Alibaba’s (NYSE:BABA) shares fell 1% on Thursday in the wake of the company’s fiscal first-quarter results. The shares dropped despite the conglomerate’s stronger-than-expected top- and bottom-line results.

There is a lot of pessimism towards Alibaba. That’s because, since it’s headquartered in China, it could be delisted by the U.S. government. The stocks of all Chinese companies face that risk now.

However, Alibaba is benefiting from several non-cyclical growth trends, as its Q1 earnings showed. With the stock’s charts cooperating, the shares may be well-positioned at this point.

Alibaba Reported Strong Earnings

The company’s fiscal Q1 earnings of $2.10 per share came in 14 cents ahead of analysts’ average outlook. Its revenue of $21.76 billion grew 34% year-over-year and beat analysts’ mean estimate by almost $500 million.

Alibaba CFO Maggie Wu said:

“Our domestic core commerce business has fully recovered to pre-COVID-19 levels across the board, while cloud computing revenue grew 59% year-over-year. Our strong profit growth and cash flow enable us to continue to strengthen our core business and invest for long term growth.”

The company’s major business units are tied to the strong non-cyclical growth trends of e-commerce and cloud computing. As shown by the results of JD.com (NASDAQ:JD), Amazon (NASDAQ:AMZN), eBay (NASDAQ:EBAY) and others, e-commerce remains quite strong.

Even companies that are not traditionally associated with e-commerce have reported very strong digital sales. Among the names in that group are apparel brands Nike (NYSE:NKE) and Lululemon Athletica (NASDAQ:LULU), as well as big-box retailers Target (NYSE:TGT) and Walmart (NYSE:WMT).

The beauty of e-commerce is that it was in a long-term uptrend before the novel-coronavirus pandemic. The virus is simply accelerating this trend, as Alibaba’s results showed.

Breaking Down Alibaba Stock

Analysts, on average, expect Alibaba’s earnings per share to rise about 16% this year to $8.76, and the mean top-line estimate calls for growth of 32%. Some may argue that, with the shares trading at a price-earnings ratio of 29 times, based on the average 2020 EPS estimate for Alibaba, they are too expensive.

I would argue that, for several reasons, their valuation is not excessive.

First, the company’s revenue-growth outlook is better than many of its mega-cap-tech peers, including Facebook (NASDAQ:FB), Microsoft (NASDAQ:MSFT), Amazon (NASDAQ:AMZN), Apple (NASDAQ:AAPL) and Alphabet (NASDAQ:GOOGL, NASDAQ:GOOG). Its current P/E ratio is also lower than those names. Revenue growth and P/E ratios are not the only things that matter, but those metrics show what a reasonable investment Alibaba is.

Alibaba’s business certainly isn’t slowing down, as its chairman and CEO, Daniel Zhang, noted on its Q1 earnings conference call:

“We were well positioned to capture growth from the ongoing digital transformation, which has been accelerated by the pandemic, in both consumption and enterprise operations.”

The company’s strength is also reflected in next year’s average forecasts, which call for 26% revenue growth and 28% earnings growth.

Second, I agree with Alibaba’s decision to prepare for the potential escalation of trade tensions between the U.S. and China. It’s planning to list Alibaba stock on Hong Kong’s stock exchange. Further, it has a 33% stake in Ant Group which is looking to list its shares in Shanghai and Hong Kong. Ant is not a small entity, as it is seeking a $225 billion valuation through its IPO.

Trading Alibaba Stock

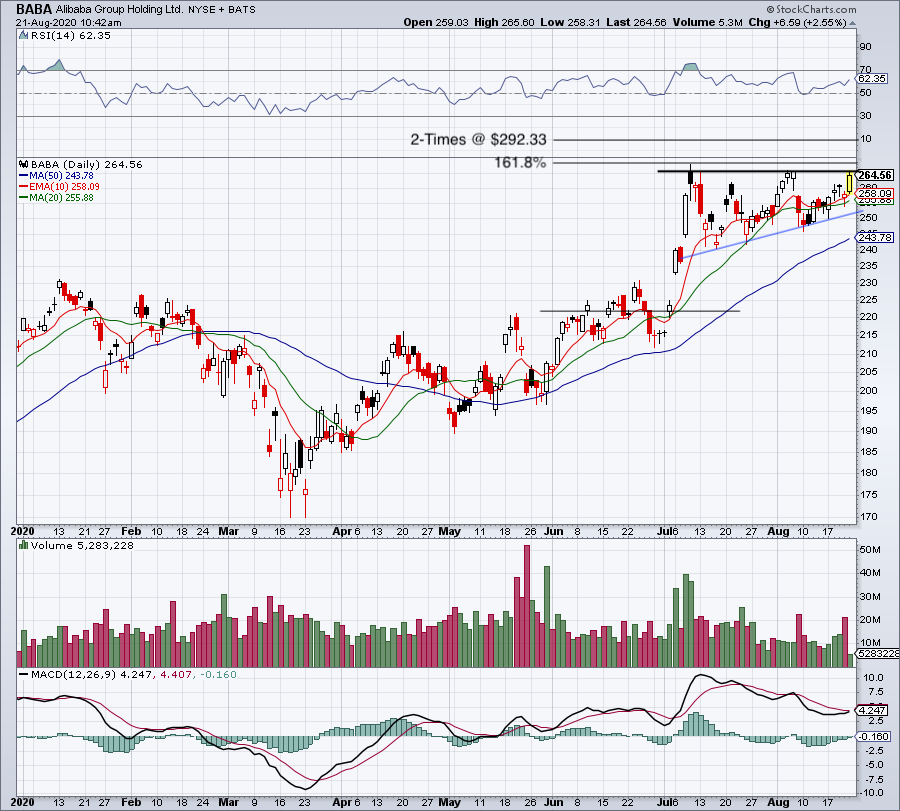

Click to Enlarge

As shown by the nearby chart, Alibaba has been consolidating since early July.

The shares have been moving into a sideways pattern, but they are trying to climb. Their limited reaction to the company’s earnings can be viewed as positive, given the strong results it reported.

Still, the shares have not yet confirmed that they are heading higher. The $265 level has been clear resistance, with the 161.8% extension level just over the stock’s prior high which is near $269.

If Alibaba stock can clear this $265 to $269 area, it will ultimately put the two-times range extension near $292 and the $300 mark on investors’ radar. On the downside, a break of the 10-day and 20-day moving averages and a break below its support level will put the 50-day moving average in play.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long AMZN and AAPL.