What trader sentiment is telling us … so much bearishness might fuel a monster bull … did it start yesterday?

Yesterday saw the markets explode higher, with the beaten-down Nasdaq leading the way, up 3.5%.

As I write Friday afternoon, we’re back to losses. All three major indexes are down, with the Nasdaq’s 3.5% decline leading the way.

Much of the blame is falling on Amazon’s poor earnings from yesterday after the bell.

So, what was yesterday then? Just a brief, bullish blip within a broader sea of selling? Or was it a precursor to more sustained bullishness, despite today’s losses?

Well, we don’t have a crystal ball. But let’s start answering by looking at sentiment.

***Many times, when a majority of investors all feel the same way about a particular market move or upcoming direction, the opposite happens

You often see this at the end of a bull market. When everyone is bullish, everyone has put their money into the market. But this means there are no more investable dollars left to continue pushing prices higher. And so, despite the bullish sentiment, prices drop.

This dynamic often plays out in reverse as well. When all the bearish sellers have left the market, there’s no one left to keep pushing prices lower. So, any whiff of good news can send prices screaming higher.

There’s an old idea on Wall Street that the market tends to do whatever surprises and hurts the most investors.

Well, coming into yesterday, investor sentiment had grown so negative that the gains were overdue.

Let’s look at a handful of examples of this negativity, beginning with something our technical experts John Jagerson and Wade Hansen of Strategic Trader wrote about in their Wednesday update.

Here they are to introduce the concept:

Traders (you included) can borrow up to 50% of the purchase price of a stock – according to Regulation T of the Federal Reserve Board. That means if a stock costs $100, you are only required to put up $50 of your own money to purchase the stock. You can borrow the other $50.

Traders borrow money for their trades to increase their leverage, or potential for return, in the trade.

If you use 100% of your own money to buy a stock and the stock increases in value by 10%, you make a 10% return on your money.

But if you only use 50% of your own money and then borrow the other 50% to buy a stock, you make a 20% return on your money if the stock increases in value by 10%.

You essentially double your potential return when you borrow half of the purchase price.

John and Wade point out that leverage obviously works both ways.

For example, say you only use 50% of your own money in a trade and then borrow the other 50%. If your investment drops 10%, you suffer a 20% loss on your money. You double your potential losses.

Here’s the logical takeaway from John and Wade:

Confident traders tend to increase the leverage in their trades by borrowing more. They want to generate larger returns.

Nervous traders tend to decrease the leverage in their trades by borrowing less. They want to protect their capital.

In light of this, we can track this leverage, or “margin debt,” to see how traders are feeling, which can have an outsized impact on market direction.

***What are margin debt levels telling us about how traders have been feeling?

Back to John and Wade:

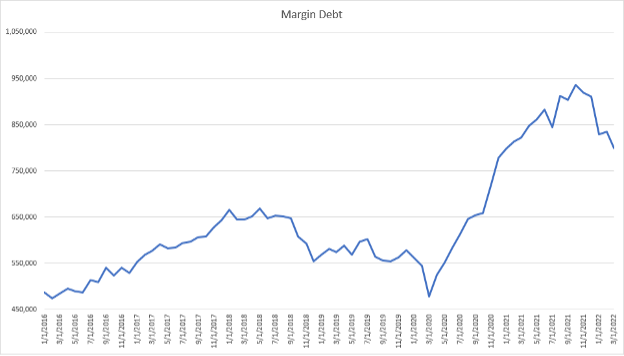

For the past two years, traders have shown extreme confidence in the U.S. stock market by increasing margin debt to new highs.

That all started to change in late 2021. According to the latest numbers from FINRA, as of Mar. 22, Wall Street has cut its borrowing to only $799.7 billion to buy stocks (see Fig. 5).

It may sound strange to say “only” $799.7 billion, but as you can see in Fig. 1, this is down nearly 15% from the high of $935.9 billion Wall Street had borrowed as of Oct. 21, 2021.

We don’t have any numbers for April yet, but it appears confidence is still falling.

We wouldn’t be surprised to see margin debt continue to drop as traders work to reduce risk and protect the capital in their portfolios by de-leveraging their positions.

So, we’ve had traders feeling increasingly bearish.

What about individual investors?

***Where mom ‘n pop traders think the market will be six months from now

Coming into yesterday, retail traders weren’t feeling particularly bullish either.

We can see this by monitoring research from the American Association of Individual Investors (AAII).

From its reading (4/27), only 16.4% of AAII members felt bullish about where the market will be in six months. A whopping 59.4% were bearish, with the remainder neutral.

For some context, this was the most bearish that investors have been in the last 12 months. It’s also double the average level of bearishness, which comes in at 30.5%.

***For more overly bearish sentiment, we could look to the recent put-to-call ratio

We won’t dive into all the details but, in general, put options are a bearish bet on the market, while “calls” are a bullish bet. Looking at the ratio of puts to calls tells us which sentiment is in control.

Coming into yesterday, the five-day average put/call ratio stood at 0.94, according to CNN Business, which is interpreted as “Extreme Fear.”

Plus, as we pointed out yesterday, the Relative Strength Index of the S&P had just sunk to nearly oversold conditions.

Bottom line, with so much negativity in the air, it was actually no wonder that we enjoyed a monster relief rally yesterday.

The bigger question is whether it was the seed of a real bullish reversal, or just a head-fake within a larger, bearish decline.

***What to make of yesterday’s bounce

Back on March 25th, the host of the popular investment show Mad Money, Jim Cramer, pronounced “the bear market is over.”

The Nasdaq promptly rewarded his self-assured prediction by falling 12% over the next few weeks. In fact, with today’s sell-off, the Nasdaq remains at 11.5% down since Cramer’s call.

So, let’s approach a market forecast with a bit more humility.

As we noted above, given the extreme volume of negativity coming into yesterday, we were due for a bounce.

And due to today’s continuation of negativity, it wouldn’t be surprising to see more gains over the coming sessions after the market digests the poor Amazon numbers.

But we have to ask, beyond overly negative sentiment, what has really changed?

Yes, overly bearish sentiment can result in a temporary bullish reversal in the market – that’s exactly what we saw back in mid-March.

But for real, sustained gains, we need tailwinds from elsewhere to support a bullish move.

Think of it like trying to pedal a bicycle from a standstill. The tiny cogs will get you going, but they can’t get you going fast. It’s the larger cogs that help you achieve real speed and momentum.

In the case of the market, an emotion-based relief rally is a great start. But it’s the small cog.

For the market to head back to the highs at the turn of the year, we need the big cogs, which means positive news related to earnings, inflation, Fed policy, and the removal of the broader macro-overhangs of Russian aggression and China-related supply chain problems.

***On this note, this morning we learned that the Fed’s favorite inflation gauge, the core personal consumption expenditures price index, rose 5.2% in March

Some analysts are proclaiming this to be a victory, since the reading from February was 5.3%.

Sure, while dropping 0.1% is better than adding 0.1%, the more important point is that inflation is still burning through the economy.

Given this number, it’s likely we’ll see the anticipated 50-basis-point rate hike from the Fed next week. And that’s even with the negative GDP reading from yesterday. (After all, consumer spending posted solid numbers, and that’s what the Fed is watching closely.)

But this 50-basis-point hike is largely priced into the market today. The variable will be Fed Chair Powell’s commentary. Perhaps the poor GDP number will soften things a bit. Maybe the unknowns surrounding Russian aggression will lead to move dovishness.

We don’t know – that’s what we’ll be watching.

Looking elsewhere, if earnings continue to surprise on the upside, it could give us a boost. That said, the market seems to be trending toward paying equal attention to guidance for next quarter. Case in point: Apple, which posted strong earnings yesterday after the bell, but warned of a possible $8 billion hit from supply chains next quarter. Its stock is off about 2.3% as I write.

In good news, so much air has been let out of the market that valuations are appearing far more reasonable today.

I know that I’m not offering a clear prediction of what’s going to happen. And I know that can be frustrating. But there are simply too many shifting variables right now to declare we’re headed up or down. I don’t want to Jim Cramer you.

What we do know is that our first bit of new information that will give us clues about direction will come next Wednesday, when the Fed releases its policy statement.

We’ll be watching closely and will report back here in the Digest.

Have a good evening,

Jeff Remsburg