The current market rally has been one of the strongest to date. The Nasdaq index has returned almost 20% year-to-date (YTD), and that is after it gained 37% in 2023. The S&P 500 also gained 21.9% in 2023 and is up 14.5% halfway through 2024. You may argue that the Covid-19 recovery has had a lot to do with these numbers, but even if you compare returns since Feb. 2020, the rally so far has been solid.

Nevertheless, it’s wise keep an eye out for stocks to sell. Circumstances can head south quickly, and certain businesses are in a very vulnerable position. It makes sense to trim your positions in these stocks and invest in stocks that provide more quality and value.

I’m not a doomer by any means, and I still think you should invest in solid businesses with solid fundamentals. As long as Wall Street holds up the premium as the underlying business grows, there’s not much to worry about in the long run. However, when a business is expected to slow down or is in a cyclical market, you shouldn’t let the euphoria bring your guard down.

AudioEye (AEYE)

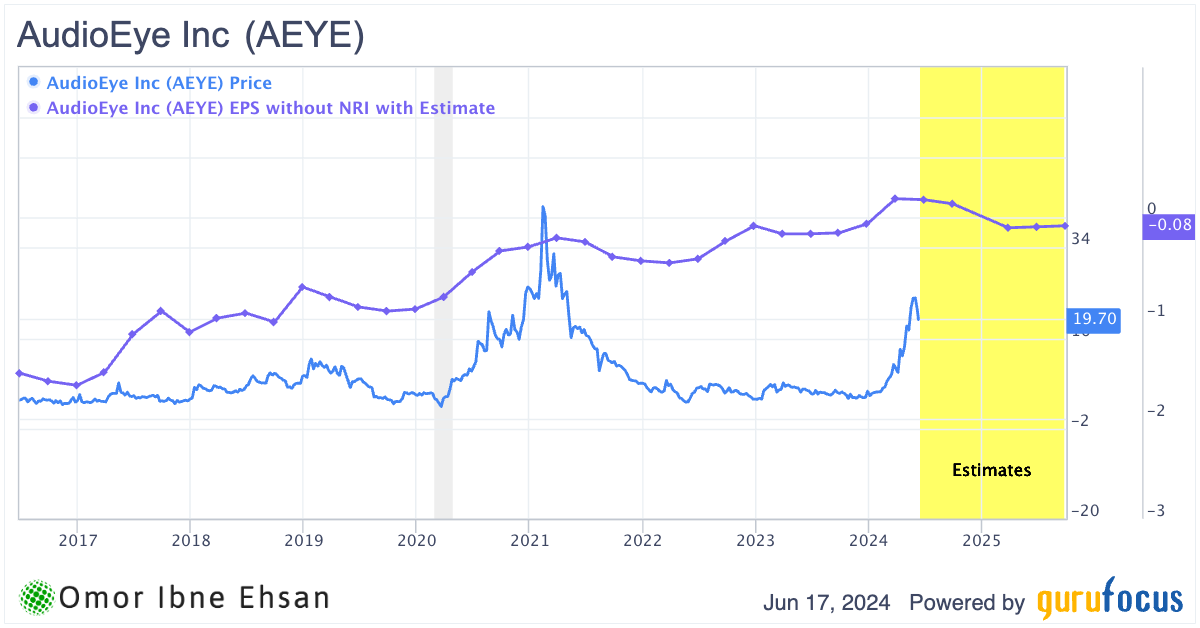

AudioEye (NASDAQ:AEYE) provides digital accessibility solutions to make websites accessible for people with disabilities. While AEYE stock has soared 254% over the past year, riding the AI hype wave, I believe the momentum is reversing, and shares could tumble much further.

The company is facing intensifying competition as bigger, smarter AI models emerge that can provide similar accessibility services for free. Look into OpenAI’s GPT-4o model, and you’ll be surprised at what it can do. AudioEye’s first quarter results were lackluster at best, with revenue inching up just 4% year-over-year (YOY) to $8.1 million. You’re paying almost 50 times forward earnings for very sluggish growth. Even EPS growth is expected to slow down.

Click to Enlarge

Management is hyping up potential tailwinds from new accessibility regulations in the U.S. and Europe. However, with AudioEye’s single-digit penetration among key reseller partners today, I’m skeptical they can fully capitalize on any demand surge. AudioEye’s first-mover advantage is rapidly eroding as the AI arms race heats up.

I think it’s prudent for investors to take some chips off the table. Trimming positions into this AI-driven euphoria seems like the best move.

Williams-Sonoma (WSM)

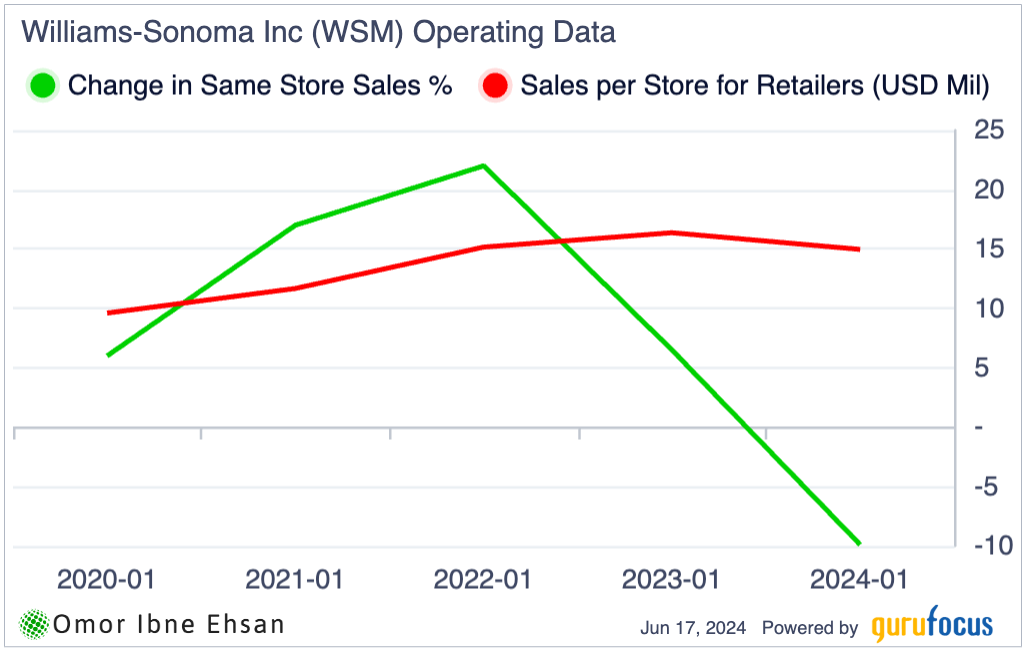

Williams-Sonoma (NYSE:WSM) is a leading specialty retailer of high-quality home products. The stock has been on an absolute tear, soaring 148% over the past year and hitting fresh highs after posting strong Q1 results.

However, the peak euphoria might be upon us, and this could be an ideal time to take some chips off the table. The company’s comparable sales declined 4.9% in Q1, signaling that the pandemic-fueled home goods boom is rapidly cooling off.

Click to Enlarge

Also, management benefited from a one-time $49 million reversal of freight accruals in the quarter, artificially inflating operating margins to 19.5%. Excluding this, margins would’ve been materially lower at 17% to 17.4%. Thus, future margins could struggle.

Regardless, it’s hard to justify chasing it at these levels. The risk-reward seems skewed to the downside, especially as consumers tighten discretionary spending.

Century Aluminum Company (CENX)

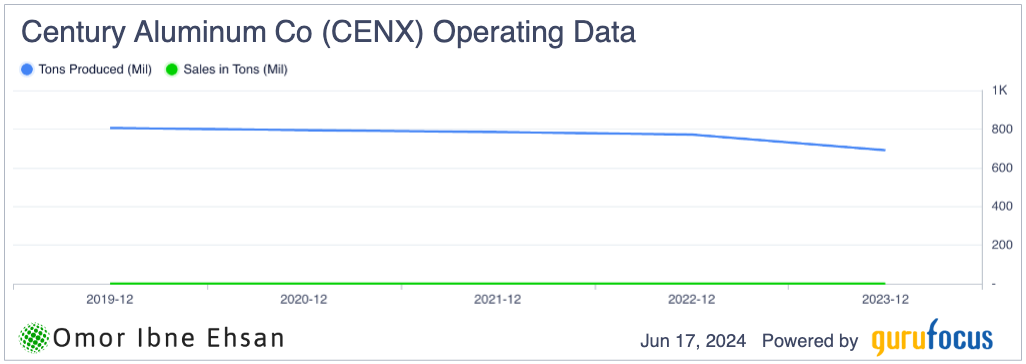

Century Aluminum (NASDAQ:CENX) produces primary aluminum in the U.S. and Iceland. While CENX stock has soared over 65% in the past year, I believe it’s time for investors to take profits and sell. The current earnings multiple of 35 times forward earnings is simply too stretched. Even when zooming out, it trades at 11 times 2025 estimated earnings. Production has also gone down in the long run.

Click to Enlarge

Despite the company’s progress on new initiatives and improving market conditions, I don’t see anything exceptional that justifies the current premium valuation. Adjusted EBITDA of just $25 million in Q1 is good but not great. And while alumina prices have risen, driving some near-term tailwinds, this is a cyclical business that has seen many ups and downs over its history.

So, CENX may be at another cyclical high. The growth and profit potential ahead simply doesn’t hint at anything interesting enough to maintain this overvalued stock price. It could be wise to sell into this strength before the pullback gets worse.

MicroStrategy (MSTR)

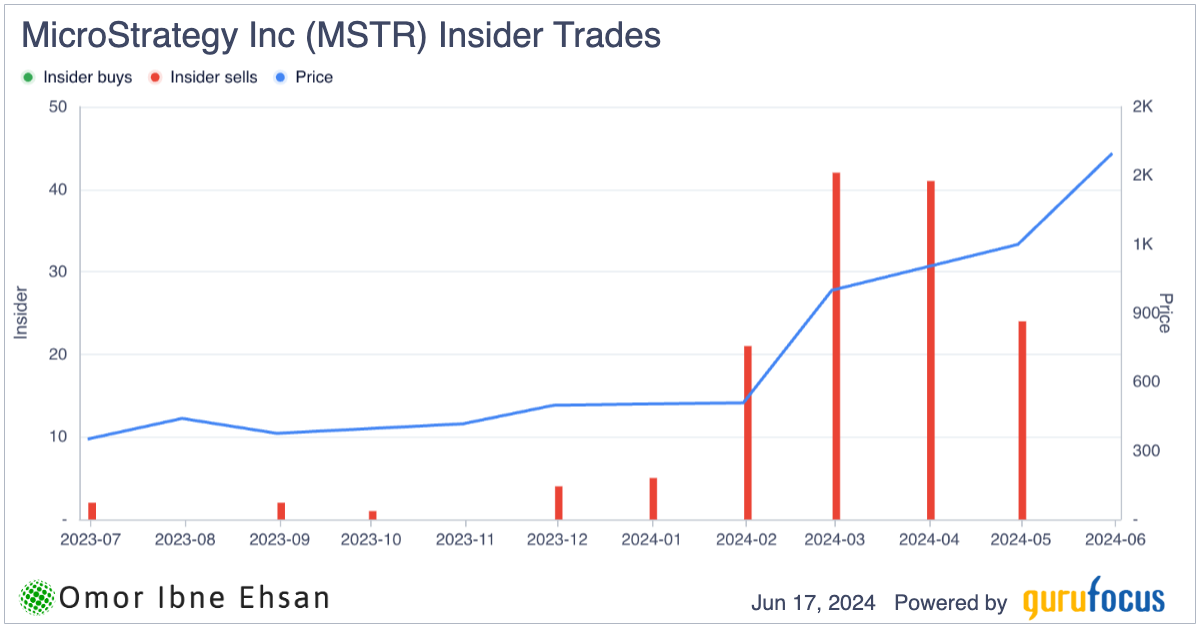

MicroStrategy (NASDAQ:MSTR) provides enterprise analytics and business intelligence software. I’m very bearish on MSTR stock right now, even though I remain bullish on crypto in the long term. That’s because MSTR tends to get extremely overvalued during crypto bull markets. So it would be prudent to take profits here with the stock up a staggering 377% in the past year alone.

While MicroStrategy’s subscription services revenue grew an impressive 22% to $23 million, I believe the downside risks far outweigh any remaining upside potential. The company holds 214,400 Bitcoins at an average purchase price of $35,180 per BTC.

However, this massive Bitcoin position also makes MSTR incredibly vulnerable to any crypto market downturn. If Bitcoin prices pull back, MSTR shares will likely plummet, given how much the stock has run up. Quite frankly, MSTR is only a buy when crypto markets are struggling – not when they’re booming. For now, it’s time to lock in gains and steer clear. Insiders are doing just that.

Click to Enlarge

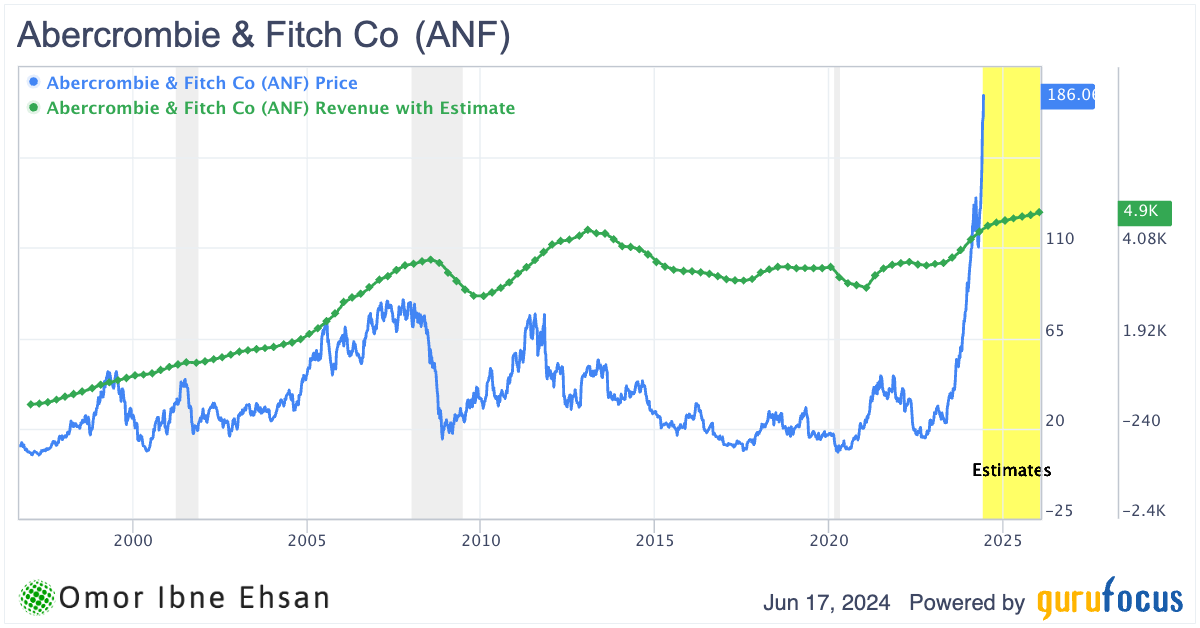

Abercrombie & Fitch (ANF)

Abercrombie & Fitch (NYSE:ANF) operates as a specialty retailer of apparel and accessories. ANF delivered record Q1 sales of $1 billion and operating income of $130 million But the stock’s 413% surge over the past year has left it overvalued and vulnerable to a steep correction.

The apparel market is notoriously cyclical. And, discretionary stocks like ANF tend to be the first to stumble when economic headwinds intensify. The company had strong sales growth across regions and brands. Yet, analysts are forecasting a sharp deceleration to just 4% annual revenue growth going forward. I doubt the market will pay a premium for the stock when that happens.

Click to Enlarge

With such mediocre growth on the horizon, ANF’s valuation of 20 times forward earnings and two times sales is very lofty. Given the challenging macro backdrop for consumer spending, the market is pricing in an unrealistic level of optimism.

Wingstop (WING)

Wingstop (NASDAQ:WING) operates and franchises restaurants specializing in cooked-to-order chicken wings and fries. The stock has been on an absolute tear, soaring 110% over the past year to trade at a staggering 21 times forward sales and 116 times forward earnings.

Truly, Wingstop’s growth has been undeniably impressive. Its Q1 same-store sales surged 21.6%, and 65 net new restaurants opened. However, the current valuation has gotten ahead of itself. The company is now trading more like a high-flying software stock than a restaurant chain.

Yes, management raised their full-year same-store sales guidance to low-double-digits. But how much of this momentum is sustainable? As consumers eventually pull back on discretionary spending amidst economic uncertainty, Wingstop’s premium valuation leaves little margin for error. Analysts see little upside.

Click to Enlarge

It’s hard to justify paying such a lofty multiple for a restaurant stock. Wingstop seems priced to perfection.

Encore Wire (WIRE)

Encore Wire (NASDAQ:WIRE) manufactures a wide range of electrical building wire and cable products. The stock has been a standout performer, soaring 437% over the past five years, but I believe the market’s exuberance has gone too far. While Encore Wire’s underlying business remains solid, there are mounting headwinds that could send the shares lower from here.

For one, EPS has struggled to get back to the $37 range seen back in 2022 and is projected to still be around $20 in 2025. Additionally, sales growth has decelerated to the mid-single digits and remains well below the $3 billion peak reached in 2022.

Encore Wire has also agreed to be acquired for $290 per share, and the stock is currently trading just a hair below that level.

Click to Enlarge

In my view, this puts a firm ceiling on the upside potential and leaves the stock vulnerable to downside risk if the deal encounters any hiccups. I think it’s time for investors to take profits.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.