Dividend stocks are popular for a reason. These stocks are supported by companies with solid underlying businesses generating strong cash flow. Top-rated mature companies have histories that span decades, and they’re unlikely to be knocked off course if there is a recession. Plus, reinvesting these dividends could compound your returns over the decades, resulting in massive overall gains.

As such, I think allocating a good chunk of your portfolio towards such dividend stocks is a good idea. These stocks should provide considerable ballast (and cash) when times are tough, and they’ll continue growing well during the good times. Here are seven dividend stocks to buy and hold until 2030 and beyond.

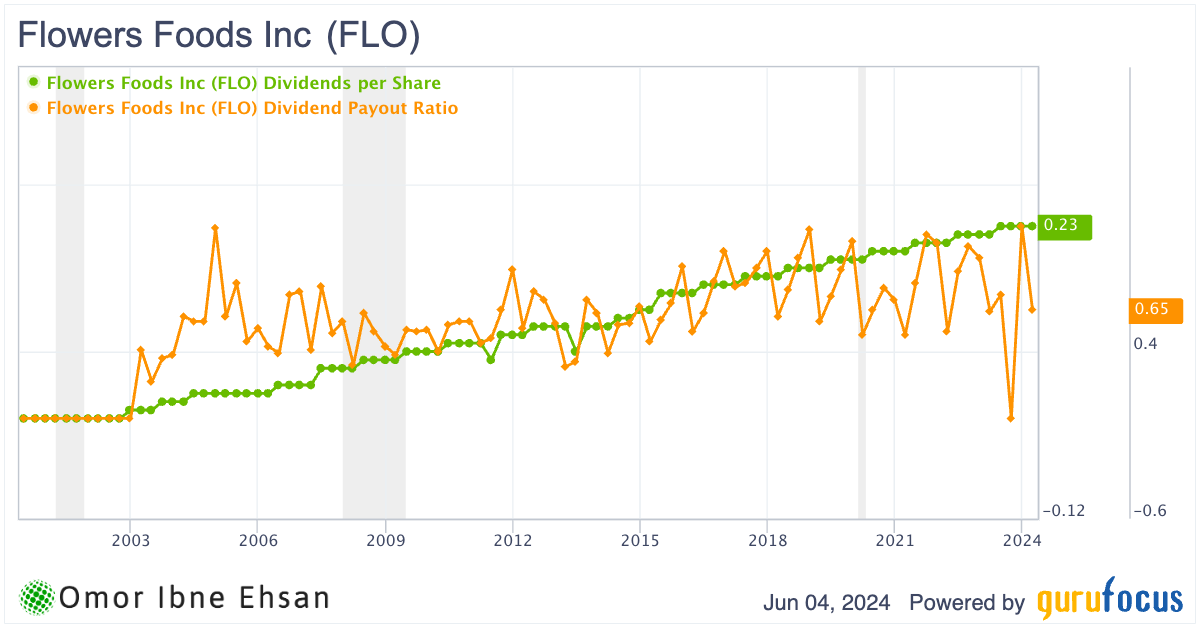

Flowers Foods (FLO)

Flowers Foods (NYSE:FLO) produces and markets packaged bakery foods in the United States. Despite the challenging consumer environment, the company’s solid first-quarter results reflect the increasing effectiveness of its portfolio strategy driven by investments in marketing.

I believe Flowers Foods is one of the most stable and consistent stocks over the past two decades. While FLO stock has dipped slightly recently (like most retail stocks), the company grew branded retail volumes for the first time since 2020, with Dave’s Killer Bread leading the way with its second consecutive quarter of 10% unit growth.

Management is maintaining its full-year outlook, which incorporates continued volume improvement. Although economic uncertainty could impact consumer behavior, Flowers Foods is executing well on its portfolio strategy. The stock’s attractive 4.15% dividend yield and 22-year streak of consecutive hikes make it a compelling option for income-focused investors. I remain confident in Flowers Foods’ growth potential and believe it is a solid dividend stock to buy and hold until 2030.

Click to Enlarge

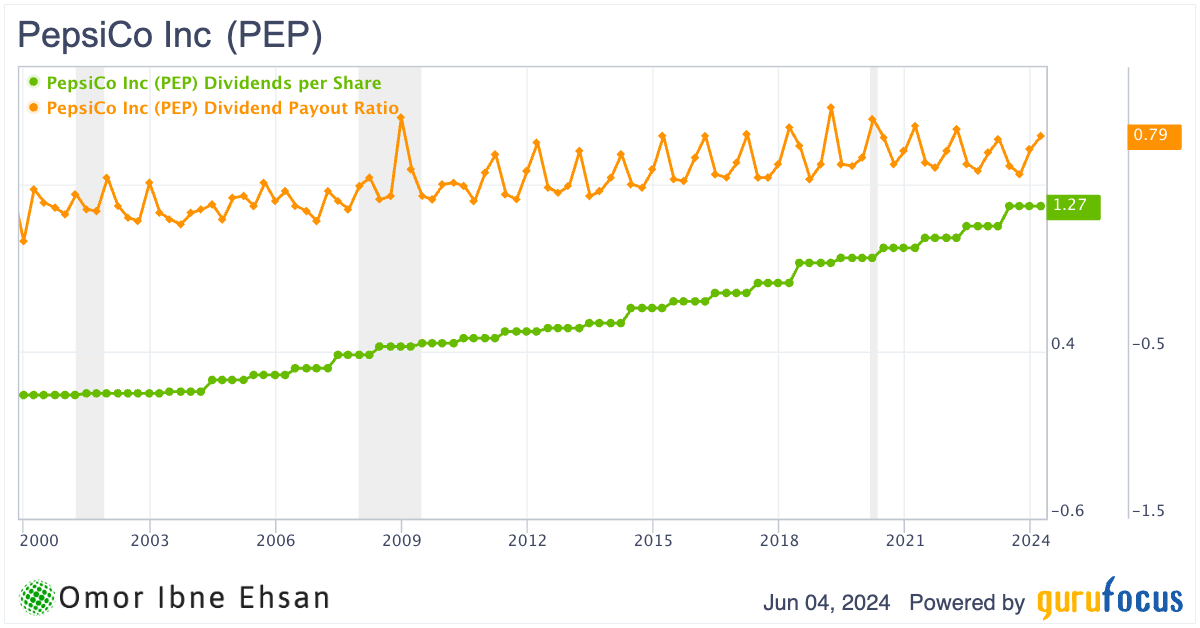

PepsiCo (PEP)

PepsiCo (NASDAQ:PEP) is a global food and beverage powerhouse. This earnings season, I’m even more confident that PEP stock belongs in any long-term dividend growth portfolio. That’s partly due to the fact Pepsi outperformed both earnings and revenue estimates in Q1.

The company’s international business is firing on all cylinders, already at $36 billion in revenue, and growing at an impressive high single-digit rate with strong margins. PepsiCo is smartly investing in manufacturing capacity expansions in key growth markets like China, India, Vietnam and Poland to further capitalize on this momentum.

While Frito-Lay North America margins were a bit soft this quarter, I’m not concerned. The segment still delivered a 2% revenue growth, which is solid, as volume declined by 2%.

With a current 3.17% dividend yield and an incredible 53-year streak of consecutive payout increases, PepsiCo is a quintessential dividend king worth owning for the long-term. I recommend buying this dip and holding PEP stock through thick and thin.

Click to Enlarge

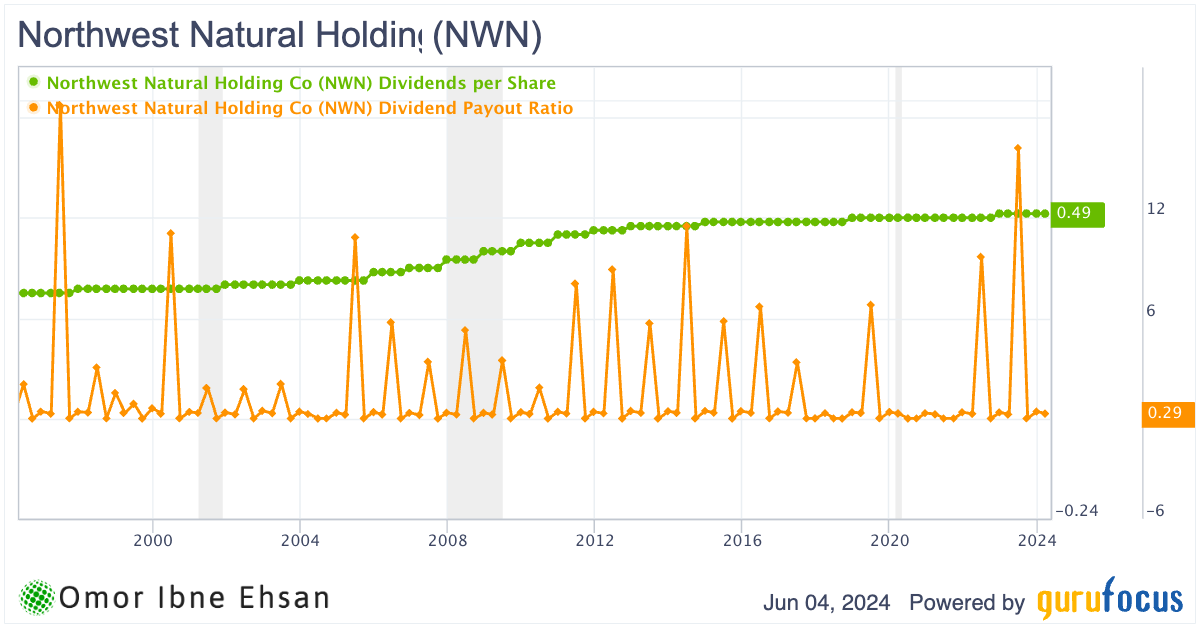

Northwest Natural (NWN)

Northwest Natural Holding (NYSE:NWN) distributes natural gas to customers in the Pacific Northwest. The stock has taken a beating over the past few years, but I believe this beaten-down dividend payer is worth a closer look for income investors with a long-term investing horizon.

In Q1, NWN reported earnings per share of $1.69, missing estimates by 10 cents, on revenue of $433.5 million, a 6.26% year-over-year decline. Despite the earnings miss and shrinking top line, the company maintained their full-year guidance. Additionally, NWN’s customer base grew 1.7% over the last 12 months, and the company delivered record volumes during a severe winter storm in January, highlighting the essential nature of natural gas.

While the Pacific Northwest faces some demographic headwinds, I believe NWN is well-positioned to weather the storm and reward patient investors. LNG prices have also rebounded significantly from recent lows.

Also, I don’t think the Pacific Northwest will see its population shrink too much in the coming years. And hotter summers could convince a lot of people to stay or move north. The dividend yield here comes in at 5.2%.

Click to Enlarge

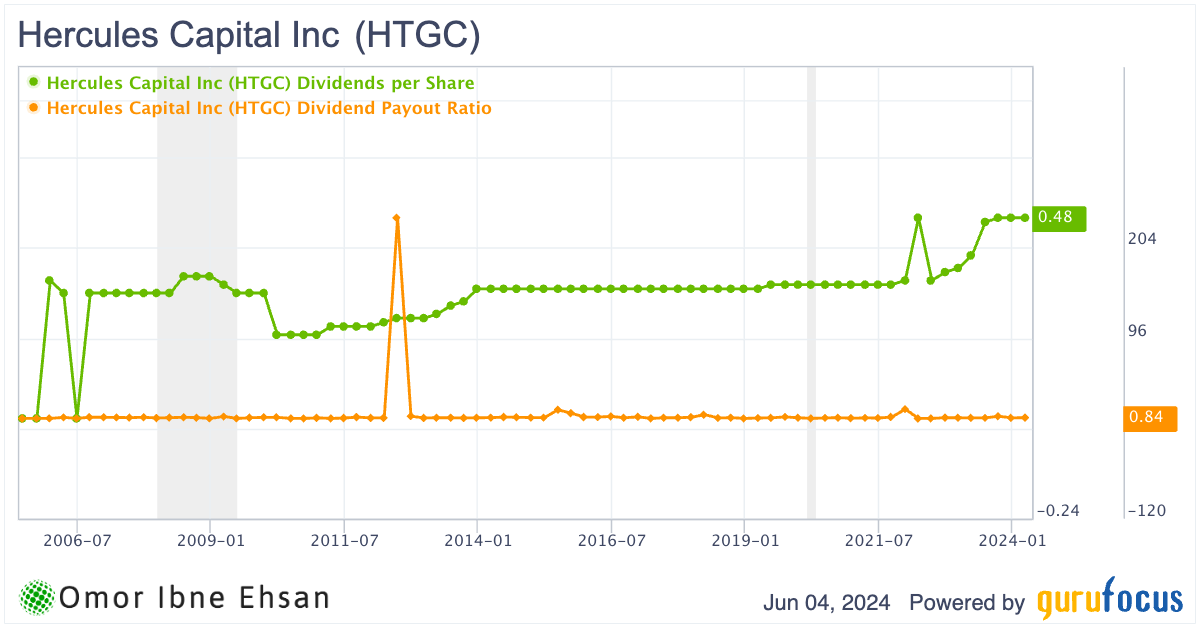

Hercules Capital (HTGC)

Hercules Capital (NYSE:HTGC) is a business development company that provides debt and equity financing to venture capital and private equity-backed companies. I believe this company is well-positioned to deliver strong returns and income for long-term investors. In Q1 2024, Hercules originated a record $956 million in gross debt and equity commitments and funded an impressive $605.2 million. The company generated $121.6 million in total investment income, up nearly 16% year-over-year, and $79.2 million in net investment income, up almost 21%. This allowed Hercules to comfortably cover its 40 cents per share base distribution by 125% despite conservative leverage.

While some may view business development companies as risky, especially in a potential recession, I think Hercules deserves more credit. The stock has already climbed 34% over the past year, and investors can still lock in a juicy 8.06% dividend yield. Even if a recession comes, the stock should recover fast, as it has done so many times in the past.

Click to Enlarge

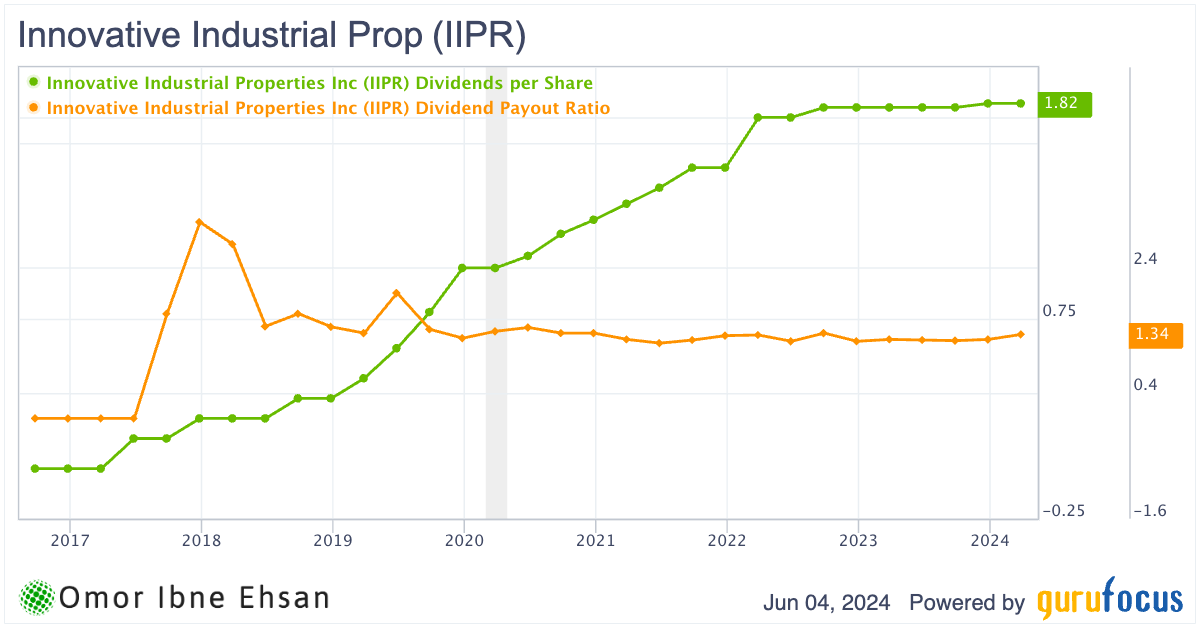

Innovative Industrial Properties (IIPR)

Innovative Industrial Properties (NYSE:IIPR) is a cannabis-focused real estate investment trust (REIT). In my view, IIPR is a compelling dividend stock to buy and hold until 2030 for investors willing to take some risk.

The company reported Q1 2024 revenue of $75.45 million, down a modest 0.81% year-over-year, and adjusted funds from operations (AFFO) per share of $2.21. While growth has moderated, IIPR’s portfolio remains highly stable, with most tenants paying rent on time.

Management also executed new leases at four properties totaling $69 million and completed construction on three fully leased properties spanning 732,000 square feet in the first four months of 2024 alone. This momentum should drive future cash flow growth to support IIPR’s attractive 6.7% dividend yield.

Click to Enlarge

I believe IIPR’s long-term bull case is underpinned by the high likelihood of U.S. cannabis legalization by 2030, which could significantly expand the company’s growth runway. Even without federal legalization, sales could reach $71 billion by then.

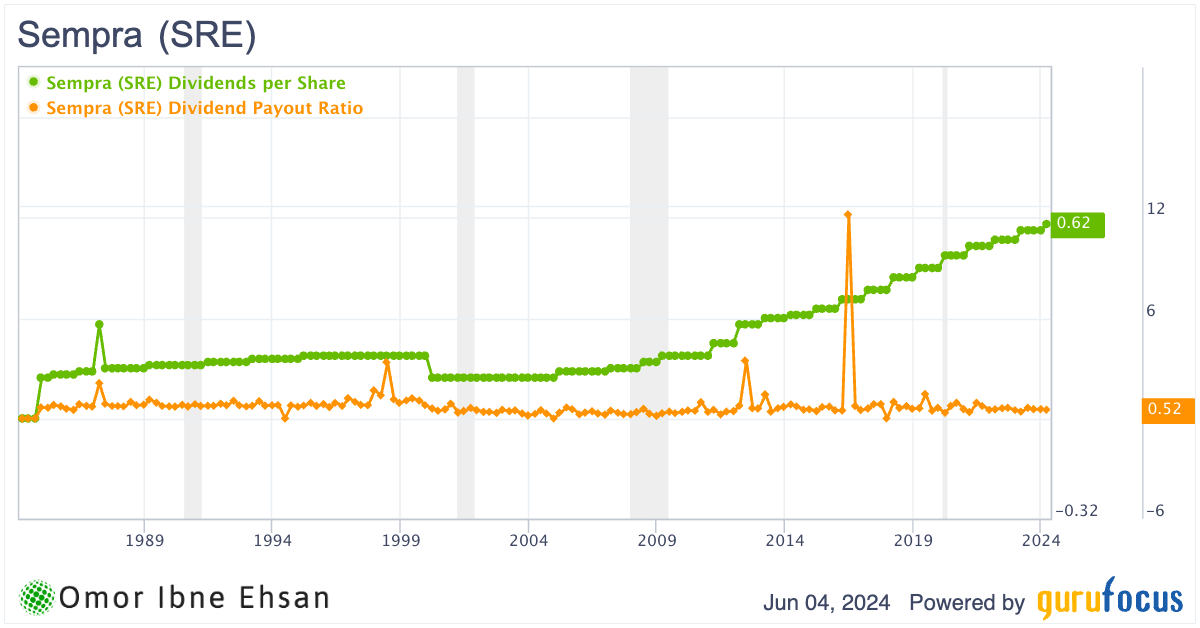

Sempra (SRE)

Sempra Energy (NYSE:SRE) is an energy infrastructure company serving nearly 40 million customers. While the stock has only risen 14% over the past five years, I believe Sempra remains a sturdy long-term investment.

In Q1, Sempra missed revenue estimates considerably, with sales plunging 44.5% year-over-year to $3.64 billion. However, this was primarily due to a pass-through of lower natural gas costs, which fell from $2.7 billion to $554 million. These costs have little profit impact as the savings flow directly to customers.

Looking forward, Sempra can benefit from the current energy infrastructure super-cycle. With strong demand drivers like electrification, AI, and data centers, Sempra is poised to capitalize on grid investments in California and Texas. Meanwhile, its LNG export projects should thrive as Europe shifts away from Russia.

With 21 consecutive years of dividend hikes and a 3.23% yield, Sempra is exactly the type of resilient dividend grower I want to buy and hold until 2030, if not longer. The recent revenue miss has no impact on my confidence.

Click to Enlarge

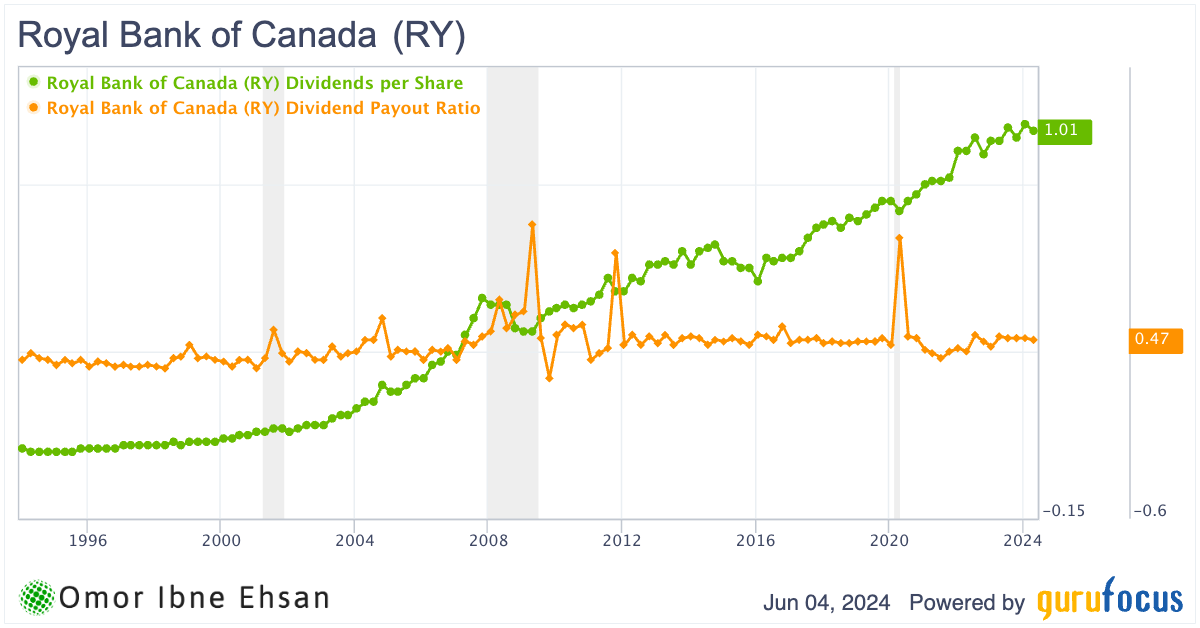

Royal Bank of Canada (RY)

Royal Bank of Canada (NYSE:RY) is Canada’s largest bank by market capitalization. I believe RBC’s strong Q2 results underscore why this is a solid holding for any dividend portfolio. The bank reported net income of $4 billion, with its return on equity (ROE) increasing to an impressive 14.5%. Revenue grew robustly across diversified business lines, from capital markets to Canadian banking.

RBC’s increasing scale advantages and cost discipline drove strong adjusted operating leverage of 4.5%. The bank’s balance sheet remains rock-solid, with a CET1 ratio of 12.8%, even after closing the HSBC Canada acquisition. As Canada’s most influential bank, RBC is not only “too big to fail,” but also exceptionally well-positioned to grow alongside the country’s booming population.

With the stock yielding a healthy 3.84% and the dividend being hiked another 3% this quarter, I’m confident RY stock will continue to be a cash cow for shareholders.

Click to Enlarge

For sleep-well-at-night dividend income and exposure to Canada’s resilient economy, it’s tough to beat RBC.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.