Everyone loves to buy low and sell high, right? That doesn’t necessarily mean we have to buy penny stocks to do it. After all, if we buy a $100 stock and it goes to $500, that was a buy-low, sell-high move that I would’ve liked to be in on. But we don’t have to overlook cheap stocks to get big moves either.

Keep in mind, the following names are trading in the single-digit range for a reason. Something is wrong or was wrong, but brighter days could be ahead.

Need proof?

Advanced Micro Devices (NASDAQ:AMD) was trading for less than $2 per share in early 2016. Some 30 months later it’s almost at $20. In 2011, Bank of America (NYSE:BAC) was trading for about $5. It’s taken a while, but seven years later and its over $30 a share. Noodles & Co (NASDAQ:NDLS) has a 52-week low of $3.50 and is now trading at $10.

These are just a few names that have made the turn. So who could be next? For our setup, we wanted some high-quality opportunity. We are looking at cheap stocks trading in the U.S., with a $5-handle or lower and have a market cap above $300 million. We also wanted named with expectations of positive earnings growth this year and next year.

So here’s what we’ve got:

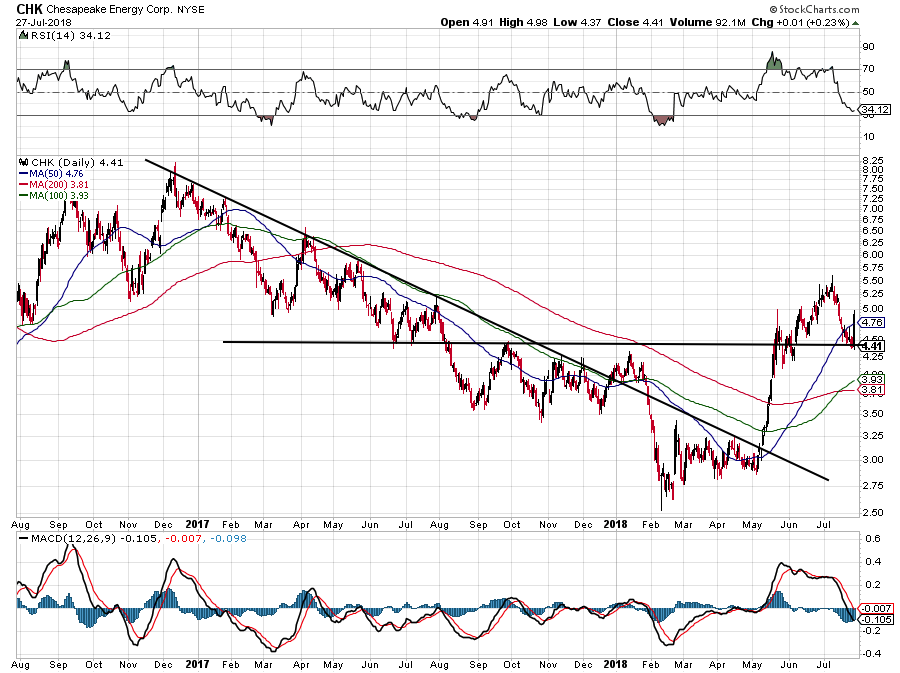

Cheap Stocks to Buy: Chesapeake Energy (CHK)

Click to Enlarge

On Friday, Chesapeake Energy (NYSE:CHK) shares rocketed higher after announcing it would sell assets in the Utica shale for $2 billion. For a $4 billion market cap company, that’s no small deal, although shares have since given back most of their gains.

CHK management says the deal should improve EBITDA and lower gathering, processing and transport costs by more than $400 million. Further, as energy prices continue to climb, CHK should continue to benefit going forward.

On the charts, CHK held exactly where it needed to. Below this $4.25 to $4.50 area and bulls will have larger concerns. Above though and the recent highs near $5.50 are in target.

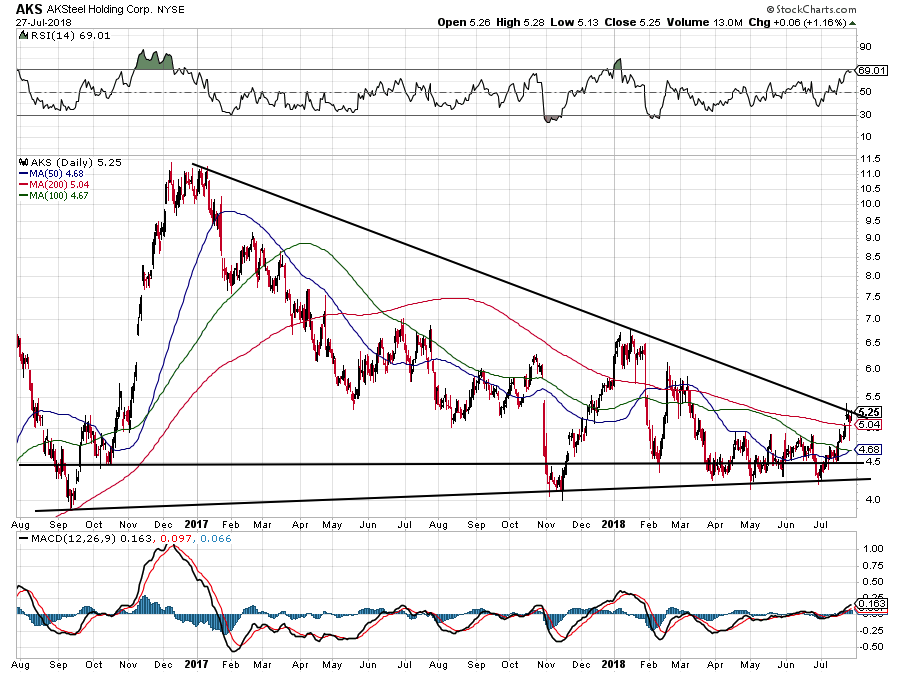

Cheap Stocks to Buy: AK Steel (AKS)

Click to Enlarge

The $5 level has been vital for AK Steel (NYSE:AKS) on both the upside and the downside. Share initially dropped below that mark on Thursday before quickly reversing intraday and heading higher. If it can get back above the recent high near $5.40 and AKS stock looks like it could run to $6.

Steel stocks like AKS, Nucor (NYSE:NUE) and U.S. Steel (NYSE:X) have been volatile. The global trade war and frequent changes in tariffs (and presidential tweets) have created an unstable operating environment for investors. That added uncertainty adds to the volatility, although there is optimism that these issues will be worked out this year.

The fear is that, if there are cutbacks in steel consumption — like with orders from the automakers such as Ford Motor (NYSE:F) and General Motors (NYSE:GM) — then business will suffer. But so long as we remain in a healthy economic environment, steel stocks should continue to do well.

For the record, the U.S. economy just printed a 4.1% GDP report for the second quarter and revised the first quarter from 2% to 2.2%. So things are going well and steel should be one of the beneficiaries.

AK Steel fell below $5 when it reported earnings this week. It missed on revenues due to a power outage caused by a lightening strike, which is by definition an event unlikely to happen twice.

Cheap Stocks to Buy: Zynga (ZNGA)

Click to Enlarge

Why should investors consider buying Zynga (NASDAQ:ZNGA) stock now? Trading at about $4, there is seemingly not much to love about the name.

With its $3.5 billion market cap, Zynga is far from huge. When going off its trailing earnings valuation, ZNGA is not that attractive either. However, take a closer look. For instance, the company has more than $635 million in cash and short-term investments and no debt.

Currently, analysts expect Zynga to grow sales more than 14.4% this year and another 13.4% in 2019. On the earnings front, estimates call for 66% growth this year to 15 cents per share and another 33% in 2019. That prices ZNGA stock at about 26 times this year’s earnings.

Previously, we mentioned its trailing valuation — which is about 80 times the last 12 months of earnings — was expensive, and it is. But on the surace, 26 times for this year’s earnings isn’t too bad for such good growth. No one will argue that Zynga is a blue-chip stock, but double-digit revenue growth and no debt only makes it more attractive.

If Zynga can keep costs down and boost its margins, it will become even more attractive. Should legalized gambling continue to take more progressive steps, Zynga is sure to benefit and could be an M&A target down the road.

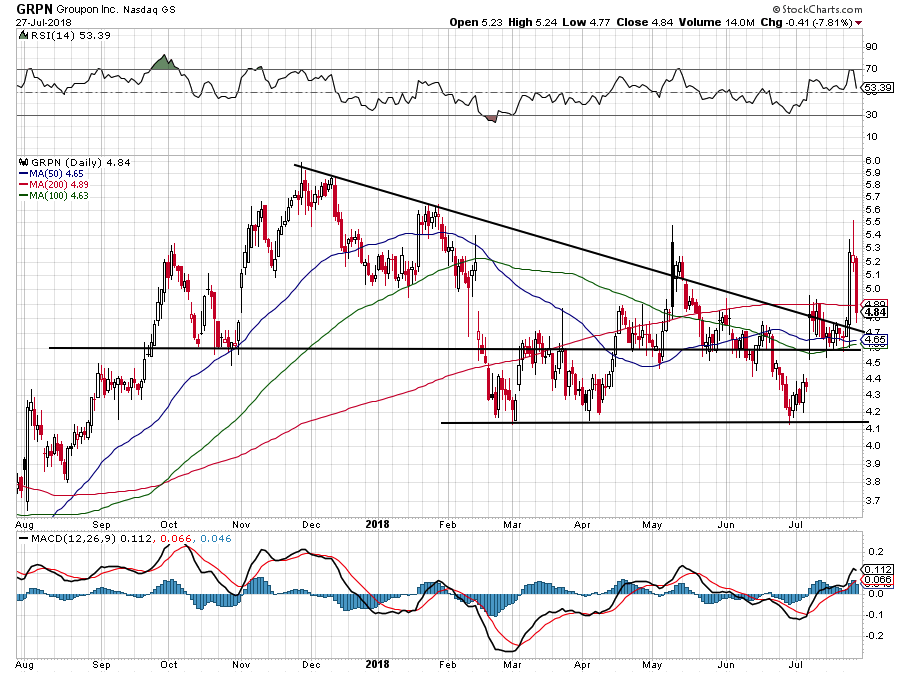

Cheap Stocks to Buy: Groupon (GRPN)

Click to Enlarge

On Friday, shares of Groupon (NASDAQ:GRPN) tumbled almost 8% after the company lost a patent dispute with IBM (NYSE:IBM). The move thrust GRPN back below $5. Is it time to buy?

Unlike Zynga, Groupon does have a small amount of debt with $192 million on the books. But with $725 million in cash, GRPN has more than enough in the bank.

The company is in improvement mode, as it sheds revenue growth in lieu of profits. While on a GAAP basis Groupon is not yet profitable, the company is quite near break-even operation.

As the company boosts its gross margins despite the decline in revenue, operating margins are climbing as well. On a non-GAAP basis, analysts expect earnings of 24 cents per share, more than double the 11 cents per share it generated last year. That prices Groupon at about 18 times this year’s earnings, which are forecast to grow another 12.5% next year.

Next year is also when analysts expect Groupon to generate positive revenue growth vs. the 6.7% decline this year. All in all, Groupon isn’t perfect. But it doesn’t have a bloated balance sheet, is improving its profitability and should see a lift in revenue next year. If it’s able to maintain or build on its recent margin improvement, the boost in sales should help GRPN’s bottom line meaningfully.

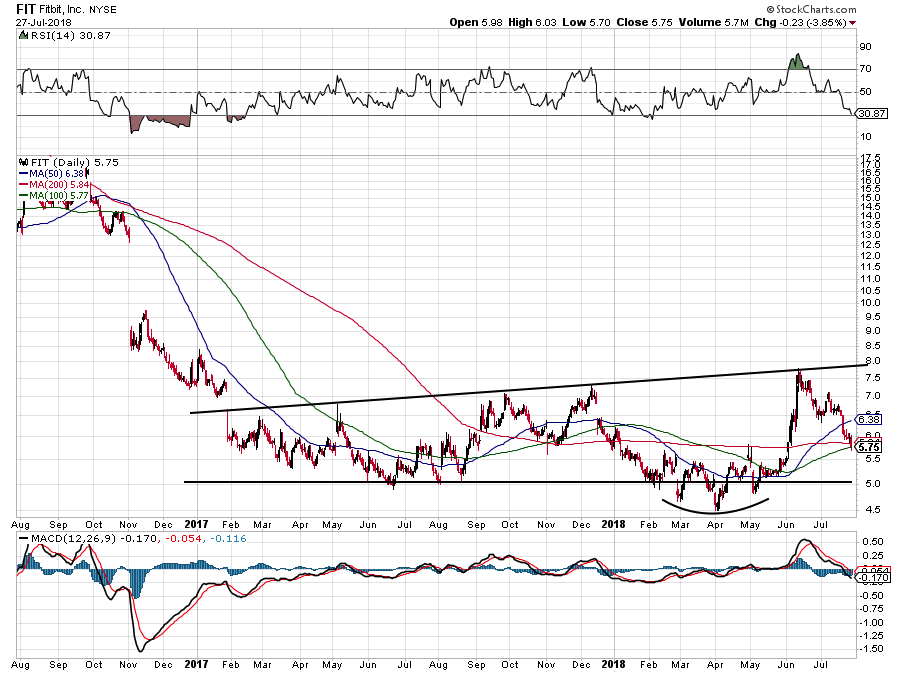

Cheap Stocks to Buy: Fitbit (FIT)

Click to Enlarge

Fitbit (NYSE:FIT) is not necessarily below $5, but with a $5-handle we considered close enough.

Is the company starting to bottom? It’s been a prolonged process, but possibly. While Apple (NASDAQ:AAPL) has become the predominant player in wearables with its Apple Watch, Fitbit isn’t non-existent. And while it makes high-end versions too, someone needs to dominate the lower end of the wearables market, right?

As wearables continue to gain traction in popularity, Fitbit can be the one to answer the call. Plus, as companies and insurance providers start to take health and health costs more seriously, some — like Target (NYSE:TGT) — are beginning to provide products like a Fitbit to its employees as a means of improving health and costs.

For FIT’s part, the company sports a $1.4 billion market cap, has $658 million in cash and short-term investments and zero debt. If and when management gets this ship turned around, shares can fly as a result.

Estimates call for an 8.7% decline in sales this year, but a 1.7% bump in 2019. While not great, it’s good to know that next year’s sales should be done declining. While not yet profitable, Fitbit also boast improving margins, suggesting the company is trending toward that goal in the future.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell was long BAC, AAPL and GM.