There are a handful of stocks that are benefiting from the new world created by the novel coronavirus. Among the most notable is Zoom Video (NASDAQ:ZM). With Zoom stock up 145% in 2020, its leadership is clear.

As bad as it sounds, there are a handful of stocks that are benefiting from the outbreak of Covid-19. They are the companies that center on stay-at-home themes, generating additional revenue by consumers who continue to spend without leaving their home.

Video conferencing is an obvious winner, but so too are Netflix (NASDAQ:NFLX), Amazon (NASDAQ:AMZN) and others.

Now the question becomes, is Zoom stock one to sell once the coronavirus passes? As we get back to a state of normalcy, that’s a fair question. After all, lockdowns and shelter-in-place orders are what drove ZM shares higher in the first place.

But I think the answer is simple: No, Zoom is not a sell once Covid-19 fades.

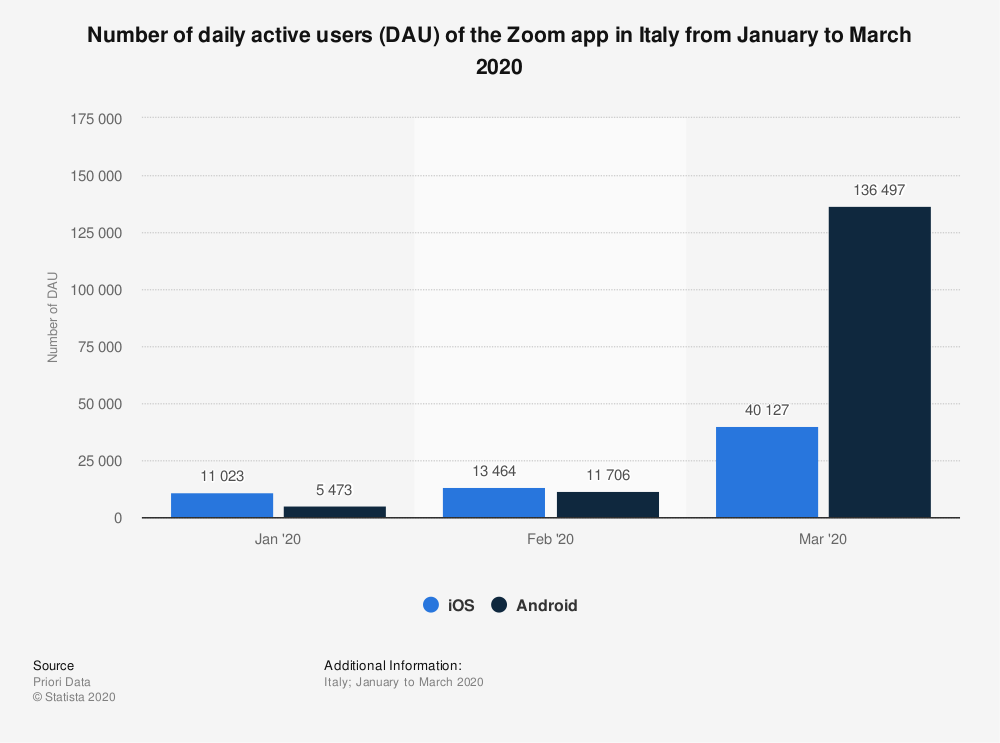

A Deeper Dive on Zoom Stock

Consumers won’t completely abandon Apple’s (NASDAQ:AAPL) FaceTime calls or Zoom’s group-video chats once we can get out freely and spend time together. However, they will certainly spend less time using these platforms to communicate.

That doesn’t mean everything will be that way, though. Twitter (NYSE:TWTR) and Square (NYSE:SQ) have already committed to allowing their workers to work from home as long as they want.

Facebook (NASDAQ:FB), Visa (NYSE:V) and Alphabet (NASDAQ:GOOGL, NASDAQ:GOOG) have said that those who can work remotely can do so through year-end.

This trend is an employee benefit. It’s not just big tech doing it either. Tons of other firms — large and small — are quickly adapting to the new world. They’re seeing the convenience and the cost savings. It equates to less travel expenses and will lead to lower rent bills if less office space is required. While this may be a problem for the commercial real estate market, it will be a boon for companies like Zoom Video.

It’s why Zoom recently had 300 million participants in one day at the end of April. That’s up from 200 million at the beginning of the month and just 10 million in December. We’ve seen the growth in Microsoft (NASDAQ:MSFT) Teams too, which had 75 million daily active users near the end of April. That’s up from 44 million in the prior month.

While the explosive growth trend here won’t last, many of these customers will remain customers. For Zoom, I’m not sure how things could have lined up any better. A surge in usage will allow Zoom to capture more customers much more quickly than previously thought. That bodes well for sustained growth.

Valuing ZM Stock

Click to Enlarge

However, growth is not the issue with Zoom stock.

Analysts predict revenue will hit $931.4 million this year, up almost 50% from 2019. They predict another 34% jump in 2021, which would send revenue up to $1.25 billion.

On the earnings front, analysts expect profit of 43 cents per share this year, followed by 53 cents per share in FY 2022 (next year). Both estimates have inched higher considerably over the last two and three months, too. Zoom Video was actually profitable before Covid-19 and should remain that way long after — so the coronavirus is not just a short-term bump in profit.

That said, this stock is expensive. Zoom stock commands a market cap of more than $48 billion, towering over its sub-$1 billion in expected sales this year. Even based on next year’s numbers, ZM still trades at ~39 times forward revenue.

Because of the valuation, we want to wait for a dip-buying opportunity. Ultimately, this is a well-run company with long-term secular growth potential. Further, it has a clean balance sheet — current assets of $1.1 billion easily top current liabilities of $333.8 million — while free cash flow has been positive for the last four years. But it’s expensive and we have to respect the valuation.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.