Despite the volatile price action in the broader market, Salesforce.com, Inc. (NASDAQ:CRM) has been rather steady. Will that pattern continue going forward? I think it will, as Salesforce stock should continue its “quick and steady” gains higher.

Already CRM stock is up 19% on the year, dwarfing the gains of the SPDR S&P 500 ETF Trust (NYSEARCA:SPY) and the PowerShares QQQ Trust, Series 1 (ETF) (NASDAQ:QQQ), which are flat and up 4%, respectively.

Also for the record, Salesforce stock is up 45% over the past 12 months.

The average price target on Wall Street calls for CRM to rally 13% to $137.50. The highest target calls for a 31% rally to $160 and heck, even the lowest price target isn’t very encouraging for bears. It sits at just $116, less than 5% below current levels.

Investors should consider buying a 5% pullback, not selling. Here’s why.

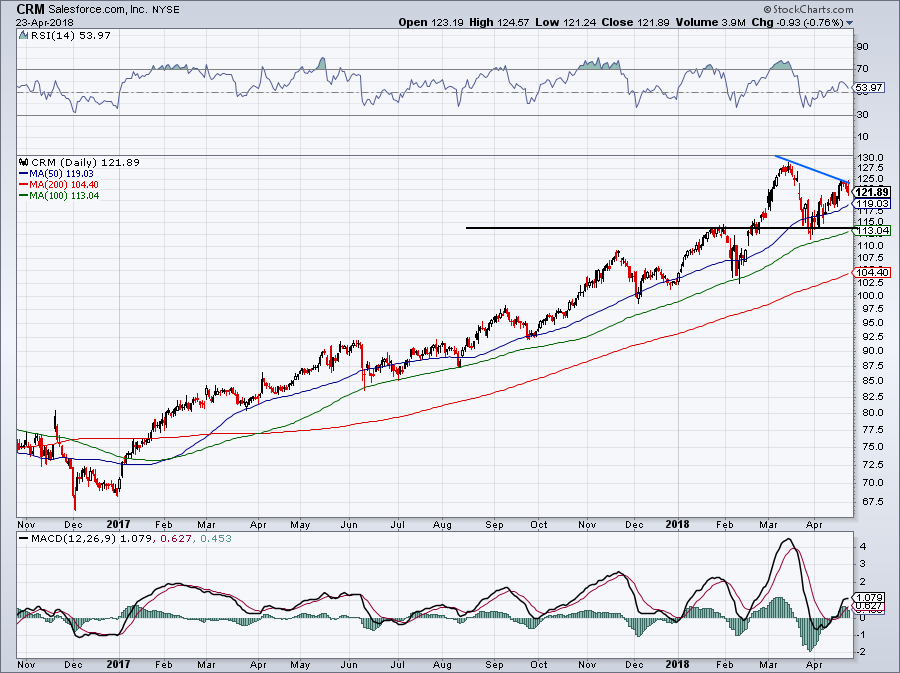

Trading CRM Stock

I would draw a trendline on the chart below, but it’s pretty cut and dry: Salesforce has been a beast. In fact, the stock’s best trendline at this point is its 100-day moving average (in green).

Click to Enlarge

For new investors or investors looking to grow their stake, pullbacks to the 100-day moving average should be bought. That’s been the case since June, down near $85. Shares have rallied $36 or more than 40% since then. Not too shabby.

At current prices, a retest of the 100-day would require a pullback down to $113, although by the time CRM pulls back, the 100 day may very well be higher than its current measure. Additionally, this $115 area has some support beyond just the 100-day; it’s got level support too (black line).

There’s slight downward resistance as well (in blue), but I don’t expect that to derail CRM’s long-term uptrend.

Further, enterprise software, cloud and similar businesses to CRM have been holding up well. That’s despite the increased volatility in the market as of late, as these names have done well on the market’s down days. That should excite investors, as these will be the go-to names once the market turns more bullish.

Microsoft Corporation (NASDAQ:MSFT) is another one that’s been acting very well.

Why We Like Salesforce Stock

There are plenty of reasons to like CRM at this point. One of the main reasons? That Salesforce is operating in an industry that’s seeing accelerating growth. Cite the economy or the tech industry (or both), but the company’s business and many others continue to do very well.

That’s what’s allowing these companies to hold up better than other industries and sectors; not necessarily rally amid market declines, but still the point stands. That’s very encouraging price action.

Cloud computing growth isn’t slowing down, as evidenced by visible through Amazon.com, Inc. (NASDAQ:AMZN), Adobe Systems Incorporated (NASDAQ:ADBE) and even the recent earnings results from Alphabet Inc (NASDAQ:GOOGL, NASDAQ:GOOG).

The industry continues to fire on all cylinders and while many folks may have thought that the cloud is the past and artificial intelligence is the future, they may be overlooking how much growth is still left in the cloud.

All in all, this bodes well for CRM stock and it still has a long runway of growth.

CRM Growth

How much runway? Analysts are looking for strong growth this year. On the revenue front, estimates call for 21% growth this year (fiscal 2019) and more than 19% next year (in fiscal 2020). Longer term, expectations call for roughly 20% revenue growth over the next four years.

However, that may not be enough. Expectations for 2022 call for $19.8 billion in sales, but CEO Marc Benioff has continually said management sees a clear path to $20 billion in sales by 2022. That may not seem all that special, but consider that 2018 sales were “just” $10.5 billion. So revenue should essentially double between then and 2022.

It becomes more realistic considering that the Salesforce stock deferred revenue grew 28% year-over-year last quarter.

Let’s not forget about the bottom line either: Earnings are set to grow almost 60% this year and over 25% in the following year. While CRM isn’t quite known for its earnings power, it’s clear Salesforce has momentum in both its business and its stock.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell held a long position in CRM and GOOGL.