On Thursday, JPMorgan analysts came out with a positive note on Microsoft (NASDAQ:MSFT) and upped their price target on Microsoft stock to $125. From current levels, that implies “just” 6% upside. But just because MSFT stock has been on a tear doesn’t mean we should thumb our noses at a potential continuation of the rally.

And by “on a tear,” I mean a quiet one. For the last few months, Microsoft stock has actually held the crown of the largest U.S. company by market cap. With a market cap of roughly $900 billion, it’s ahead of Amazon (NASDAQ:AMZN) stock and its $871 billion market cap. More impressively though, MSFT stock, which has jumpred 32% in the last 12 months, is actually outperforming many of its peers over the past year.

While Amazon and Netflix (NASDAQ:NFLX) may be up big over the past few months, they actually trail Microsoft over the past 12 months, as AMZN and NFLX have risen just 29% and 27%, respectively during that time. Facebook (NASDAQ:FB), Apple (NASDAQ:AAPL) and Alphabet (NASDAQ:GOOGL

, NASDAQ:GOOG) have risen 7%, 12% and 17%, respectively over the last year, also trailing Microsoft stock.

So while Microsoft may not get as much recognition and attention as FAANG does, that doesn’t mean we should ignore this big-time winner.

Valuing MSFT Stock

Because of the big rally of Microsoft stock over the past year, its valuation has gotten more expensive. However, I would argue that MSFT stock is not too expensive given its growth, opportunity and quality.

MSFT trades at roughly 26 times analysts’ consensus 2019 earnings estimate, but the expectations for the company’s growth are solid and consistent. Analysts on average expect its revenue to grow 12.4% this year and 10.4% next year. Consensus earnings expectations call for the company’s bottom line to rise 14.2% this year and 12.6% next year. More promising is the fact that MSFT has beat consensus earnings estimates for 11 straight quarters and consensus revenue estimates in 9 of the last 11 quarters.

At times though, I don’t get the logic of investors. In this case, I question those who critique the valuation of Microsoft stock, but will defend a company like Procter & Gamble (NYSE:PG). With PG trading at more than 23 times this year’s consensus earnings estimates, how can anyone believe that MSFT can’t justify its valuation but PG can, with its 0.5 percentage points of revenue growth and the consensus outlook of 5,5% earnings growth?

Those who take that stance will argue that PG is a blue-chip name with a dependable yield. I’m sorry, but is Microsoft not considered a blue-chip stock at this point? Granted, PG has a long history of dividend hikes and pays out 2.9%, versus Microsoft’s 1.6% yield. But to call Microsoft stock overvalued isn’t fair, in my opinion.

All earnings season, we’ve seen companies like Microsoft, Accenture (NYSE:ACN), Salesforce (NASDAQ:CRM) and other cloud companies crush expectations. Because of that long runway, MSFT’s growth should continue. And since MSFT stock is as consistent as it is, I believe it can justify its premium valuation. Simply put, premium companies deserve premium valuations.

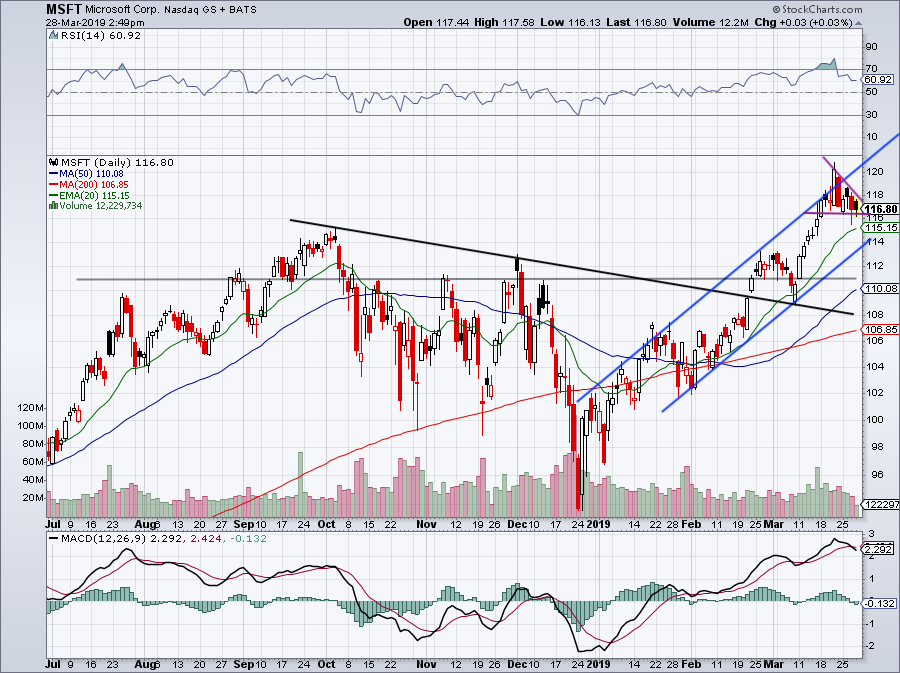

Trading MSFT Stock

Click to Enlarge

Many cloud companies recently provided optimistic full-year outlooks. However, many guided for a slightly weaker-than-expected first quarter. Microsoft also provided somewhat mixed guidance for the current quarter.

Could the cautious guidance hurt cloud stocks and/or tech names? Such weakness could create an opportunity to buy Microsoft stock.

We’ll find out more when MSFT reports its earnings. Until then, the charts actually look pretty good.

Since MSFT stock, currently trading near $119, has pushed back up through, $118, new highs are likely on deck and JPMorgan’s $125 price target for Microsoft stock is within reach.

Overall, short of a noteworthy market-wide correction, I don’t expect MSFT to come under too much pressure. Let’s not bet against this winner until its price action or fundamentals give us a reason to.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long AAPL, AMZN and GOOGL.