I’ll tell you what is most worrisome about the stock market at all-time highs with valuations now exceeding the dot-com bubble. It’s the fact that mature, blue-chip stocks are currently way overvalued.

Before we get further into the topic of blue-chip stocks, let’s first take a look at the overall state of the market:

- The Shiller CAPE price-to-earnings (P/E) ratio is at more than twice its historical averages.

- Margin debt at brokerage firms is at all-time highs.

- $5.3 trillion in stimulus was given out over the past 15 months, which won’t be repeated. According to surveys, 40% of this went into the stocks.

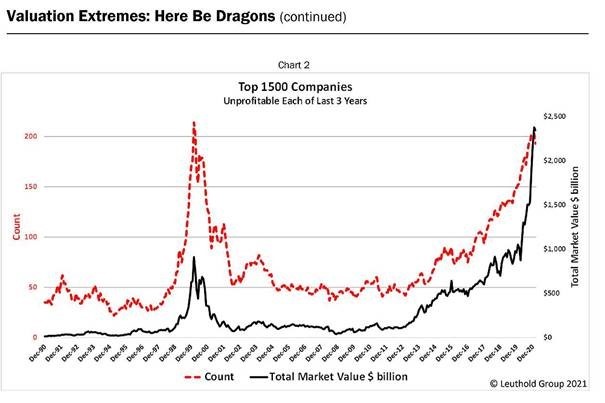

- The number of unprofitable companies is at the highest level since 1999.

- The devastating effect of inflation on consumers and companies is potentially forthcoming.

- The price-to-sales (P/S) ratio for the S&P 500 is at an all-time high.

- The market-capitalization-to-GDP ratio is at an all-time high.

We all know there are stocks in this bull market that represent ridiculously speculative concepts that are doomed to failure. Think Lemonade (NYSE:LMND) or Nikola (NASDAQ:NKLA). And then there are real businesses whose stock prices are grossly over-inflated. Thus, there should be high expectations for an ugly divorce between business success and investment success for a decade. Think Netflix (NASDAQ:NFLX) and Tesla (NASDAQ:TSLA).

It’s not so much the growth-oriented tech stocks that are bothersome, but what keeps me up at night is the valuations of blue-chip, established, mature companies. Growth-stock bull markets come and go with crazed valuations, but why are we paying so much for some of the most fabled and established businesses in the world?

That’s what bothers me.

Let’s look at some of these overvalued blue-chip companies:

- McDonalds (NYSE:MCD)

- Clorox (NYSE:CLX)

- Visa (NYSE:V)

- Target (NYSE:TGT)

- Equifax (NYSE:EFX)

- Automatic Data Processing (NASDAQ:ADP)

- Cintas (NASDAQ:CTAS)

Overvalued Blue-Chip Stocks: McDonalds (MCD)

The history and growth of McDonalds over the 20th century is one of the great business stories in American history. From one store in 1948 to 39,000 restaurants today in over 100 countries, McDonalds was the ultimate growth stock. But as mentioned before, all growth stocks mature. And with 13,700 units in the U.S., unit growth has come to a grinding halt and is now shrinking.

U.S. comp sales are expected to be up 9% in 2021, compared to pre-Covid-19 growth of 5%. After this rebound year, comp sales should return to the low double-digit range.

MCD stock trades at 28x 2021 consensus earnings per share (EPS) estimates compared to long-time historical P/E ratios that averaged in the mid-teens range. Success at fundamental investing is derived by both multiple expansion and earnings growth. There will be little if any multiple expansion for MCD stock. We will almost certainly see a contraction when the market turns sour.

MCD’s upside is limited to likely mid-single-digit growth, so it may be better to wait for an entry point that offers both multiple expansion and earnings growth.

Clorox (CLX )

Since 1913, the Clorox bottle has been a household staple in practically every home in America. However, almost all consumer products manufacturers are mature businesses. Clorox averaged 2% revenue growth from 2014 to 2019. Furthermore, long-term expectations post-Covid-19 are to ramp that up to 3% to 4%.

The double-digit growth in 2020 was, of course, due to pandemic-led purchases of cleaning supplies. We didn’t know at the time that surface transmission of Covid-19 was extremely rare. As a result, Clorox was able to get a one-time boost from the unclear science at the time as people around the world excessively cleaned their homes and businesses.

CLX stock has retreated about 23% from its highs last summer, but it still trades at 23x 2022 normalized earnings. Clorox’s 14x EV/EBITDA ratio for 2021 should be reserved for growth tech stocks demonstrating sustainable long-term double-digit growth.

The company’s 2.43% dividend yield won’t help when multiples retreat to historical levels. Now the market has to adjust to the reality of Clorox being just another mature consumer products company.

Overvalued Blue-Chip Stocks: Visa (V)

Since going public in 2008, Visa has achieved solid large-cap growth status with a total return of approximately 1,372%. The famed global payments company with one of the most recognized brand names on earth operates an asset-light, low capex business model.

Double-digit growth has been the norm for Visa for much of its life as a public company and has traded at P/E multiples in the low 20s. However, today V stock trades at an astounding 43x 2021 estimated EPS.

At this level, share buybacks will destroy shareholder capital, as multiple expansions from these levels are highly unlikely. Unless we get 10 straight years of very strong global economic growth, valuation ratios for Visa are only going one direction — down.

Target (TGT)

I covered Target in detail in my article last week. The company had fantastic results in 2020 as a result of essential business as well as a thriving online segment driven by lockdowns. Comp sales increased an astonishing 19.3% last year, driven by digital and omni-channel offerings. This compares to the previous two years of annual comp growth, which were 3.4% and 5%.

However the stock trades as 24x 2021 estimate EPS, as investors apparently think that type of 2020 growth can continue. But how does one justify these valuations for a large retail industry player that will likely grow at GDP rates plus a few points if they execute very well? Target’s online business can grow at strong double-digit rates for quite some time, but at some point their physical stores are at risk of being stranded assets.

Even more disturbing is the company’s statement that at the end of FY 2020, there was $4.5 billion available on their share repurchase program. Buying back shares at extraordinarily high valuations with the stock price near all-time highs is a surefire way to destroy shareholder value and waste the company’s own capital.

It’s safe to say nothing has really changed, and we can expect the market to adjust TGT stock to its proper standing in the mature retail world.

Overvalued Blue-Chip Stocks: Equifax (EFX)

Equifax may not be a common name to stock traders, but it’s certainly a household name to consumers who have had any form of credit in their lives. EFX is one of the big three credit-reporting bureaus, the others being Trans-Union (NYSE:TRU) and Experian (OTCMKTS:EXPGF).

EFX has benefited from the explosive real estate and refinancing market as artificially suppressed interest rates by the government has led to a real estate boom that may eclipse 2006 and 2007. Revenues grew 18% in 2020 and 27% in Q1 2021. Keep in mind, this is a company that grows at GDP levels and is heavily tied to economic activity. Revenues grew 2.8% in 2019 and 1.5% in 2018.

Equifax is a well-managed and innovative company that suffered one major scandal in 2017 as hackers breached into 143 million consumers’ private data. The company eventually recovered and restored its damaged reputation.

As it stands today, Equifax is still a great company that should experience long-term growth at GDP rates going forward, excluding the forthcoming real estate bust. Furthermore, it is now valued at 33x 2021 EPS and 27x 2022 EPS. Come on!

Equifax is one of my favorites companies I’ve had the pleasure of knowing in my 25-year career. But come on!

Automatic Data Processing (ADP)

A long-time growth and dividend achiever, ADP has been successfully rewarding investors since the 1980s. As the largest payroll processor and provider of other human capital management solutions, ADP is a cash-flow machine with a sticky, low-turnover business model.

ADP is generally a cyclical company as its growth is typically tied to payroll growth and unemployment levels. The company took a big hit in the initial 2020 Covid-19 crash. ADP stock plummeted over 40% as unemployment skyrocketed in early 2020. It has since recovered, but why is it trading at 31x FY 2021 estimated EPS and 28x FY 2022 estimated EPS? That is significantly above its historical P/E trading ranges.

For a low to mid single-digit grower for both revenues and EPS, ADP valuation rations are extreme and not sustainable.

Overvalued Blue-Chip Stocks: Cintas (CTAS)

While investors often get overly obsessed with technology, innovation and disruption, that’s the not the only way to make money in the stock market.

Providing and cleaning uniforms as well as cleaning supplies to a very large chunk of businesses in America has proven to be a successful formula for Cintas. Had you bought CTAS at around $5 per share in 1990 and sold it today at $350, your total annual gain would have been — hold on, let me do the numbers — a ginormous return on your investment. But let’s say someone said you should invest in this hot computer technology company, or a cleaning and uniform company — which would you have chosen?

Cintas is also a cyclical company tied to economic activity, mostly in North America. CTAS stock suffered a big 2020 drop as restaurants and retail businesses shut down during the pandemic lockdowns.

But today, CTAS trades at 35x 2021 EPS estimates and 34x 2022 EPS estimates. It’s EV/EBITDA ratio is about 24x. The type of growth metrics required for valuations like that simply don’t exist at Cintas.

As with Equifax, Cintas is one of my favorite companies of all time. But come on! Let’s be real.

On the date of publication Tom Kerr did not have (either directly or indirectly) any positions in the securities mentioned in this article.

Tom Kerr, CFA, is an experienced investment manager and business writer who has worked in the investment and securities business since 1994.