Growth stocks are some of the best bets you can make in the market due to the momentum in their business. Growth showcases strong demand and execution, and the market will happily slap a higher and higher premium for this growth as long as it is there. Thus, growth stocks often deliver some of the highest returns in the market and have a great risk-reward ratio compared to other types of stocks.

Buying growth stocks that have impressive profitability and have the cash to run the business until they hit profitability are some of the best bets you can make for the long run.

Let’s delve into seven growth stocks that are likely to perform well through 2025 and beyond.

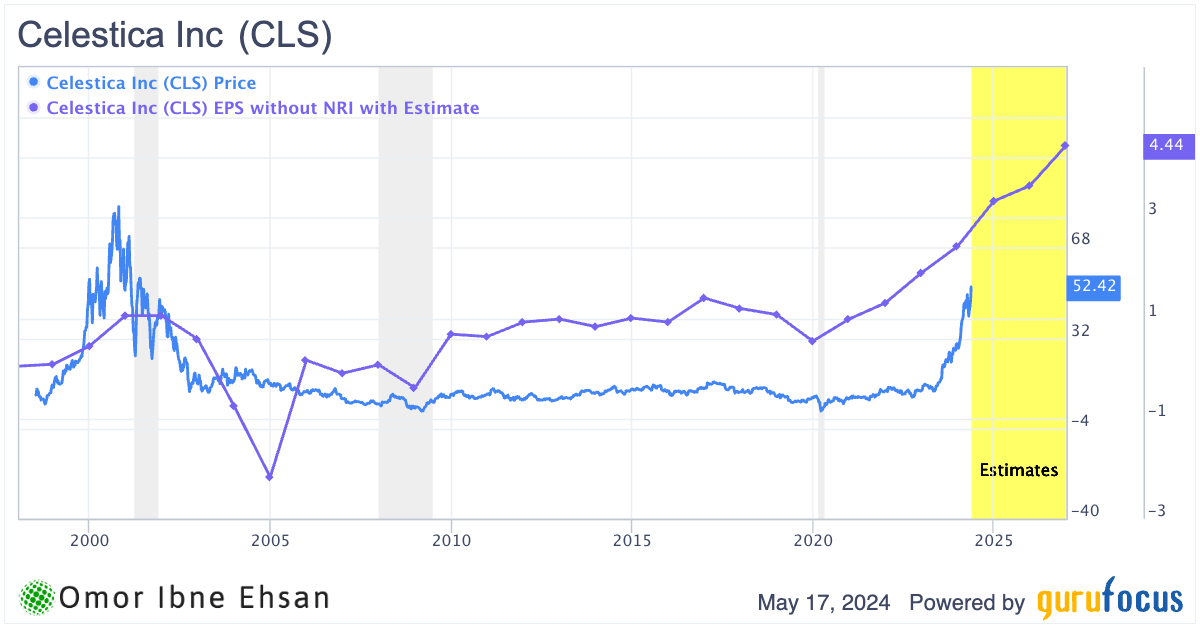

Celestica (CLS)

Celestica (NYSE:CLS) is a supply chain electronics manufacturing company. CLS stock has been delivering stellar gains and is up 366% in just the past year. However, it could climb even higher.

The firm’s Q1 results far exceeded expectations, with revenue growing 20.2% year-over-year (YOY) to $2.2 billion. Diluted EPS of 85 cents overwhelmingly beat analysts’ estimates by 15.4%. This was fueled by enormous demand from high-volume cloud computing customers in their Communications and Corporate sectors. The net margin in Q1 was just 4.6%, indicating ample room for future growth.

Click to Enlarge

While their Aerospace and Defense unit also continues achieving double-digit increases, the Industrial side encountered some challenges. However, management sees improving conditions ahead as orders for capital equipment rise again.

Investors are paying less than 16x forward earnings for all this, so it is a buy despite all the gains recently.

SkyWest (SKYW)

SkyWest (NASDAQ:SKYW) is up 172% in the past year but for the right reasons.

Its impressive Q1 showed EPS of $1.45, which was much higher than expected, coming in 26 cents above estimates. Revenue grew 16% YOY to $803.6 million. A big reason for this was a 5% rise in flight time. This growth shows that SkyWest’s pilot staffing challenges are starting to improve. And strong demand continues from their partners like United (NASDAQ:UAL).

While the charter side of SkyWest’s business remains small for now relative to everything else they do, prospects could strengthen as they move forward. I am very bullish due to the growth, and you’re still paying just 11 times forward earnings for this execution.

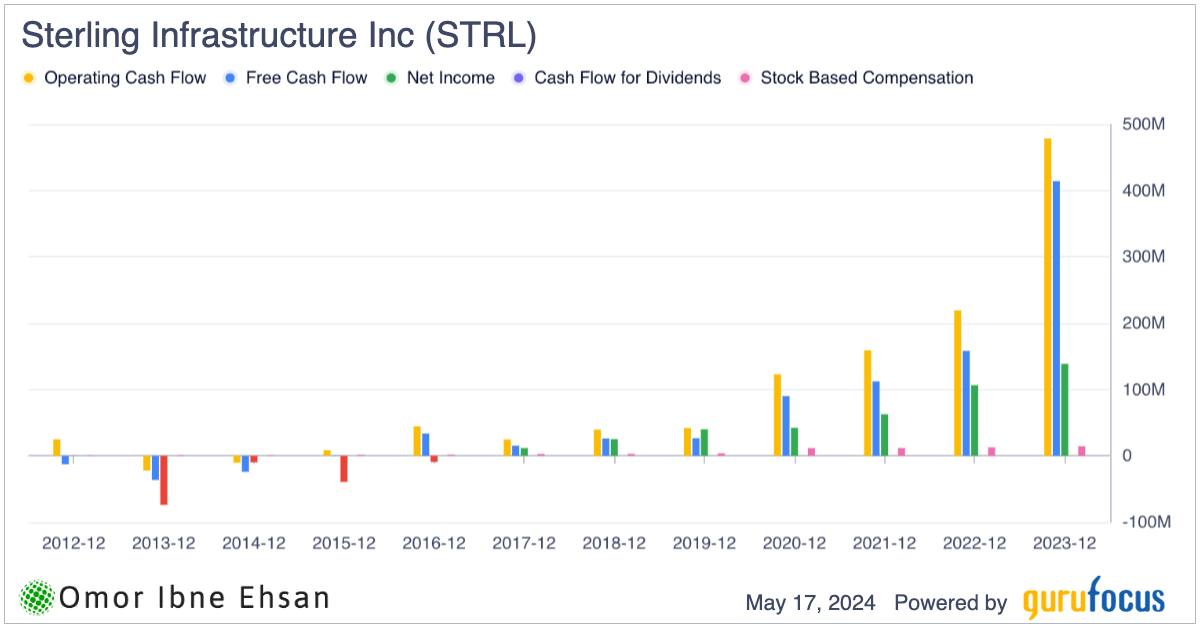

Sterling Infrastructure (STRL)

Sterling Infrastructure (NASDAQ:STRL) has been delivering stellar returns. This stock is up 980% in the past five years and up over 202% in the past year. However, this is not a pure momentum play by any means, as the company has the fundamentals to back up this surge.

It had a great Q1, with earnings per share reaching $1. This significantly beat analysts’ expectations by 18 cents, fueled by 9.1% revenue growth and margin expansion across all business segments. Also, order backlogs swelled to $2.35 billion, up 45% YOY. The cash flow growth has been tremendous so far.

Click to Enlarge

Additionally, double-digit profit growth in the Energy and Facilities segment despite revenues dropping 10% looks bullish. Likewise, operating income in this division rose 12% as supply chain challenges eased and the business mix shifted toward more profitable projects. With a hefty $961 million order backlog, up 32%, this segment looks ready for a strong 2024.

Analysts expect 18.6% EPS growth and 12.3% revenue growth for all of 2024. Recently, management raised guidance. So, along with the backlog swelling, I wouldn’t be surprised if they beat these expectations by big margins.

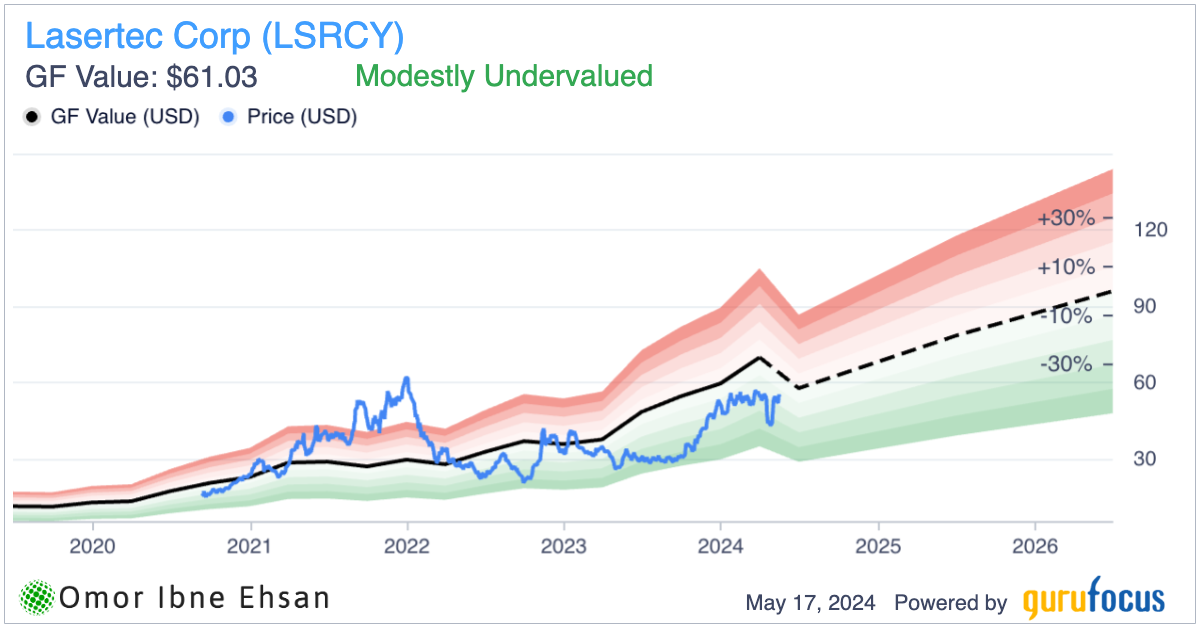

Lasertec (LSRCY)

Lasertec Corporation’s (OTCMKTS:LSRCY) has seen positive momentum in the past year, but it has recently stalled. However, the company holds a big market share in semiconductor inspection and measurement.

Click to Enlarge

In Q1, the company reported a staggering 180% YOY increase in sales of products related to semiconductors, reaching nearly 35 billion Japanese Yen. This surge in revenue was complemented by a 53% increase in service sales.

Further, new orders totaled an impressive 76.3 billion Japanese Yen, with a record 14 billion Japanese Yen in service orders. Also, the stock comes with a small 0.47% dividend yield.

However, I am worried about currency devaluation eating into these metrics. Lasertec’s ADR has underperformed its regular stock on the Japanese stock exchange and could decline if the Yen tumbles more. But, if we see rate cuts soon, the Yen should bounce back. Japan’s ultra-low rates make the currency unattractive for now, but I don’t think the Yen will decline forever.

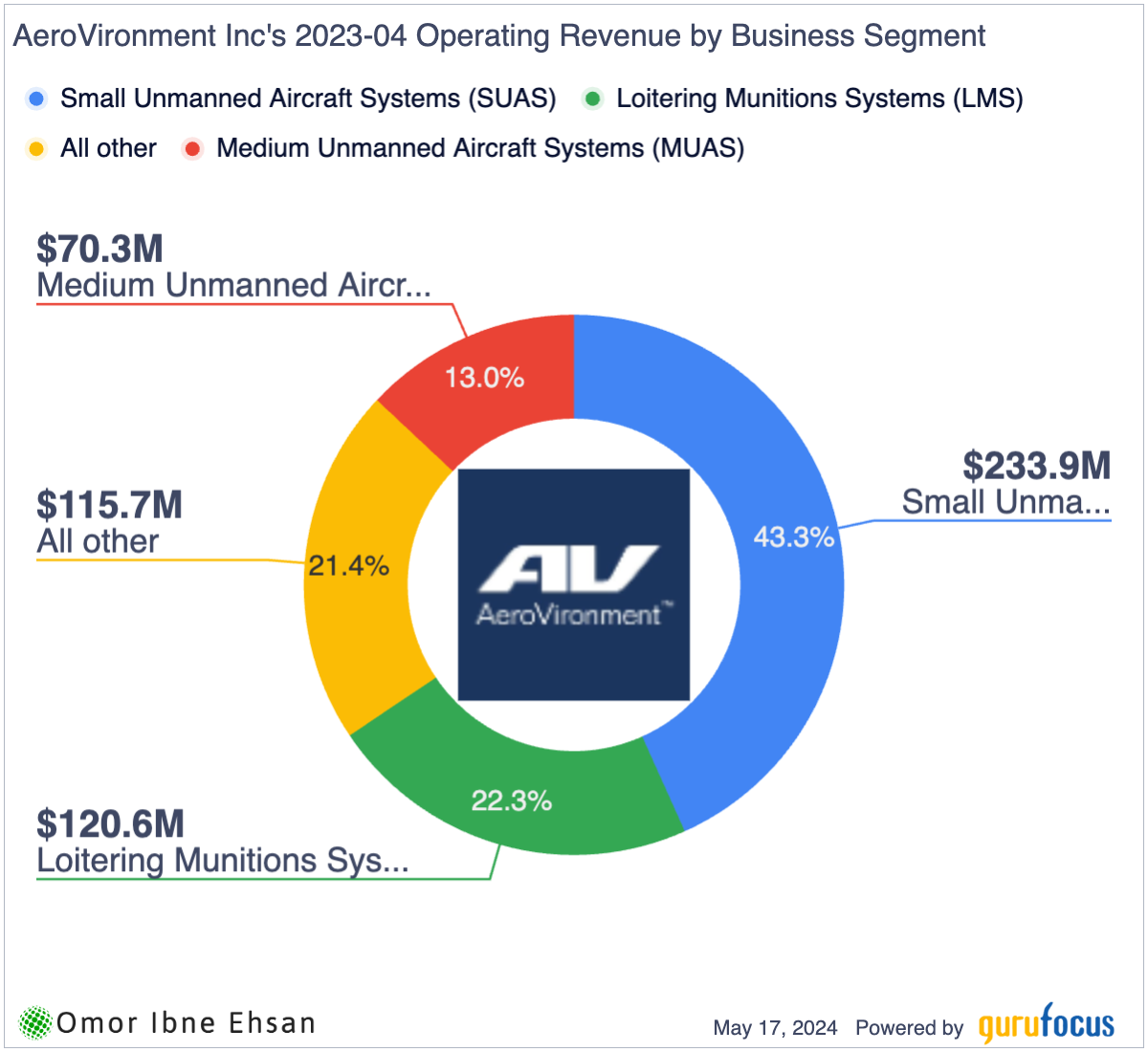

AeroVironment (AVAV)

AeroVironment (NASDAQ:AVAV) is a drone company and a major defense contractor. These drones are becoming more and more critical, and the market is obviously bullish as the U.S. seeks to mass-produce drones in the coming years.

Click to Enlarge

AVAV’s results for the most recent quarter were quite impressive, with revenue up 39% YOY, reaching almost $187 million. This beat sales estimates by a massive 8.4%. EPS also beat by 83.1%. The top performer was their Loitering Munition segment, more than doubling revenue YOY due to the order surge for Switchblade drones. Over 20 countries express interest, and a potentially huge new contract from the U.S. on the horizon.

However, investors will want to monitor AeroVironment’s ability to expand their production capacity for these increasingly large programs. One such program is the Marine Corps Organic Precision Fires initiative, which is being measured in the billions. If AVAV can scale up manufacturing capabilities while maintaining efficiency, their robust 12% YOY growth in pending orders could further accelerate. Management confidently projects double-digit revenue growth through fiscal year 2025. AVAV may still be undervalued despite its recent performance.

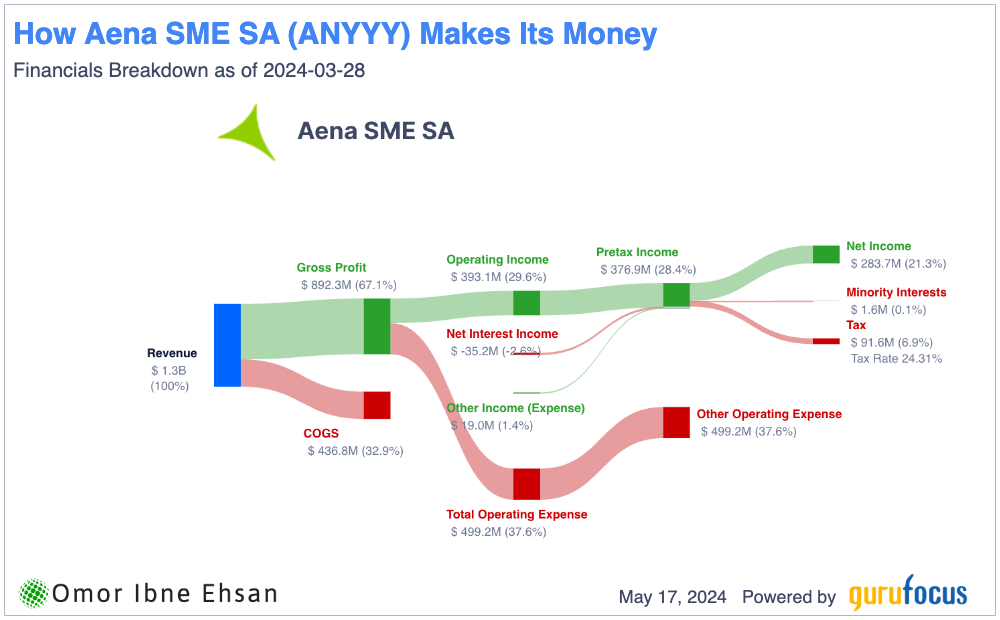

Aena SME (ANYYY)

Aena SME(OTCMKTS:ANYYY) operates two of the top 10 major airports in the European Union. This company is the world’s largest airport operator by passenger volume. Its Q1 passenger traffic soared 11.9% YOY, with traffic at the company’s airports recovering to 115.2% of 2019 levels. This substantial increase in demand resulted in a 20.1% jump in revenue to €1.2 billion YOY. But, it’s quite a bit lower converted to dollars due to the Euro’s devaluation.

Regardless, management reiterated their forecast for full-year traffic implying 7.1% growth. At the same time, ANYYY’s expansion into Brazil through acquisitions opens up another avenue for increasing business. The company has sturdy margins as well.

Click to Enlarge

The approved dividend of €7.66 per share also puts the forward dividend yield at a solid 4.23%. With travel demand still strong so far, Aena SME’s future looks promising.

GigaCloud (GCT)

GigaCloud Technology (NASDAQ:GCT) is not a cloud company by any means. However, I’m not complaining about the misleading name, considering this end-to-end B2B e-commerce company has delivered stellar gains of 177% since I first featured it in an article back in Dec. 2023. It specializes in big items like furniture. It has good upside potential still.

Click to Enlarge

Its revenue is up 96.5% YOY in Q1, and that beat estimates by 3.3%, along with EPS rising 69.2%, which also beat estimates by 64.7%. Their new “Branding-as-a-Service” approach seems promising. It allows sellers to benefit from well-known brand names and stand out amongst lots of competition in crowded markets. The acquisitions of Noble House and Wondersign appear to come at a good time, as GigaCloud diversifies what it offers customers while integrating these new businesses into its operations.

However, management’s rosy outlook seems overly optimistic compared to recent softening consumer spending trends. An 8% decrease in furniture sales across the U.S. is concerning for future demand. Yet, GigaCloud’s online presence should insulate them from headwinds.

Investors pay just 12 times forward earnings. And analysts expect EPS to rise from $3 to $4.5 in the next two years. They also anticipate revenue rising from $1.1 billion to $1.6 billion in the same timeframe.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.