Most of us are aware that the stock market continues to climb higher and higher. New high after new high continues to bless the Dow Jones, S&P 500 Index and Nasdaq Composite. The VIX — also known as the “fear gauge” — is hovering near record lows. That’s got some high-quality dividend stocks looking a tad expensive.

While some valuations are stretching too far, the yields are also sinking below key thresholds. Consider that many investors like a nice round number on yields. They don’t say, “Oh I’m looking for 2.83% and higher.” No, they usually want stocks with 3% yields or higher. Or 2.5%, 3.5% and any reasonable number in between.

Thanks to the ever-climbing stock market, many yields have been on the decline. That doesn’t make these stocks a sell. In some cases, they’re not even a hold — some very well may still be a buy.

However, should a market correction occur — anywhere from a standard 5% to a more gut-wrenching 10%-15% — these stocks will be much more attractive. Market-wide corrections are welcome (minus that panic feeling!) because the businesses aren’t changing. Just the stock price.

So what we have here are seven high-quality dividend stocks that may be a bit over their skis, but still worthy of investors’ dollars. Rather than building out a full positions, however, these dividend stocks may warrant a buy-half-now, buy-half-later type of strategy. Should a pullback materialize, these stocks will be even more attractive.

Dividend Stocks to Buy on a Pullback: Johnson & Johnson (JNJ)

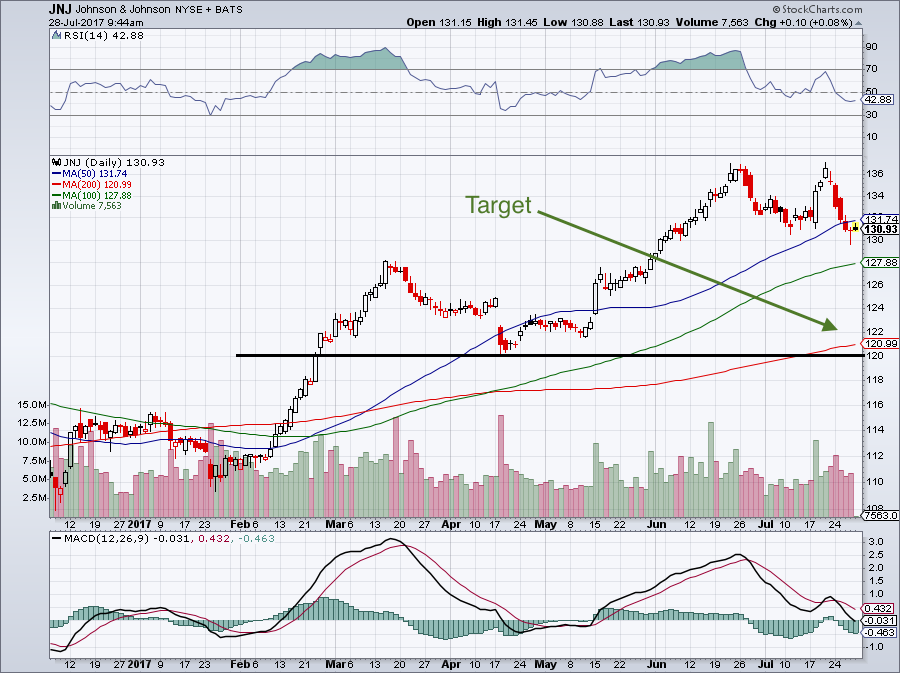

Roughly 18 months ago, Johnson & Johnson (NYSE:JNJ) was yielding just north of 3%. But after JNJ stock went on a rip-roaring 27% rally, shares now yield just 2.6%. Like we said in the intro, it’s not that JNJ is an unattractive company. It’s just that its stock has been quite strong — up 13.5% in 2017 alone.

The 5.5% and 5.6% sales growth expected in 2017 and 2018, respectively, is attractive. So is the steady 6% to 7% earnings per share growth expected over the next five years. But is it worth 17x forward earnings and a price-to-earnings ratio of 22?

History says no, and perhaps investors do, too. Shares have twice hit the $136 level over the past month and have been harshly sold lower. That makes today’s prices at $130 an okay level to start a position, if investors aren’t already long.

But what would be more attractive is a $10 per share decline, or roughly 7.5%. This decline would push JNJ’s dividend yield up to a more attractive 2.8%. That would get a lot of blue-chip and income-hungry investors to perk up. Second, it would bring its valuation down to a more reasonable level.

Click to Enlarge

Over the past five years, JNJ stock has had its price-earnings ratio hit 23 four times. Each time it has quickly fallen back below 20, including a few weeks ago. Getting down to a P/E of 20 would require JNJ stock to fall to about $120 per share. Looking at the charts, this level should have good support, too.

It’s okay to pay a premium price for premium stocks. With its strong brands, fat profit margins (22.5%) and reasonable dividend, JNJ is one of those premium names.

Dividend Stocks to Buy on a Pullback: Pepsi (PEP)

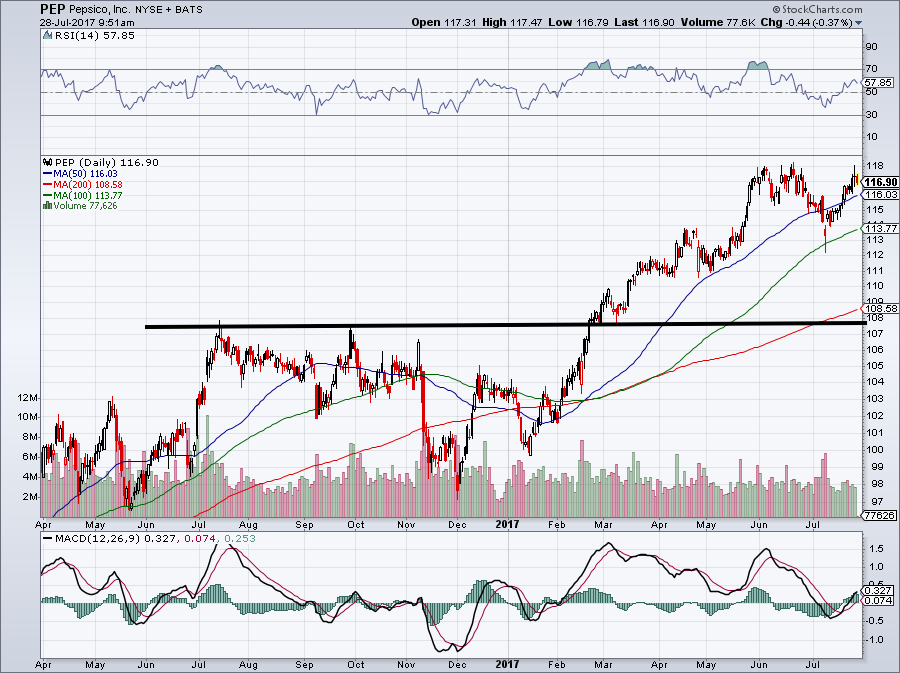

PepsiCo, Inc. (NYSE:PEP) is within a stone’s throw of its 52-week high at $118.24. It’s no surprise, given that two weeks ago PEP gave investors a fifth-straight earnings and revenue beat.

However, the stock’s performance — up 12.2% in 2017 — has driven its dividend yield down to 2.75%. Rarely does PEP stock carry a 3% dividend yield. So for a high-quality company like Pepsi, a high 2% yield is really all we can ask for. (I promise we’ll get to some higher yielding stocks in a minute!)

Of course, investors who want more yield can go to The Coca-Cola Company (NYSE:KO). While it may dish out a 3.2% yield, investors have to pay a higher valuation for slower growth. Personally, I’d rather take the slightly lower payout and invest in the stronger company. CEO Indra Nooyi has done a fabulous job with PepsiCo. Beyond just Pepsi, the company owns brands like Tropicana, Gatorade, Aquafina, Lipton and dozens of others. It’s got snacks like Sabra hummus, Stacy’s Pita Chips, Lay’s, Ruffles and Tostitos. It’s a killer lineup that’s sure to be around for decades to come.

Because of the strong business, investors can certainly stay long. However, those looking to buy may not want a full position just yet. PEP stock currently carries a 21.1 forward P/E ratio and a trailing P/E ratio of 24.8. Even for a strong brand like Pepsi, it’s hard to justify that type of valuation for a mid- to high-single digit earnings grower.

Click to Enlarge

It’s hard to say where to buy Pepsi on a historical basis, though. Over the last five years, shares have steadily commanded a higher valuation. However, a 7% to 8% correction would bring its valuation at least back to historical norms. It would also put the stock close to its 200-day moving average and just above prior resistance.

Dividend Stocks to Buy on a Pullback: McDonald’s (MCD)

Consumers can debate the Pepsi versus Coke taste battle until they’re blue in the face. But it’s hard to argue about sipping on one while enjoying a burger from McDonald’s Corporation (NYSE:MCD). I’m not sure what kind of magic CEO Steve Easterbrook has, but he’s got some mojo when it comes to running a company.

McDonald’s is on fire. Although revenues declined 3.4% year-over-year last quarter, MCD turned in its fifth-straight top- and bottom-line earnings beat. Investors are cheering over the company’s blazing comp-store sales results of 6.6% this quarter, smashing estimates of 4%. Heck, that’s even better than Starbucks Corporation (NYSE:SBUX). And get this, management is working on ways to accelerate that growth.

Of course, MCD stock has been on fire as a result of all this. This once-4% dividend yielder now pays out just 2.4%. That’s down because it’s been rallying hard, climbing 22% and 63% over the past 12 and 24 months, respectively. While I admit a faster-growing company deserves a higher multiple, McDonald’s may be ahead of its skis. Analysts expect earnings to grow an impressive 14% this year, but just 7% in 2018. Additionally, sales will take a hit in both years. While lower sales and higher profits translates to better margins, its forward and trailing P/E ratio of 22.5 and 27.7 are alarming.

Long-time investors likely won’t part ways and I don’t blame them. But I wouldn’t be adding up here. I’m not sure what would cause the selloff, but a decline to the $133 to $136 area would push its yield close to 3% and make MCD stock much more attractive. Especially if it continues to turn in strong growth like it did last quarter.

Dividend Stocks to Buy on a Pullback: Realty Income (O)

Apologies for starting with three sub-3% dividend stocks. These next four all have yields north of 3%, starting with Realty Income Corp (NYSE:O).

O stock has been consolidating for about 10 months now, trading between $52 and $62, on concerns with interest rates and retail. First, when interest rates rise, it makes risk-free money (Treasuries) more attractive versus bond-equivalent stocks. Think stocks like General Electric Company (NYSE:GE) and Pepsi, and more specifically sectors like utilities, telecoms and real estate investment trusts. As a landlord, however, the demise of retail falls directly on O’s lap.

But Realty Income isn’t some flaky company with questionable specs. For starters, rising interest rates means that the Federal Reserve believes the economy is strengthening. Would you rather own a retail REIT in a falling rate environment as the economy tanks or a strengthening economy with rising rates? I’ll take the latter scenario as well.

Second, O isn’t 100% immune to the retail slowdown. But the “Monthly Dividend Company” has a very diverse portfolio of highly successful, dependable tenants. That should reassure investors that they’re investing in a company that will be around for awhile. This isn’t a mall-based REIT with tenants going bankrupt every few months.

It’s paid out a dividend for 564 straight months (47 years!), raising that payout for 79 consecutive quarters (19.75 years!). Shares have returned a compound annual growth rate of 16.4% since going public almost 25 years ago.

So you want a 4.4% yield that you can count on? Go with O. Investors can easily justify buying the stock around $56 to $57 with plans to add even more on a dip back into the $52 to $53 range.

Dividend Stocks to Buy on a Pullback: Procter & Gamble (PG)

Up 4.5% over the past two weeks, Procter & Gamble Co (NYSE:PG) finds itself higher by almost 8% this year. This may surprise some, given that P&G continues to struggle from a business perspective. But there are reasons aside from its 3.05% yield to give PG a shot.

Earnings estimates call for 5% growth in 2017 and nearly 7% in 2018. That’s not bad, and honestly, its P/E ratio of 16.5 isn’t too shabby either. If PG weren’t a blue-chip company, 16.5 multiple may be hard to pay for 6% annual earnings growth. But this is a premium name. Besides, this is the stock’s lowest valuation since 2011, so obviously investors are discounting it a bit. Additionally, Nelson Peltz is lobbying for change. Peltz has a pretty solid track record as an activist, so his focus on P&G should be a positive.

Peltz doesn’t want a new CEO, nor a breakup, use of excessive leverage or removal of current directors. He in fact, really just wants to be added to the board. He’s referenced P&G as a “suffocating bureaucracy.” Trian, which Peltz runs, later had this to say:

“Over the past 10 years, P&G’s total return to shareholders is less than half that of its peers and it has been in the bottom quartile over most recent time frames…Trian believes P&G needs to address the root causes of this consistent underperformance, including deteriorating market share across most of its categories and excessive cost and bureaucracy.”

PG stock may go on sale later this year, which makes it a perfect buy-half-now, buy-half-later position. PG’s trading at its lowest valuation in six years and pays a solid dividend. Finally, with Peltz making noise, some positive changes should come P&G’s way.

Dividend Stocks to Buy on a Pullback: Cisco (CSCO)

Cisco Systems, Inc. (NYSE:CSCO) may be one of the most attractive names on the list. Shares are still up 4.4% on the year, but this includes its recent 7.5% decline from about $34. Now trading nearly $31.50, CSCO stock has a more attractive dividend yield (3.7%) and a better valuation. Trading at just 12.5x forward estimates and about 16x trailing earnings, CSCO is pretty darn cheap.

Everything isn’t perfect, though. While Cisco has an impressive streak of beating on earnings and revenue, it hasn’t grown sales by more than 5% since February 2015. It won’t be this year and likely not next year either. Analysts expect revenue to fall 2.7% this year and grow just 0.5% in 2018. Earnings growth is subpar as well, growing at less than 1% this year and 3% in 2018.

For all that sluggishness, some may wonder why CSCO is a name to consider. Its low valuation and fat dividend fit in nicely alongside its profitable business. But what CSCO needs to do is open up the wallet. It’s got an insane $68 billion in cash and short-term investments versus a market cap of about $160 billion.

Click to Enlarge With that kind of cash it’s time to start buying some companies and fueling that top line growth. If it does, investors will surely pay a higher premium for Cisco. If it doesn’t, shares could be header lower. Its 52-week low of $29.12 is only a few dollars away. I don’t usually like buying new lows in stocks.

But for this type of valuation and for a company with this much cash, one could justify buying now and adding at more attractive levels. But please Cisco, buy something!

Dividend Stocks to Buy on a Pullback: Blackstone (BX)

Blackstone Group LP (NYSE:BX) is one of my favorite companies. After erupting after the election, it seemed like BX was destined to chop between $28 and $30. If I hadn’t been so greedy with my entry, I too would be enjoying the stock’s breakout to $34.

The downfall to Blackstone is its earnings. Not that it swings between net loss and net gain, but that its overall income looks like a set of waves. It’s a series of high peaks and deep troughs. Market timers can do well in BX if they hit it at the right time. In the same way we pay a premium for predictable earnings, we pay a discount for volatile earnings.

Hence, BX trades at just 10.8x forward earnings estimates. That’s despite forecasts calling for 43% growth this year and another 9.4% in 2018.

Despite the earnings volatility though, BX is an incredibly high-quality company. CEO Stephen Schwarzman established BX in 1985 and has been at the head ever since. The big news for the company came in May, when it was announced that the Public Investment Fund (PIF) of Saudi Arabia would be putting $20 billion toward U.S infrastructure projects.

The $20 billion is an “anchor” in the BX fund and management expects another $20 billion to come from other investors. In the end, BX says it could invest about $100 billion through the project. Blackstone makes its money mainly through management fees. When these fees start falling to the bottom line, BX investors will be very happy.

With consolidation occurring near current levels and a dividend yield of 6.25%, investors can buy BX stock near $33. However, investors should add to that position should shares fall to between $28 and $31 for more long-term gains.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell held a long position in SBUX and O.