Buying the dips and acquiring shares of a proven company on short-term declines has been a successful strategy over the long-term. When investors look back five or 10 years from now, the opportunities which presented themselves during the Great Recession, the COVID trough, or even the recent downturn in 2022 were worth buying. Of course, it may not have felt that way at the time. But that’s why buying undervalued stocks with solid future prospects is important to do in good times and bad.

I think these undervalued stocks could surge back just like the Magnificent 7 did after their respective downturns. By investing in these companies, you could potentially triple your money by 2026.

Here are seven undervalued stocks to consider right now.

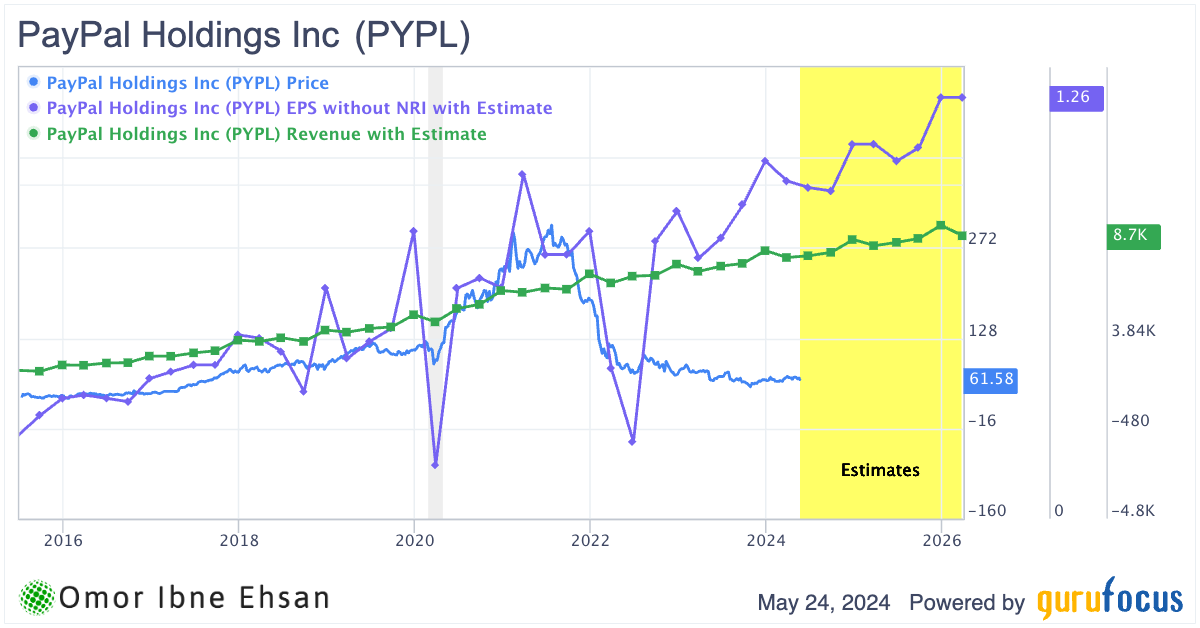

PayPal (PYPL)

PayPal (NASDAQ:PYPL) didn’t post the best results this past earnings season. There are some promising signs with this fintech giant. But important work must be done to get the company back on track. PayPal reported $7.7 billion in revenue, beating analysts’ estimates by $183 million. However, earnings per share of $1.08 fell short of projections by 14 cents.

Early testing of the company’s new Fast Lane checkout experience is yielding nearly a 10% increase in conversions for first-time users. Rolling this out more broadly in Q2 could provide an even more meaningful meaningful boost.

This company has an unshakable merchant base and is a household name. I do not think PYPL stock will remain at these valuations forever, given the level of buybacks they’re doing and revenue growth expected to remain around 8% annually. User account growth is the most important metric with PayPal, and while this number fell following the pandemic, it has turned positive again, at least on a quarterly basis. Thus, the recent decline in PYPL stock seems very irrational given the underlying fundamentals.

Click to Enlarge

Based on the better-than-anticipated first-quarter results, management now expects full-year earnings per share growth in the mid-to-high single-digit percentage range. This is an increase from previous guidance. The payments giant still has significant work ahead to prove a successful turnaround. But if PayPal can effectively execute on its plans, the stock may deliver strong returns from current levels.

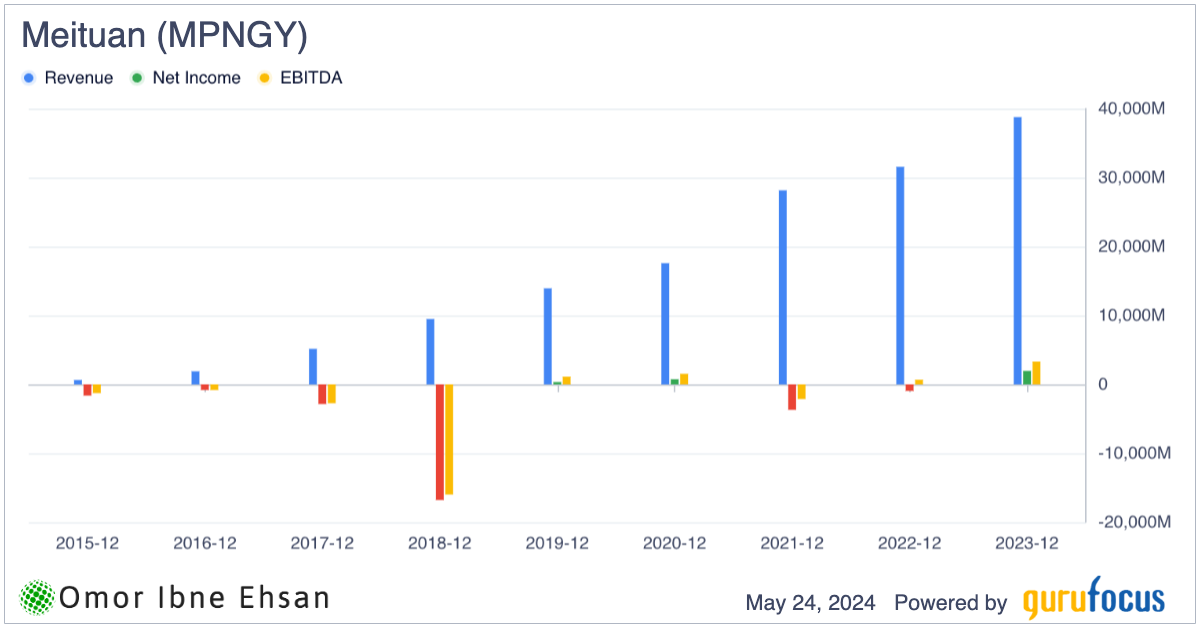

Meituan (MPNGY)

Meituan’s (OTCMKTS:MPNGY) latest business update made me feel very optimistic about the company’s growth trajectory. Many solid Chinese companies have plunged due to China’s broad-based decline in its stock markets. However, Chinese stocks have been recovering well recently, and I think Meituan has a long road of recovery ahead.

With revenue surging nearly 26% to reach RMB 276.7 billion and adjusted net profit skyrocketing to RMB 23.3 billion in 2023, Meituan seems to be firing on all cylinders. The food delivery giant is capitalizing on the rapid growth in China’s local commerce industry, with daily order volumes jumping almost 24% to a staggering 60 million.

But what really excites me is Meituan’s relatively new instashopping service. In my opinion, that part of the business is the real gem. Orders for this segment soared over 40%, as the company successfully cultivated the habit of receiving everything you need within 30 minutes.

I wouldn’t be surprised if the company’s share price tripled over the next few years if Meituan remains profitable.

Click to Enlarge

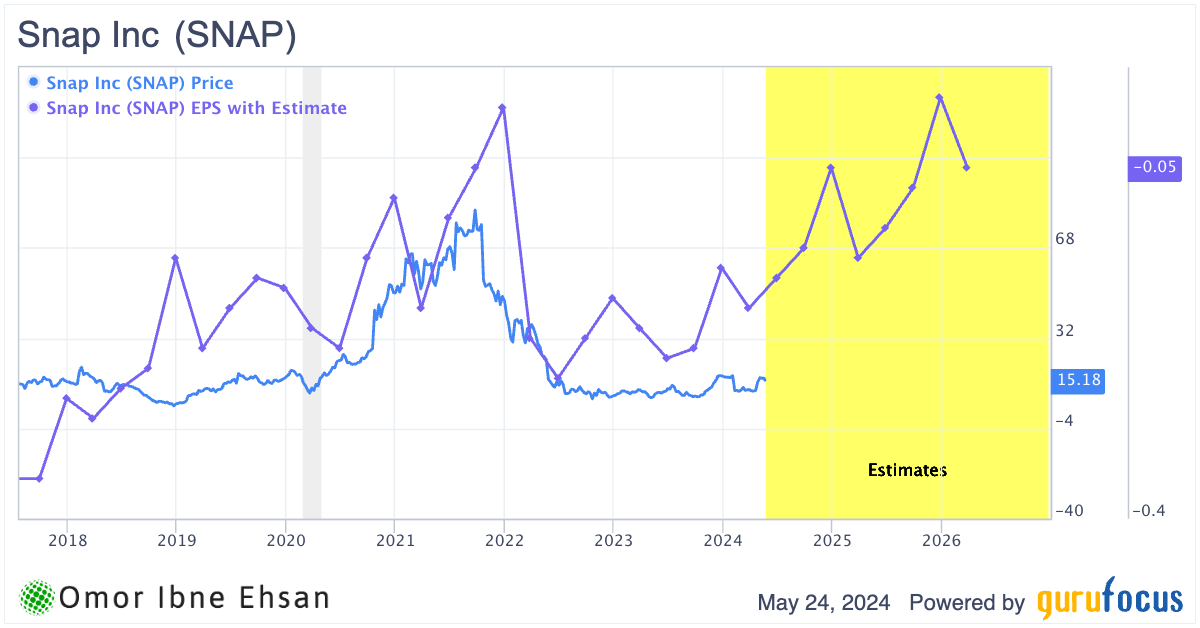

Snapchat (SNAP)

Snapchat (NYSE:SNAP) is arguably the most undervalued social media stock you can buy right now. I think this stock could have a recovery that mirrors that of Meta’s (NASDAQ:META).

That’s partly due to the company’s strong Q1 results, which have made me feel optimistic about the company’s trajectory. With revenue accelerating 21% year-over-year to $1.19 billion and daily active users growing 10% to 422 million, Snap is showing real momentum. I’m particularly encouraged by the 75%+ growth in purchase-related conversions driven by their 7-0 Pixel Purchase optimization model. The company’s earnings per share outlook also looks solid, which is why I think Snap could mirror Meta’s performance.

Click to Enlarge

If Snap can continue executing on its strategic priorities of diversifying revenue, growing engagement, and leading in AR, I believe the stock has serious multi-bagger potential by 2026. The company’s ability to reach over 75% of 13-34 year-olds in 25+ countries representing half the global ad market is a major asset.

I think a potential TikTok ban in the U.S. could be a massive catalyst for Snap. The company would be a clear prime beneficiary in terms of both users and ad dollars. TikTok’s issues could become Snap’s opportunity.

With strong Q1 numbers and several potential growth levers, Snap looks like a compelling buy for patient investors willing to hold through 2026.

Sprinklr (CXM)

I feel optimistic about Sprinklr’s (NYSE:CXM) future despite the “premium” valuation associated with this stock. The company’s revenue grew by 17% year over year to $194.2 million, handily beating the forecasts. Additionally, recurring subscription income grew solidly by 19% to $177 million.

In my opinion, Sprinklr seems to be making smart strategic moves to set itself up for continued growth. Bringing in experienced executives like Trac Pham as interim chief operations officer and Amitabh Misra from Adobe as chief technology officer could be a real difference-maker in terms of their operational expertise.

Most exciting is Sprinklr’s opportunity in the evolving field of generative artificial intelligence. After 14 years spent building a robust backend foundation, the company provides plenty of AI exposure to investors. And yes, you are paying 31-times forward earnings for this stock. But as long as Wall Street holds up that premium as earnings rise, this stock could still deliver solid returns in the coming years.

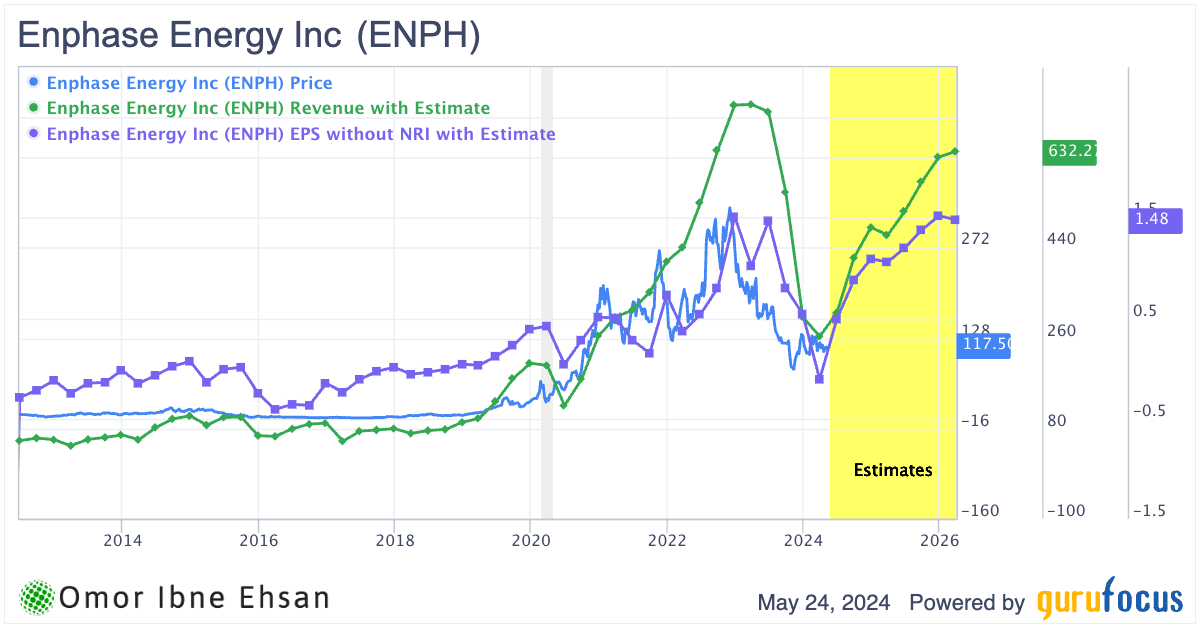

Enphase Energy (ENPH)

Enphase Energy (NASDAQ:ENPH) is a renewable energy company focused on solar. Much like the EV industry, the solar industry has had difficulties in recent quarters. Most new flashy businesses in industries that require lots of capital have plunged. Accordingly, the latest report on Enbridge’s business performance also reveals the company is facing challenges in current market conditions. Revenue for the quarter came in at $263.3 million, down 63.7% year-over-year. This was well below the level financial analysts had predicted. Shipments of their microinverters and battery storage systems, at 1.4 million units and 75.5 megawatt hours, respectively, were also lower than hoped.

The number of microinverters and batteries sold to final customers in the U.S. dropped 23% from the previous quarter. That’s a worrying sign that demand may be decreasing. Notably, the situation in California was particularly weak, with sales of microinverters there falling 37%. The transition to their new NEM 3.0 energy program is clearly impacting business.

Gross profit margins at 46% look okay at first glance. However, this number benefitted from tax credits available through the Inflation Reduction Act. Cash flow generation slowed as well, coming in at just $41.8 million for the period. With $113 million worth of products still sitting in inventory in the sales channel, Enphase’s near-term business prospects seem uncertain. That said, if an investor is willing to hold the stock for the long-run, I’m confident Enphase can deliver solid returns.

Click to Enlarge

Analysts expect earnings per share to rise from $2.9 in 2024 to $6.3 in 2026. If that’s the case, this stock could be worth a buy, despite all the hair on it.

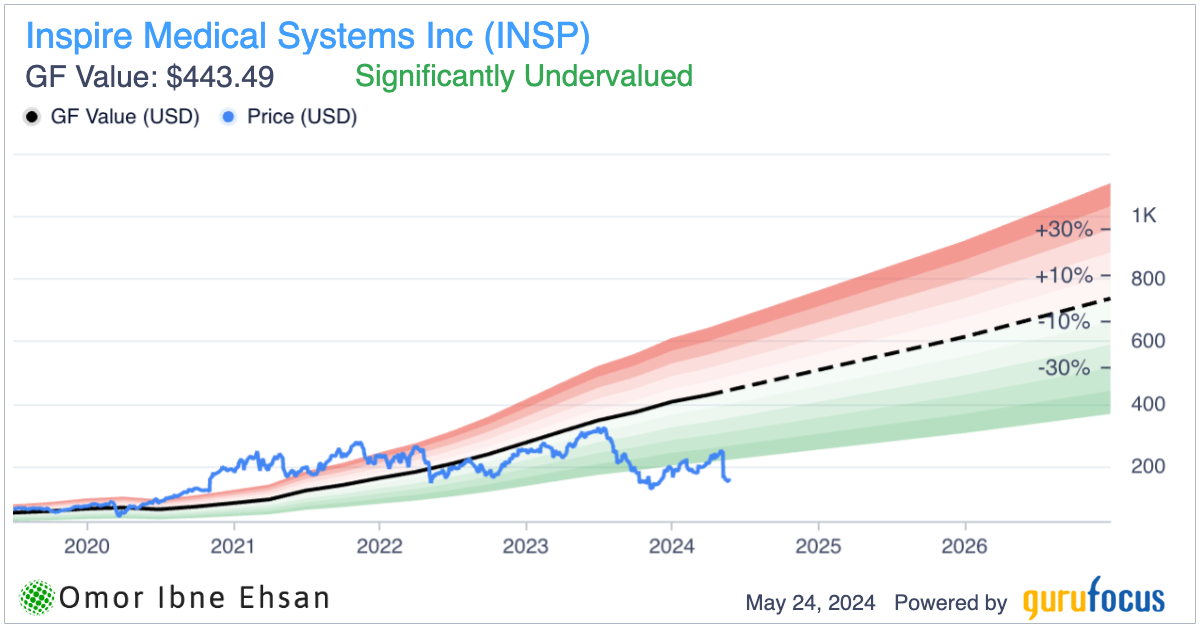

Inspire Medical Systems (INSP)

I’ve been keeping a close eye on Inspire Medical (NYSE:INSP) for some time now. While the company may not be a household name, I believe Inspire has tremendous potential to grow in the coming years.

Inspire delivered very impressive results in Q1, with revenue increasing by 28% year-over-year, reaching $164 million. This strong growth was being driven by greater adoption of the company’s sleep apnea therapy solutions in both the United States and international markets. Based on this positive momentum, Inspire’s leadership team updated their revenue guidance for the full year to a new range between $783-793 million and targets continued growth of 25-27%.

Inspire is not profitable right now, but it expects to be profitable for all of 2024. The company’s management team provided initial guidance estimating their earnings will be somewhere in the range of 10-20 cents per share. As their business matures and they gain efficiencies, I foresee their profitability increasing sharply from here. This could lead to tremendous upside. Analysts expect 2026 earnings per share to come in around $2.20, and if you zoom out, this figure could reach as high as $10 in 2031.

You’re paying a premium for sure, so this stock is not really one of the “undervalued stocks,” if you look at it from a near-term perspective. But with the long-term trend in mind, I think it fits.

Click to Enlarge

Alkami Technology (ALKT)

Alkami Technology (NASDAQ:ALKT) is a tech company that provides a platform for financial institutions. I think it has great potential for continued success and growth over the coming years. In Q1, the company increased revenue by an impressive 27% to $76 million while achieving $3.8 million in adjusted EBITDA, exceeding even optimistic projections.

What particularly piqued my interest was the CEO noting their addressable market estimate has expanded to 480 million potential user accounts, up from 370 million at the time of their initial public offering in 2021. According to Alkami’s research, 58% of regional banks and credit unions are open to switching to a different digital banking platform provider. That’s a big opportunity.

I expect Alkami’s growth trajectory to become even steeper over time, as earnings per share rises from 21 cents in 2024 to 88 cents in 2026.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.