U.S. equities pushed new record highs on Tuesday thanks to better-than-expected results from Caterpillar Inc. (NYSE:CAT) and McDonald’s Corporation (NYSE:MCD) before the open, leading the stocks to finish with gains of 5.9% and 4.8%, respectively. And more is on deck, with Amazon.com, Inc. (NASDAQ:AMZN) reporting after the close on Thursday.

In the end, the Dow Jones Industrial Average gained 0.5%, the S&P 500 gained 0.3%, the Nasdaq Composite gained a fraction and the Russell 2000 gained 0.9%.

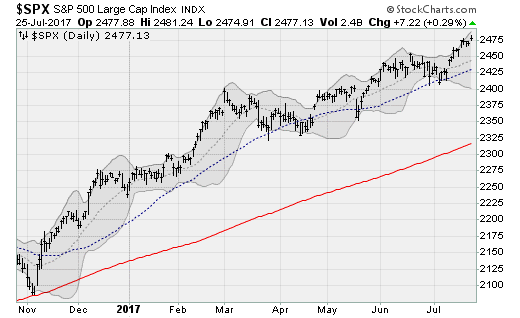

Guide: Red = 200-day moving average, Blue = 50-day moving average

Treasury bonds weakened with the iShares 20+ Year Treasury Bond (NYSEARCA:TLT) down 1.3%, pushing up long-term rates. The dollar was mixed, gold fell a touch and oil gained for the second day with attention on recent Saudi and Russian efforts to bolster production cuts resulting in the best one-day gain of 2017 up 3.3%.

Breadth was positive, with advancers outpacing decliners 1.6 to 1 on heavy volume at 132% of the NYSE’s 30-day average. Financials led the way on net interest margin tailwinds from higher rates, gaining 1.3%. Healthcare was the laggard, down 0.7%, as the Senate voted 51-50 to proceed with debate on legislation to repeal or repeal/replace Obamacare.

Copper and gold miner Freeport McMoRan Inc (NYSE:FCX) gained 14.7% after issuing improved forward guidance amid a rally in copper prices today. AK Steel Holding Corporation (NYSE:AKS) added 12.4% on better-than-expected earnings and revenues. CAT surged on a big beat in equipment sales to the construction industry and raised guidance. And MCD rose on solid global comp-store sales growth of 6.6% vs. the 3.7% analysts expected.

Guide: Red = 200-day moving average, Blue = 50-day moving average

On the downside, Alphabet Inc (NASDAQ:GOOG, NASDAQ:GOOGL) fell 2.9% — pulling the “FAANG” stocks lower in a rare decline — amid concern about softer margins. 3M Co (NYSE:MMM) fell 5.1% on a top- and bottom-line miss.

Investors are bracing for the conclusion of a two-day Federal Reserve policy meeting on Wednesday.

While no rate hike is expected (and isn’t predicted until December according to the futures market) policymakers are likely to hint at the start of a “quantitative tightening” program at its meeting in September. This, if done, would represent the beginning of the process to scale back the Fed’s $4.4 trillion balance sheet bloated by years of asset purchase stimulus.

Guide: Red = 200-day moving average, Blue = 50-day moving average

The bond market seems to be bracing for this already, with long-term Treasury bonds selling off hard as shown above.

Higher long-term interest rates translate directly into higher profitability for banks. As a result, the Financial Select SPDR (NYSEARCA:XLF) is up 1.3% jumping the high set in March. The move looks fresh and could be accelerated by confirmation the Fed’s QT program is coming on Wednesday afternoon.

Conclusion

The most marked feature of the market right now is the historic lack of volatility. There was some action in currencies through last week, with the U.S. dollar sliding hard, but even that has dissipated away this week. With the Fed on deck tomorrow, AMZN earnings on Thursday, and Apple Inc. (NASDAQ:AAPL) reporting on Aug. 1, one wonders if the tranquility can last.

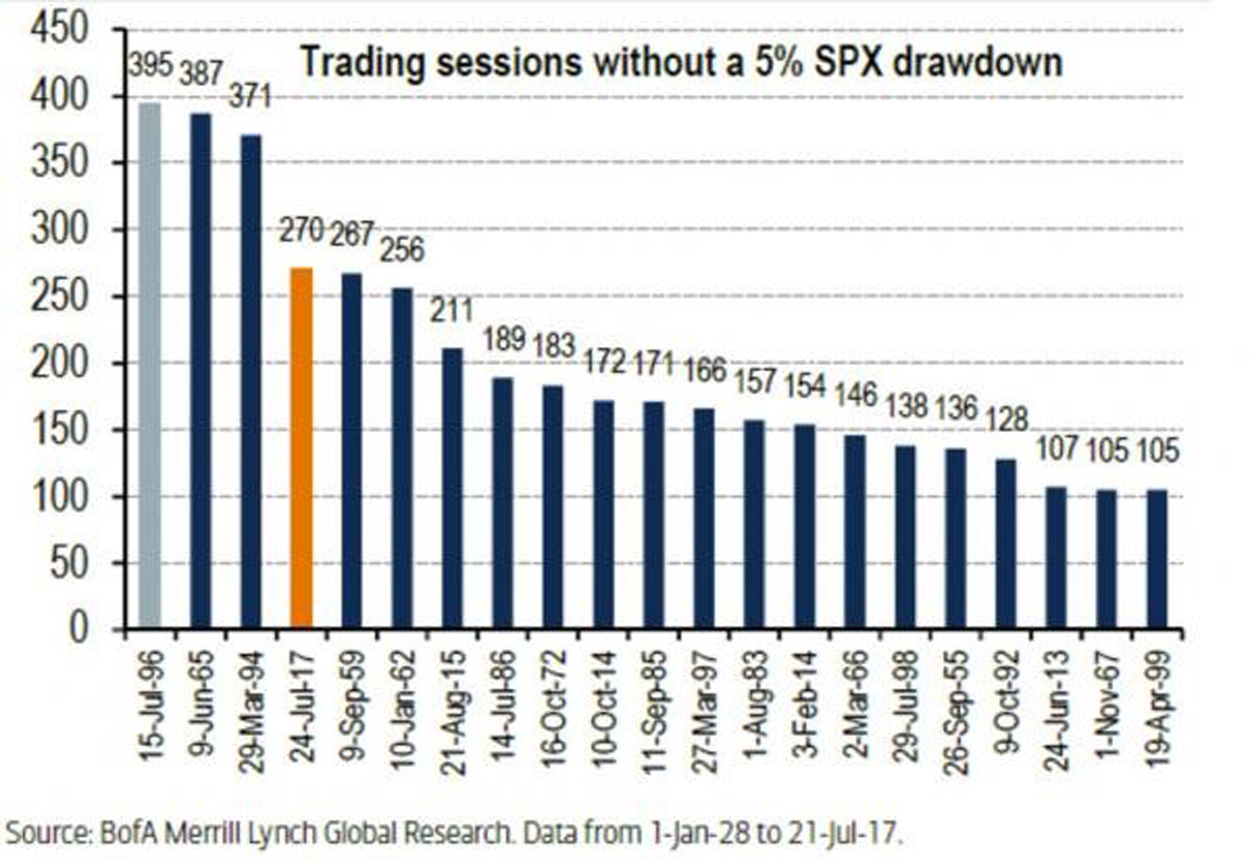

Because on multiple measures, this is historic: Representing the fourth-longest stretch of “dip-less” stock market gains in 90 years. The last major pullback was more than a year ago, represented by a touch of the 200-day moving average by the Dow Jones Industrial Average.

Looking at the S&P 500, Bank of America Merrill Lynch notes that the market’s 1965, 1994, and 1996 uptrends without a 5% drawdown were longer lived, as shown above.

Amid this, the CBOE Volatility Index has been below 10% for the last nine days straight. Ever since Fed chairman Janet Yellen’s semi-annual testimony to Congress talked up the likelihood that interest rates would top out at a relatively low level during this tightening cycle. This “dovish” comment was all it took to unleash a powerful “creeper” uptrend throughout July.

This is the VIX’s longest run below 10 in its history.

But evidence of fatigue is showing. Treasury bonds are weakening, as they did in late June, potentially pressuring “risk parity” funds. The FAANG stocks weakened for the first time in 13 days on GOOGL’s pullback. And a number of major catalysts lie ahead, mainly the Fed’s policy announcement tomorrow in which Yellen and her cohorts will get one last chance to prepare the market for a slow pullback of their bloated $4.4 trillion balance sheet.

Deutsche Bank economists expect Fed officials to firm up its balance sheet guidance to indicate that the “Committee currently expects to begin implementing a balance sheet normalization program at upcoming meetings.”

This could very well uncork some equity market volatility as traders realize the Fed is serious about draining the trillions in excess liquidity sloshing around the financial system; unleashing a pullback that is long overdue with the Dow, on a monthly basis, very extended from its 17-month moving average.

Extreme extensions away from long-term moving averages are akin to stretching a rubber band away from its unstressed state. The extension can persist, but it becomes increasingly difficult to hold it out. Same applies to stocks. As one of the most powerful forces — even larger then central banks and their cheap money — is the tendency for prices to revert to the mean.

Long-term moving averages can also be a long-term buy-sell indicator on crosses. The slope of the average can be a buy-sell indicator, but the most relevant takeaway right now is the extension as it is extreme.

Check out Serge Berger’s Trade of the Day for July 26.

Today’s Trading Landscape

To see a list of the companies reporting earnings today, click here.

For a list of this week’s economic reports due out, click here.

Tell us what you think about this article! Drop us an email at editor@investorplace.com, chat with us on Twitter at @InvestorPlace or comment on the post on Facebook. Read more about our comments policy here.

Anthony Mirhaydari is founder of the Edge (ETFs) and Edge Pro (Options) investment advisory newsletters. Free two- and four-week trial offers have been extended to InvestorPlace readers.