Costco Wholesale (NASDAQ:COST) did not get the type of pre-earnings or post-earnings love that many of its peers in retail received. With shares still notably off the highs, I like COST stock on this prolonged pullback.

What companies are considered Costco’s peers? There’s a divide in retail and it can be summed up like this: there are those that are working on thriving and those working on surviving.

In Costco’s class, I would consider companies like Walmart (NYSE:WMT), Target (NYSE:TGT), Home Depot (NYSE:HD) and even Amazon (NASDAQ:AMZN). Best Buy (NYSE:BBY) isn’t doing too bad, either.

All of these companies have a few things in common. With the exception of Amazon, these brick-and-mortar retailers are successfully building out the online arm of their business. They are also doing well amid the novel coronavirus outbreak. Unlike many other retailers and businesses, they are deemed essential and are benefiting from a wave of consumer demand, rather than suffering massive sales and earnings droughts, like Macy’s (NYSE:M) and

J.C. Penney (NYSE:JCP).

COST Stock Has a Moat

So what does any of this have to do with Warren Buffett?

Because there are those that are thriving and those that are struggling to survive, clearly the former has something that the latter does not. That my friends, is a moat — a Buffett favorite.

Costco most certainly has a moat. It has a recurring revenue stream via its annual membership. Most retailers do not have such a model, with the exception of Amazon via Prime. However, unlike Amazon, a membership is all but required to shop at Costco (save for certain items in certain states). This recurring revenue stream is more akin to a software company, which really commands a high valuation. In other words, Costco is like a software company masquerading as a retailer and this makes its stock look cheap in comparison.

Having a membership (ranging between $60 and $120 a year) gives customers access to a bevy of bulk-item deals. While Costco refrains from passing along price hikes that other retailers may take advantage of, management focuses on passing along the best deal to consumers.

In the end, this is a win-win. Costco still generates strong earnings and revenue (again, with the aid of membership sales), while customers save on most items vs. traditional retailers. This works especially well for families.

A Fit for Buffett

While Costco’s premium brand has resulted in a premium valuation, I still think this fits Buffett’s outlook. A resilient retailer with a strong moat — about 90% of customers renew their membership — consistent demand even amidst a pandemic should grab the Oracle’s attention.

As I say all of this, it has grabbed his attention. Costco is a current holding in the Berkshire Hathaway (NYSE:BRK.A, NYSE:BRK.B) portfolio. But with a stake of “just” $1.23 billion, it only represents 0.7% of the portfolio.

However, the resilience of Costco’s business model should make the stock more attractive amid Covid-19. Bloomberg argues that COST stock is ripe for a larger stake by Buffett & Co. They argued:

Costco has proven during this crisis that it has a durable brand and a wide competitive moat, two of the key attributes Buffett looks for … Those warehouse memberships are a predictable source of cash flow, almost akin to Berkshire’s insurance float that Buffett uses to invest.

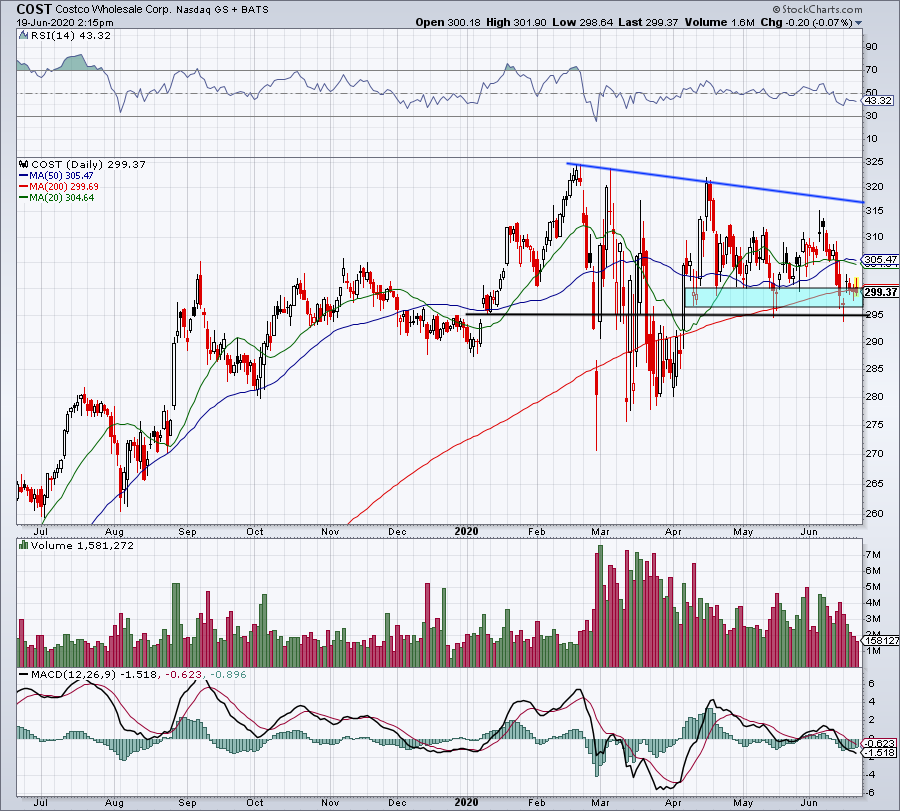

Valuing Costco Stock

Click to Enlarge

Earlier I mentioned a premium valuation, and that has always been present with Costco. At 35 times this year’s earnings estimates, I would consider that an elevated, premium valuation.

However, management has been vocal about taking extra costs and precautions with Covid-19, which is forecast to limit bottom-line growth to just 2.8% this year. Next year, analysts expect COST stock to grow earnings by 10%. On the revenue front, estimates call for steady growth of 6.8% this year and 6.1% next year.

This valuation did not suddenly increase from the coronavirus. COST stock has traded with a premium valuation for years — that’s just the way it is.

Down about 7.5% from the February highs, Costco continues in a sideways trading pattern. For the moment, shares are holding in around the 200-day moving average, 50% retracement near $297.50, and the $295 to $300 zone.

If this zone breaks, it could put $291 in play (which is the 38.2% retracement), or lower. However, a move over the 50-day and 20-day moving average could spark a rally up to the $310 to $315 area. That may allow for a test of downtrend resistance.

In any regard, we like COST stock for the long term and the current discount gives investors an opportunity to begin accumulating a position.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.