The retail sector has been an interesting one, full of the haves and the have-nots. Best Buy (NYSE:BBY) doesn’t really fit into either category very well. With that said though, Best Buy stock has performed well.

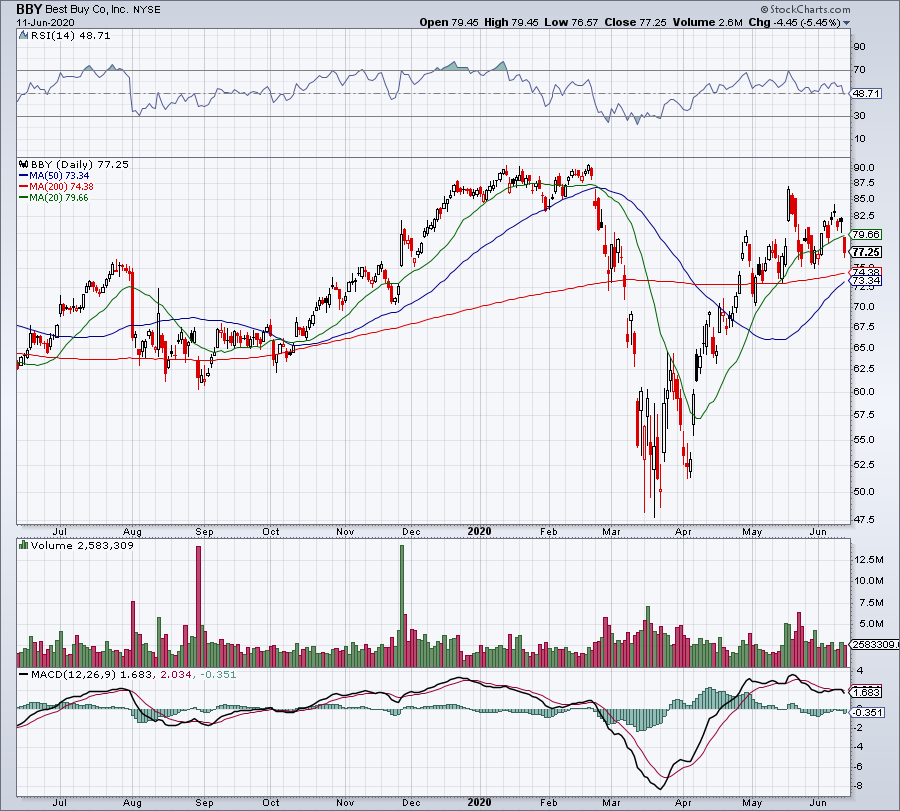

Shares are still up 61% from the March lows, and that includes its 5.5% decline on June 11. That came as the rest of the market was hammered as well.

Best Buy shares have found a way to climb despite this state of limbo. On the one hand, it’s not benefiting from a flood of demand from the novel coronavirus the way many grocers are. By the same token though, it’s also not one that’s being completely shut out either.

What Is Best Buy Doing During Coronavirus?

Retail is a very difficult sector to trust, as it depends on so many different factors. On the one hand, public sentiment and consumer confidence is key. That is, sentiment being positive enough to go out amid Covid-19 and confidence being high enough to justify spending money.

On the other hand, retail also has to balance state and local regulations, as many counties and states imposed various lockdown and stay-at-home orders.

Best Buy isn’t like Costco (NASDAQ:COST), Kroger (NYSE:KR), Target (NYSE:TGT) and a handful of others. It’s also not as vulnerable as companies like Foot Locker (NYSE:FL) or

Macy’s (NYSE:M).

Instead, Best Buy can benefit from several key trends performing well due to the coronavirus outbreak. The three main trends that come to mind include: e-commerce, work from home and gaming.

E-commerce sales are exploding. All you have to do is look at Amazon (NASDAQ:AMZN) or Chewy (NYSE:CHWY) to know that to be the case. If that doesn’t work for you, ask your local mail carrier how the parcel load has been lately. Online sales are surging, juicing a secular trend that’s been play for years.

Work from home is another obvious trend during the coronavirus outbreak. Twitter (NYSE:TWTR) and Square (NYSE:SQ) have already announced indefinite work-from-home policies, while many others in tech and corporate are taking this avenue. That has driven up demand for accessories, monitors and office equipment.

Finally, gaming is on a tear. The industry recorded its best sales for the month of March in 12 years. April set a new record. While Best Buy won’t capture all of the gaming dollars that consumers are doling out, it will catch enough that it will benefit the company’s revenue results.

Valuing Best Buy Stock

Click to Enlarge

While Best Buy’s stock is benefiting from these trends, that’s not to say it’s thriving necessarily. It has plenty of competition and has had to work its way through various lockdown obstacles.

When the company reported earnings a few weeks ago, it beat on earnings and revenue expectations. However, sales of $8.56 billion fell more than 6% year-over-year. Still, given the impact that many are seeing, I’ll take that if I’m an investor.

Domestic online comp-store sales ripped higher by 155%, showing off Best Buy’s e-commerce push, while management had this to say about the results: “In the middle of Q1, we shifted all our stores to a curbside-only operating model and were able to retain approximately 81% of last year’s sales2 during the last six weeks of the quarter, even though not a single customer set foot in our stores.”

That was the company’s first quarter of its fiscal year and look how well it did. Consensus estimates call for sales to slip just 3.3% this year, although that may be overly cautious given the rapid reopening we’re seeing in the U.S. That said, the earnings front calls for a bigger hit, as analysts look for a drop of 16% this year.

Best Buy stock trades at a reasonable 15 times earnings and pays out a dividend yield of 2.7%. Does it pack the biggest growth punch out there or the most yield? No. But it has solid growth and is a retailer that will do well with or without the coronavirus outbreak taking place. I say, stick with Best Buy stock for now.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.