If you’re reading this article title and thinking I must be delusional to talk about “the mother of all bull markets” in this environment, I don’t blame you one bit.

However, the picks I’ll be discussing today are stocks I believe are well-positioned for the next major market upswing whenever it eventually arrives. Could we still see some upside in the near term, similar to the summer 2023 correction before stocks resumed their march higher? It’s certainly possible if the hype and speculation continue.

But regardless of the short-term gyrations, I’m convinced the seven stocks highlighted below have what it takes to weather the current choppiness and turbulence. These companies have powerful long-term growth trends. I expect these stocks to deliver solid gains when the next sustainable bull market finally kicks into gear.

Berkshire Hathaway (BRK-A, BRK-B)

I’m confident Berkshire Hathaway (NYSE:BRK-A, NYSE:BRK-B) will thrive in the next bull market and for decades to come. As Buffett himself says, “If you aren’t willing to own a stock for 10 years, don’t even think about owning it for 10 minutes.” I believe Berkshire remains one of the best long-term investments you can make. It has a fortress-like balance sheet and nearly $189 billion in cash. This business has the flexibility and stability that’s hard to find elsewhere in the market.

As Morningstar analyst Greggory Warren notes, Berkshire’s unique structure means its “economic moat is more than the sum of its parts.” The company’s insurance operations provide a steady stream of low-cost “float” that can be invested for higher returns.

Recently, the company has been taking profits by trimming its massive stake in Bank of America (NYSE:BAC), selling over $3 billion worth of shares this month alone. BoA isn’t the only stock being sold, though. Buffett has been a net seller for nearly seven quarters in a row. I believe he’ll go contrarian once stocks take a breather, and this should position the firm to do very well in the next bull run.

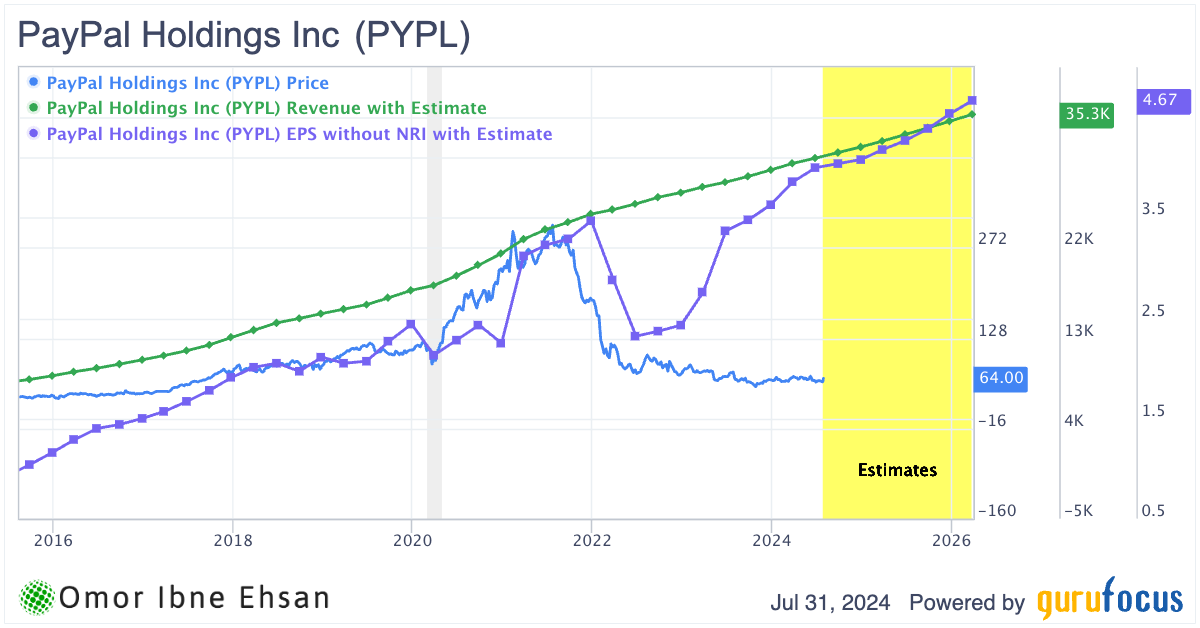

PayPal (PYPL)

PayPal (NASDAQ:PYPL) is a leading digital payment company that enables individuals and businesses to send and receive money online. The stock has been trading sideways for much of the recent bull market rally. But just when many overhyped stocks have started to falter, as of this writing, PayPal has perked up with an 8% gain in the past 24 hours.

It reported Q2 earnings that beat expectations, with revenue growing 8% year-over-year to $7.9 billion. Analysts like Cowen’s Bryan Bergin, who has a “hold” rating, noted the results were better than feared. Also, the company raised its full-year adjusted EPS guidance to $3.88-$3.98.

However, revenue growth is still decelerating, and margins have been under pressure recently. It remains to be seen if this is the start of a sustained uptrend for PayPal stock or just a short-term bounce.

Regardless, PayPal is one of the most compelling long-term buys in the market today. The stock is heavily discounted compared to pre-pandemic levels.

Click to Enlarge

With account growth reaccelerating and strong growth, I believe it’s well-positioned to outperform once market sentiment decisively turns bullish again. The stock would trade at nearly $500 if it traded at its pre-pandemic earnings multiple.

Marsh & McLennan (MMC)

Marsh & McLennan (NYSE:MMC) is a global professional services firm that provides advice and solutions in risk, strategy and people. The company has delivered strong results so far in 2024, with 6% underlying revenue growth and 10% adjusted EPS growth in Q2.

I believe MMC is one of the most consistent stocks available. It has dodged downturns in the past while still delivering significant returns in bull markets. The stock is up a solid 14% over the past year and has avoided the recent tech selloff.

In my view, MMC is a smart buy in the current environment. You likely won’t get burned if the market keeps sliding. But you should reap nice rewards in the next bull run. It’s a very sticky business model.

Moreover, the company continues to invest in talent and capabilities. Some analysts are bullish, noting more insurance premium growth ahead. However, Q2 sales and earnings slightly missed estimates on the bottom line. Yet the impact of that miss on the stock has been negligible.

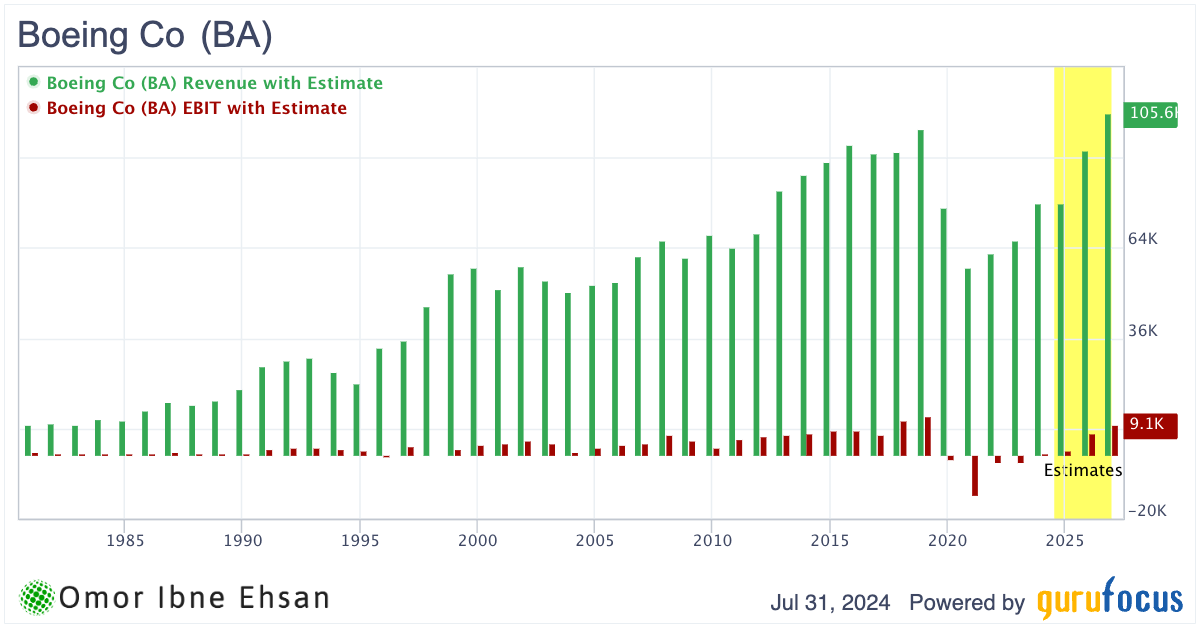

Boeing (BA)

I see potential in Boeing (NYSE:BA) as it is one of only two major passenger aircraft manufacturers globally. Its main competitor is the European company Airbus. Boeing’s strong position in the U.S. market and the government’s vested interest in its success give the company a significant advantage.

Although Boeing is currently facing weakness, I believe the stock offers considerable upside potential at its current beaten-down prices, having fallen 57% from its pre-pandemic peak.

Boeing’s Chief Financial Officer Brian West confirmed that the company’s aircraft deliveries won’t recover as manufacturing troubles continue in the second quarter. Despite this, Boeing projects demand for nearly 44,000 new commercial airplanes by 2043. As interest rates eventually come down and airlines gain breathing space, Boeing’s stock should begin to recover. Core financials are set to make a sharp recovery.

Click to Enlarge

Also, much of the initial drama surrounding Boeing has cooled down already in the past few months.

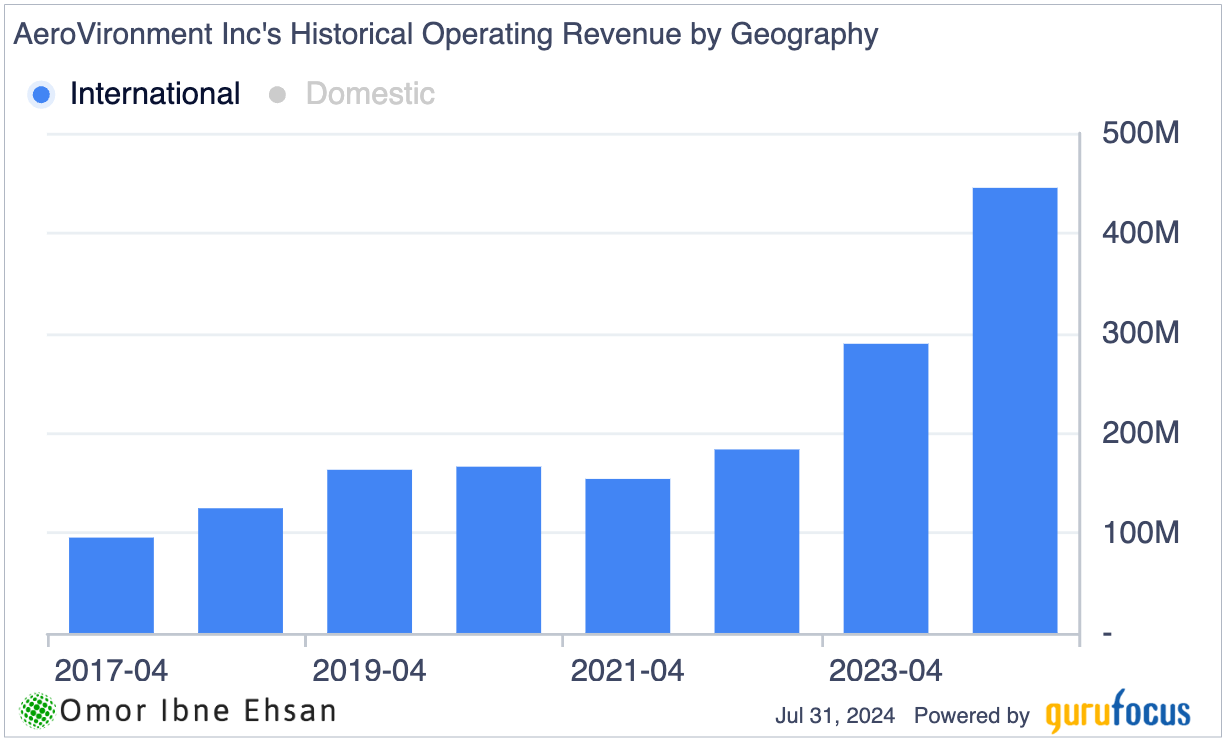

AeroVironment (AVAV)

AeroVironment (NASDAQ:AVAV) designs and manufactures unmanned aerial vehicles (UAVs) for defense and commercial applications. The company has been delivering strong financial results, with fourth-quarter revenue of $197.0 million and fiscal year revenue of $716.7 million, up 6% and 33% year-over-year, respectively.

I think AeroVironment could see substantial growth due to the rising use of drones in different industries, especially in the military. Many countries are exploring the potential of drone swarms, and governments are keen on using drones for various purposes. AeroVironment’s current contracts with defense departments worldwide make it a top player in the drone market. In fact, international orders are actually making up the bulk of its growth.

Click to Enlarge

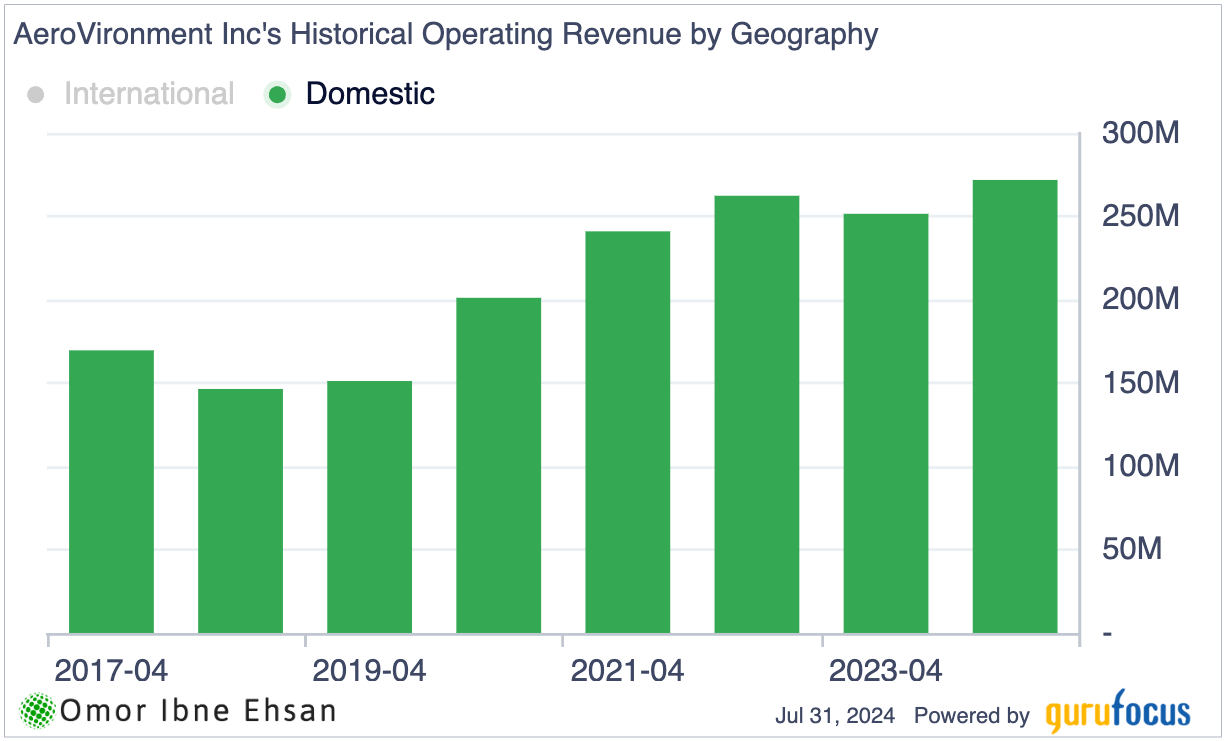

Its domestic sales have basically stalled.

Click to Enlarge

The stock has performed exceptionally well, surging 82% over the past year. However, it has corrected 21% from its June peak and has been relatively flat in the past month. Analysts maintain a bullish outlook on the stock, with a consensus strong buy rating and an average price target of $225, implying a 30% upside potential.

Visa (V)

Visa (NYSE:V) is intrinsically tied to the broader economy due to its dominance in the ways people transact and spend their money. This positions the company to benefit in various economic environments.

During periods of low interest rates, Visa thrives on increased transaction volumes and discretionary spending. Conversely, when rates rise, the company profits from higher lending rates. That’s why I think this is a stock worth buying before the next bull market. Also, it fits the bill in the current climate since you’ll be avoiding much of the recent tech selloff’s turbulence.

The company recently reported fiscal third quarter 2024 results, with revenue growing 10% YOY to $8.9 billion, slightly missing analyst estimates, and GAAP EPS increasing 20% to $2.40.

Recent analyst opinions on Visa have been largely positive. For instance, Jefferies analyst Trevor Williams reiterated a “buy” rating and a $300 (lowered by $25) price target on Visa shares. William Blair’s Andrew Jeffrey also stuck with his “outperform” rating.

UnitedHealth Group (UNH)

UnitedHealth Group (NYSE:UNH) is an insurance company that provides health benefits and services to millions of people worldwide. The company has been delivering solid financial results, with revenue growing 6% YOY to $98.9 billion in Q2 of fiscal year 2024, driven by strong performance in its Optum healthcare services division.

I believe the healthcare industry is one of the most stable and sticky places in which to invest, if you put your money in the right companies. UnitedHealth Group mostly deals with health insurance and is insulated from most of the volatility, benefiting when people have additional money to spend on their health insurance.

Despite some challenges, like the recent cyberattack and divestment of South American operations, analysts remain bullish on UNH stock. Their average rating is a strong buy. While UNH stock has been trending sideways through most of the rally, I believe it could outperform during the next rally since the recent surge was more tech-focused. In a broad-based bull market, UNH should also join in. It has had an impressive 16.5% surge in just the past month.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.