The InvestorPlace Digest aims to provide you with smart, actionable insights that can make you a smarter and richer investor. When I think of the experts I can depend on for those insights, Eric Fry is on top of the list.

His nearly two-decade track record include numerous “10-bagger” calls. He advised his readers to buy Asian stocks during the depths of its late-90s currency crisis, and to buy Russian stocks during its debt-currency crisis, as well as to buy commodities in the early 2000s, right before their historic rally into 2007. More recently, Eric advised folks to buy stocks in that would benefit from the still emerging electric vehicle boom.

In 2016, he won the Portfolios with Purpose competition — Wall Street’s most prestigious investment competition — beating 650 of the biggest names in finance with a 12-month return of 150%.

And his record on the short side of the market is just as impressive. He successfully shorted numerous technology stocks in 2000 and 2001, as those stocks sputtered toward bankruptcy. And, he famously predicted in 2005 and 2006 that the housing boom would go bust and drive government mortgage firms Fannie Mae and Freddie Mac into bankruptcy.

His InvestorPlace service, The Speculator, aims to provide subscribers with the research and actionable insights that are usually reserved for institutional clients. Wall Street depends on experts like Eric to make gains for private hedge funds and big banks.

And Eric brings that level of expertise to his readers.

With his permission, I’m re-running one of his latest articles to his subscribers. It demonstrates the kind of intelligent and perceptive insights his readers get every week in The Speculator.

I know you’ll enjoy it.

To a richer life…

Luis Hernandez, Managing Editor

and the research team at InvestorPlace.com

The Speculator Trade Alert: Buy POST Put Options

By Eric Fry,

Editor, The Speculator

Charlie Munger, the longtime investment partner of Warren Buffett, coined the following truism about troubled companies: “The liabilities are always 100% good. It’s the assets you have to worry about.”

In other words, it’s easy for companies to pile up debt in the pursuit of growth, but difficult to achieve the level of growth necessary to service the debt.

Successful companies clear that hurdle; troubled companies do not. Their assets fail to perform as well as hoped, while their liabilities keep hanging around.

Debt must be serviced, no matter how poorly a company is performing. The liabilities are always “100% good.”

This inconvenient fact has been the Achilles heel of capitalistic enterprises throughout history. Many “successful” companies fail because they do not throw off as much cash as their debt loads require.

Post Holdings (NYSE: POST) is a successful company. But it is a successful company that has piled up a very large amount of debt in order to “buy growth.”

You probably know Post from the breakfast cereals they make – famous names like Raisin Bran, Grape Nuts and Honey Bunches of Oats.

The company has made more than a dozen acquisitions over the last six years – each one designed to deliver a fresh jolt of growth to Post’s sluggish legacy business of selling breakfast cereal.

The company’s press releases continuously tout the success of this strategy. But the numbers tell a different story.

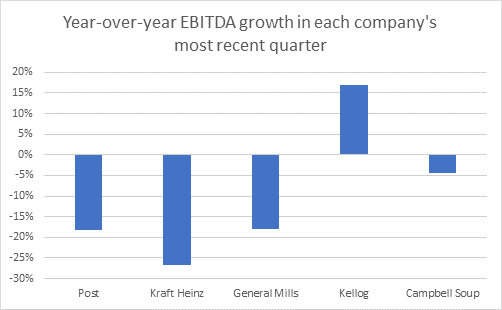

In the chart below you can see Post’s year over year EBITDA growth versus other packaged food companies.

I’m not talking about the headline numbers like earnings per share. Those look fairly pretty. I’m talking about Post’s relatively ugly return on invested capital, relative to its cost of obtaining that capital.

This financial metric has a name. It’s called Return on Invested Capital/Weighted Average Cost of Capital. Or ROIC/WACC.

Whenever this calculation produces a number greater than 1, a company is producing a return that is greater than its cost of capital. Conversely, a number below 1 indicates the company is producing a return below its cost of capital.

In other words, if Company X borrows money at 6% and uses that money to earn 9%, its ROIC/WACC is 1.5 (i.e. 9 divided by 6). That’s a good number. On the other hand, if Company X is borrowing at 6% and using that money to earn just 4%, its ROIC/WACC is just 0.75. That’s bad.

Post’s most recent ROIC/WACC was about 0.87. And that number has been declining for four straight quarters.

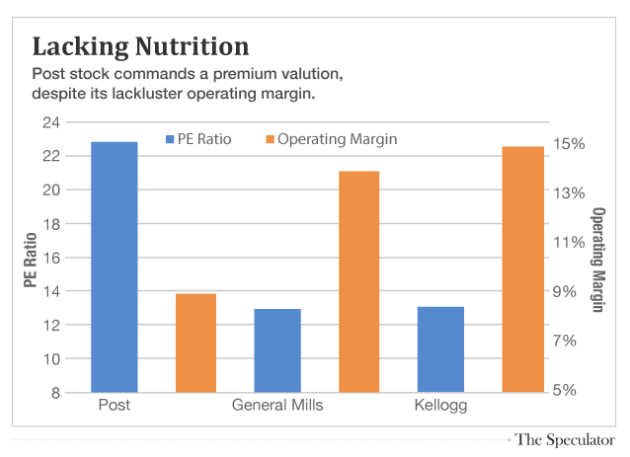

Despite this inconvenient truth, Post shares command a lavish valuation of 23 times earnings, which is nearly double the valuation of its closest rival, Kellogg (NYSE: K). Inexplicably, Post shares hold their lofty PE ratio, despite the fact that the company’s operating margin trails far behind those of both General Mills (NYSE: GIS) and Kellogg.

Perhaps Post’s rich valuation has more to do with Wall Street’s affection for the stock than with the company’s so-so operating results. Eight out of 10 Wall Street analysts rate Post a “buy.” On average, these analysts are expecting the stock to deliver a return of more than 16% over the next 12 months.

I disagree with that upbeat assessment.

Post’s poor return on invested capital (ROIC) is just one of the reasons I expect its stock price to head lower. The company’s massive debt load is another reason.

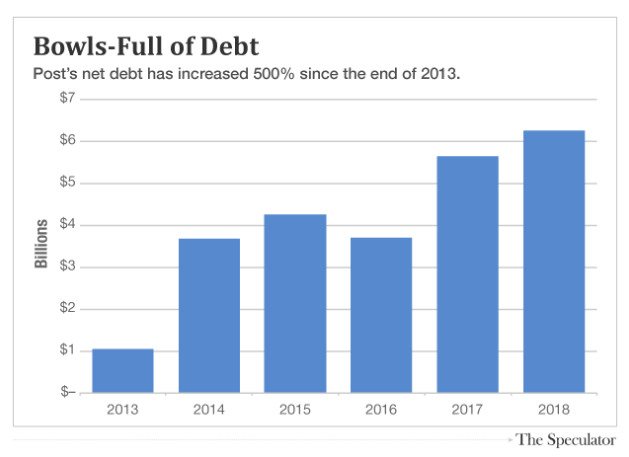

Post’s balance sheet has paid a heavy price for the company’s growth-by-acquisition strategy.

Net debt has soared from $1 billion five years ago to more than $6 billion today.

It is no mystery why Post has been piling up debt to make acquisitions. Its legacy cereal business has become as stale as a forgotten bowl of Grape Nuts Flakes.

Since 2009, cereal sales in the U.S. have tumbled 17%, according to research firm IBISWorld.

This secular decline reflects the changing tastes of American consumers. Today’s breakfast-eaters are much more likely to fill their bowls with Acai and yogurt than with Post Fruity Pebbles.

Recognizing this long-term trend, Post embarked on its strategy to diversify away from its cereal business. And the company has certainly achieved that objective.

Before Post started its acquisition binge five years ago, the company’s cereal division (now known as its Consumer Brands division) accounted for 96% of total sales. Today, that division accounts for just 29% of sales.

But diversification does not guarantee earnings growth.

If Post had been able to acquire its new businesses on the cheap and/or fund its purchases with internally generated cash, the acquisitions could have achieved a very high return for shareholders. But that’s not what Post has done.

Instead, the company has paid close to top-dollar for the companies it has acquired.

To seal the deal on one of its most recent acquisitions, Post paid more than 14 times EBITDA (i.e. gross earnings), which represents a steep 38% premium to the current valuation of the S&P 400 Packaged Foods Index.

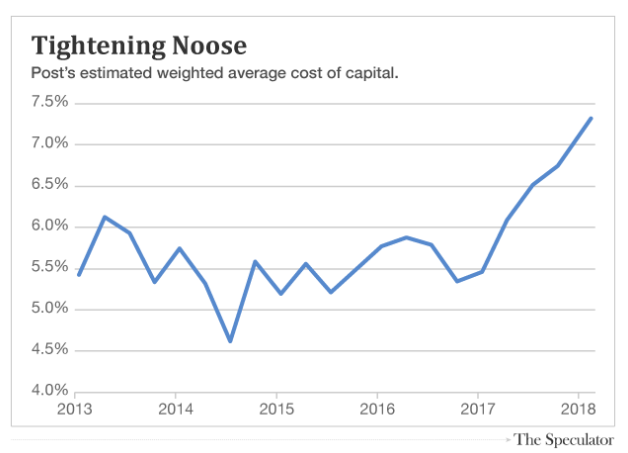

Making Post’s acquisitions even more challenging is the fact that its credit rating is solidly in the “junk” category. Its “B+” rating on long-term debt from Standard & Poor’s is a distant four notches below “investment grade.”

As a junk-rated credit, Post must pay a higher interest rate on its borrowings than would a company with a better credit rating. And to make matters worse, interest rates have been on the rise for the last several months, especially for junk-rated credits like Post.

According to Bloomberg data, Post’s cost of capital has soared from about to 5% to 7.3% during the last 12 months.

But the company’s ROIC is only 6.4%, which takes us back to the troublesome data point I mentioned above:

Post’s ROIC/WACC is just 0.87, which means its return on capital is less than its cost of capital.

That isn’t good.

If you borrow money at 7.33%, then invest it at 6.40%, you’re losing money…no matter what your income statements might say.

So I now recommend betting against the stock by selling it short (or buying put options on it).

Cosmetically, Post’s reported earnings look decent. But below the surface, its operational results reveal a company that is struggling to overcome the no-growth trends of the packaged foods industry.

Good investing,

Eric Fry, Editor

The Speculator