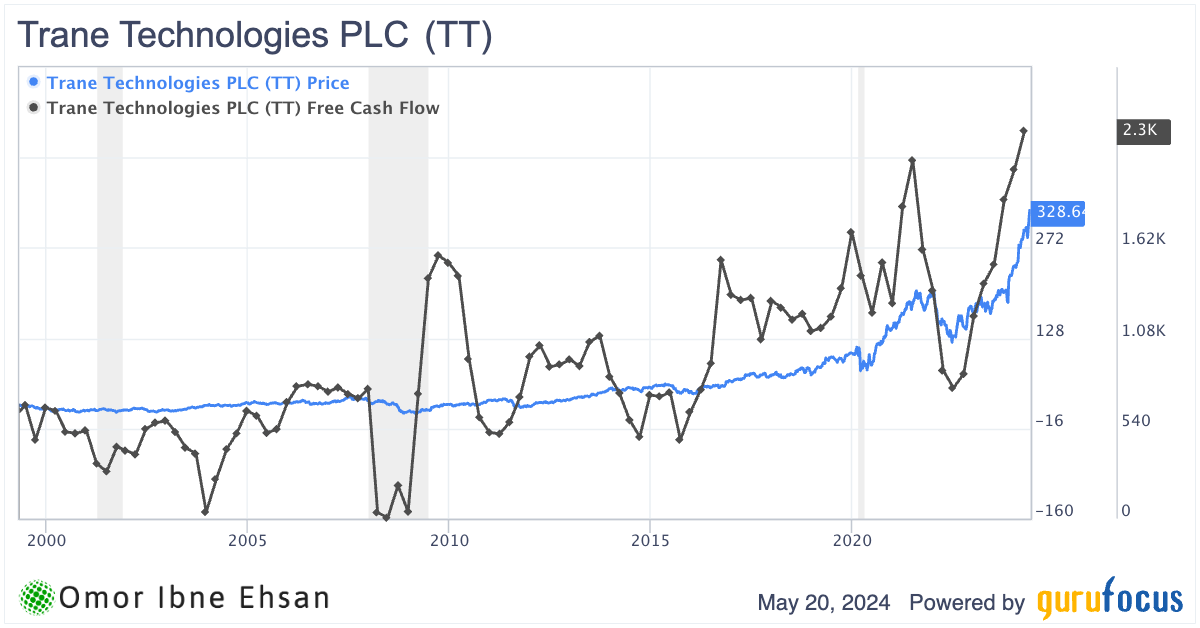

Trane Technologies (TT)

Trane Technologies (NYSE:TT) is mainly an HVAC company. We’re seeing hotter and hotter summers, and this trend is having a very good impact on the company’s coffers.

Revenue grew 15% YOY, reaching $4.22 billion. This was driven largely by HVAC solutions. Bookings rose 17% to a record $5 billion, and its commercial HVAC segment led the way with over 20% growth. The company’s order backlog increased 10% to $7.7 billion. To top it all off, adjusted EPS of $1.94 beat analyst estimates by 30 cents.

Management also raised their projection for full-year organic revenue growth. Originally estimated at 6% to 7%, they now expect 8% to 9% growth. Moreover, the stock’s current rally doesn’t seem overvalued to me due to the solid growth in cash flow.

Click to Enlarge

The strong demand Trane is seeing for its commercial HVAC solutions is allowing the company to outpace the overall market growth. While the residential market situation is less certain, the commercial strength should continue powering increases in both its top and bottom line numbers. If 2024 turns out as hot as last year, expect even more outperformance here.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.