Airlines, cruise stocks and other beaten-down assets are surging back to life. That’s as investors pile into these equities on optimism over the U.S. reopening. But let’s not forget about Visa (NYSE:V), a high-quality play that should benefit too. V stock is up almost 50% from the lows, but could it have more to go?

I like Visa for a couple of reasons, but here’s the main one: It can function with an open or closed economy.

Obviously a prolonged recession doesn’t do credit card companies any good. That will lead to a selloff in Visa, but also in MasterCard (NYSE:MA), Discover (NYSE:DFS) and American Express (NYSE:AXP). For now though, we’re not looking at a prolonged shutdown, which bodes well for the group.

Reopening America

A number of stocks — from Carnival Cruise (NYSE:CCL) to Delta Air Lines (NYSE:DAL) — have been hammered. That’s as much of the U.S. and many parts of the world entered multi-week and multi-month lockdowns. That’s a clear detriment to their business model. For Visa though, there’s at least a silver lining. The company benefits from online sales too.

So as consumers sign up for Netflix (NASDAQ:NFLX) and shop on Amazon (NASDAQ:AMZN), those credit card sales are ringing up. Further,

Costco (NASDAQ:COST), Target (NYSE:TGT), Walmart (NYSE:WMT) and other big-box retailers had a strong quarter as the public stocked up on goods.

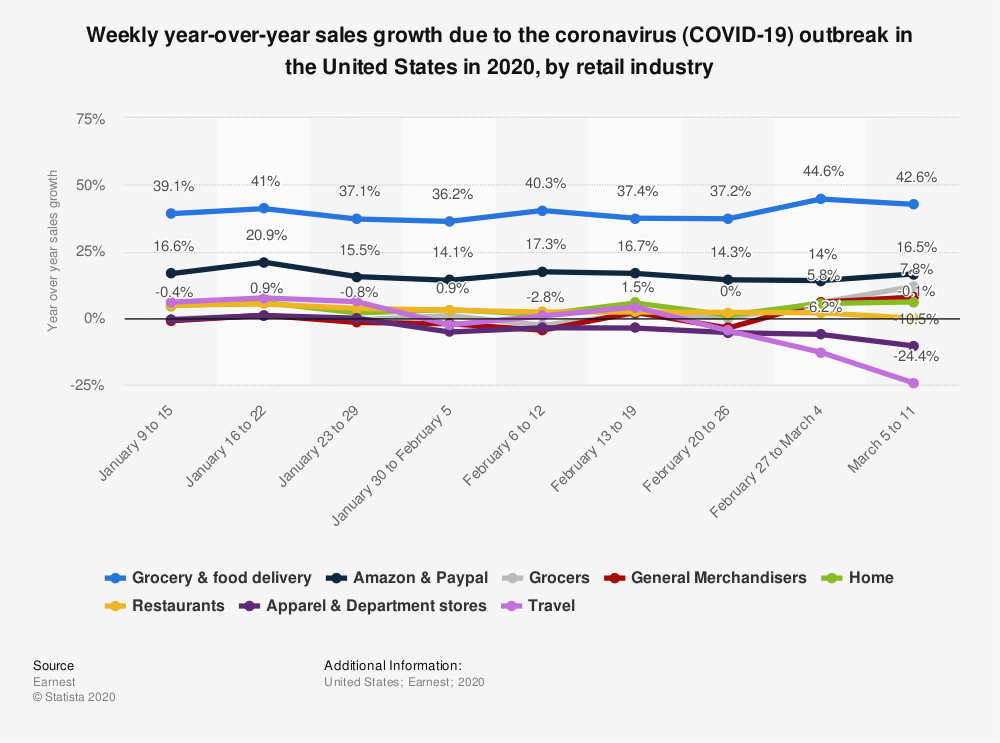

Click to Enlarge

Is this enough to offset all of the lost sales over the past few months? No, not completely. But it helps quite a bit. Combine that with the country beginning the reopening process — and seeing fast action by the public — and it’s no wonder V stock is in demand.

Taking V Stock a Step Further

The country is reopening and that’s an obvious boon for credit card companies. But let’s not forget, Visa has cemented itself in a long-term secular trend. As we digitize our wallets — shifting to more online sales, using cryptocurrency, etc. — this is only going to benefit Visa and others.

However, Visa also benefits from a secular shift from cash and check to credit and debit. This trend has been in play long before the novel coronavirus came along and will remain in trend long after it’s gone.

Further, Covid-19 will likely accelerate tap-to-pay, touchless pay, money sharing and other technologies that don’t rely on physical money handling. Put simply, Visa has a hand in all the different future versions of payment — different formats of which continue to pop up.

PayPal (NASDAQ:PYPL) CEO Dan Shulman says digital payment trends are accelerating at a rapid pace. One recap of his comments stated that, “e-commerce and digital payment trends in three months have gone where it previously may have taken three-to-five years to achieve.”

Why does that matter? Because it will continue to fuel top- and bottom-line growth for companies like Visa.

Valuing Visa

For now, current estimates call for revenue to fall 4% in 2020 to approximately $22 billion. On the earnings front, estimates call for a 7% decline this year. If we could see break-even results this year, it would bode well for investors and V stock. Particularly as this is a core holding in many portfolios.

While Visa does have roughly $17.8 billion in total debt, remember, this is a $425 billion market cap company. That’s a small sum for a company of this size. Further, total assets of $72.8 billion are almost double total liabilities at $38.2 billion.

There’s just one other point I want to make. We often praise Facebook (NASDAQ:FB) for its margins and profitability. The company sports trailing gross margins 81.72% vs. Visa at 81.55%. However, when it comes to net profitability, Visa dominates. Its net margins are all the way up at 52.26% compared to Facebook at “just” 28.57%.

Combine that with an economic reopening and it’s no wonder V stock is rallying.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.