The Federal Reserve’s next Federal Open Market Committee (FOMC) meeting and key interest rate decision aren’t until the end of July, but that hasn’t stopped the rumor mill from buzzing about what our central bank will do next.

The reality is that there are a lot of factors that the Fed needs to consider – and everyone has an opinion on how the Fed should respond to these factors.

As I shared last week, in my opinion, it would be very unwise for the Fed to raise key interest rates at its July meeting.

The latest FOMC minutes showed that there’s some dissension among committee members. The minutes revealed, “Some participants indicated that they favored raising the target range for the Federal Funds rate 25 basis points at this meeting or that they could have supported such a proposal.”

The key word is “some,” which is not indicative of a majority. Interestingly, Fed Chairman Jerome Powell recently commented, “A strong majority of committee participants expect that it will be appropriate to raise interest rates two or more times by the end of the year.” So, the FOMC minutes say “some” and Powell says “strong majority.”

Frankly, since there is an outspoken minority of doves on the Fed from Atlanta, Chicago, Minneapolis and San Francisco, I think the July FOMC meeting will rest on the June inflation reports, especially the Consumer Price Index (CPI).

In today’s Market 360, I’m going to review the June inflation reports released this week – the CPI and Producer Price Index (PPI). And I’ll share how you can prepare your portfolio for what the Fed does next…

Let’s jump right in.

Consumer Price Index (CPI)

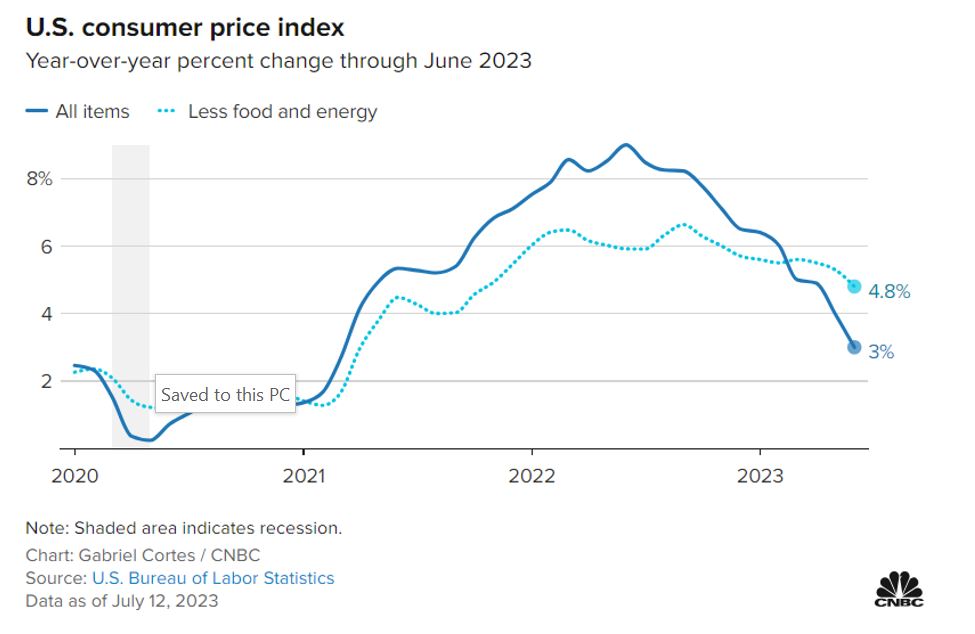

Yesterday, the Bureau of Labor Statistics released the June CPI numbers.

CPI for June rose just 0.2%, up 3% year over year. This is slightly lower than the 3.1% expected – and the lowest number we’ve seen since March 2021.

The core CPI – which excludes food and energy – also rose 0.2% for the month and 4.8% in the past 12 months. That compares to a 0.3% monthly increase and a 5% annual rise expected. This puts the annual pace at the lowest it’s been since October 2021.

Overall, this is great news.

As we dig a little deeper into the numbers, small gains in food prices and a decline in used vehicle and airline prices contributed to the lower number.

However, shelter costs – which account for one-third of the CPI – continued to climb higher. The shelter index rose 0.4% in June, up 7.8% on an annual basis. According to the Bureau of Labor Statistics, the monthly gain accounted for about 70% of the increase in headline CPI.

Chief economist at Bright MLS, Lisa Sturtevant said:

Housing costs, which account for a large share of the inflation picture, are not coming down meaningfully. Because rates had been pushed so low by the Fed during the pandemic and then increased so quickly, the Federal Reserve’s rate increases not only reduced housing demand — as intended — but also severely limited supply by locking homeowners into homes they would have otherwise listed for sale.

Markets rallied yesterday on the news – with the S&P 500 closing up 0.74%, the Dow and NASDAQ closed 0.25%, and 1.15% higher, respectively. Both the S&P 500 and NASDAQ closed at their highest levels since April 2022.

Producer Price Index (PPI)

This morning, the Bureau of Labor Statistics released the PPI numbers for June.

June’s PPI rose 0.1%, compared to the expected 0.2%. Year-over-year, the PPI rose 0.1%. This is the lowest annual pace in almost three years.

The core PPI – which excludes food, energy and trade – rose 0.1% and is up to 2.6% in the past 12 months.

But what’s important is that wholesale service prices rose only 0.1% in June after running a lot hotter in previous months.

What the numbers are telling us is wholesale service inflation has essentially fizzled.

But there was another interesting part of the PPI report…

The report showed that wholesale goods have declined 4.4% in the past 12 months. This means there’s deflation on the wholesale level.

The result is, there is no longer any inflation on the wholesale level.

The Fed’s Next Move…

With inflation cooling on both the consumer and wholesale levels, I don’t expect the Federal Reserve to raise key interest rates at the July FOMC meeting.

The fact is that the CPI surged 1.2% in June 2022, and that number is effectively cut off now. Hopefully, the doves will be more outspoken and convince the rest of the FOMC to pause again in July.

The one glitch that could persuade members to raise rates? The labor market.

Last week, the ADP reported that 497,000 payroll jobs were created in June. That was the largest monthly gain since February 2022, and it crushed expectations for 220,000 jobs.

ADP also reported that wages rose at a 6.4% annual pace in June for workers who did not change jobs. For those workers that changed jobs, wages rose at an annual pace of 11.2%. Believe it or not, this was the slowest pace in wage growth since 2021 and might help convince the Fed that wages are cooling.

The big surprise, though, was the Labor Department reporting that only 209,000 payroll jobs were created in June. The April and May payroll reports were also revised lower, and the unemployment rate slipped to 3.6%. The ADP and Labor Department also reported a 211,000 difference (232,000 versus 21,000) in leisure and hospitality employees in June.

Confused? We all are.

At the end of the day, the Fed pays attention to the market rates. The 10-year Treasury yield was well over 4% last Thursday, a week ago today. Today we’re at about 3.82% – though it cracked 3.8% earlier today. The two-year Treasury yield, which was about 5.08% a week ago, is now at about 4.66%. These are dramatic declines in Treasury yields.

And when Treasury yields fall, it takes the pressure off the Fed. In other words, Treasury yields coming down this week is good news.

Bottom line: The Fed has a lot to think about ahead of its July FOMC meeting.

In the meantime, it’s imperative we stay invested in

fundamentally superior stocks with great earnings, especially with the second-quarter earnings season officially kicking off tomorrow with the Big Banks.

Personally, I expect a lot of great reports from my Breakthrough Stocks companies. My average Breakthrough Stocks is forecasted to post 85.4% annual earnings growth in the upcoming weeks. And since my stocks are characterized by positive analyst earnings revisions, I am expecting strong earnings surprises.

To further “lock and load” my Breakthrough Stocks Buy List for this earnings season, I am adding one more stock in tomorrow’s Breakthrough Stocks Monthly Issue for July.

Join me at Breakthrough Stocks today and make sure you’re on the list to get tomorrow’s new buy.

Sincerely,

Louis Navellier