For the past two years, pundits have been calling for a housing market crash that harkens back to 2008. It hasn’t happened yet; and we’re confident that it won’t. Instead, we’re likely to see an unprecedented housing market boom in 2024.

If I had a dollar for every time I heard that the housing market would crash, I might be richer than Elon Musk. Yet, despite the persistent calls for a housing market crash over the past 24 months, we haven’t seen one.

Home prices did retreat a little in late 2022. But that didn’t last long. They’ve come soaring back in 2023. And now the median sales price of a home is $407,000 – which is nearly a fresh all-time high.

Moreover, recent home price trends suggest that whatever small “correction” we did see in home prices is already over.

According to the S&P Case-Shiller Home Price Index, home prices did actually decline for four months in early 2023 – the first time they declined in more than a decade.

But that streak is already over.

What the Housing Market Data Shows

The most recent batch of data shows that home prices rose again. The home price “correction” is over. Home prices are already back on the rise.

How can that be? Hasn’t the Fed jacked up interest rates to levels that make it borderline unaffordable at current levels? Against that backdrop, how are home prices staying high?

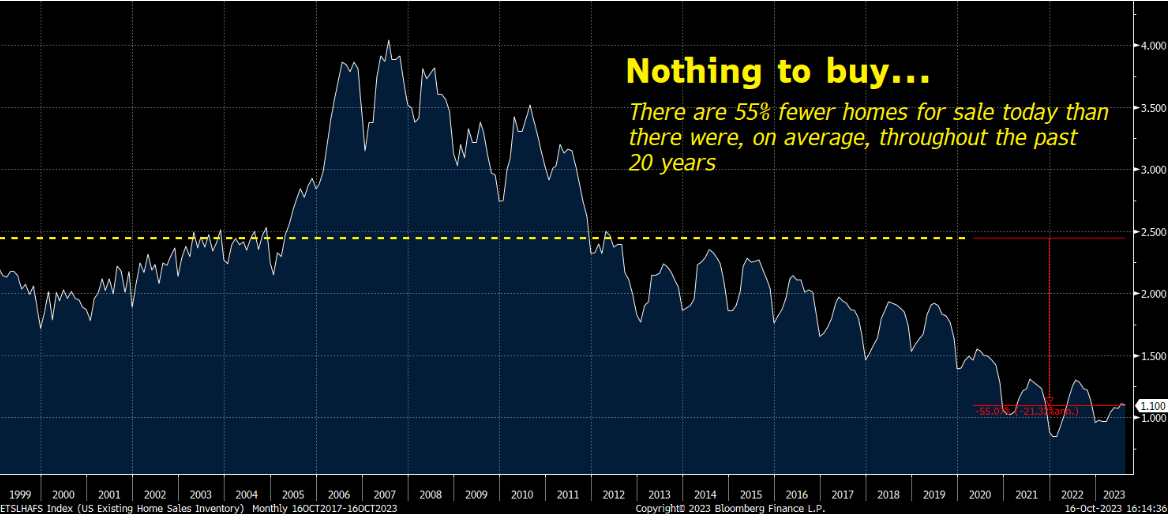

Simple – there’s no inventory.

The price of any asset – like a home – is simply a reflection of supply and demand. The higher the demand and the less supply you have for an asset, the higher the price of that asset.

And right now, the supply of homes is at an all-time low.

There are currently 1.1 million homes for sale in the U.S. That is an all-time low by a wide margin. Throughout the 2000s and 2010s, there were typically 2.5 million homes for sale in the U.S. – more than double the current total.

Of course, that begs the question: Why is supply so low?

Oddly enough, you can blame the Fed.

The Fed Is Diluting Demand and Incentive

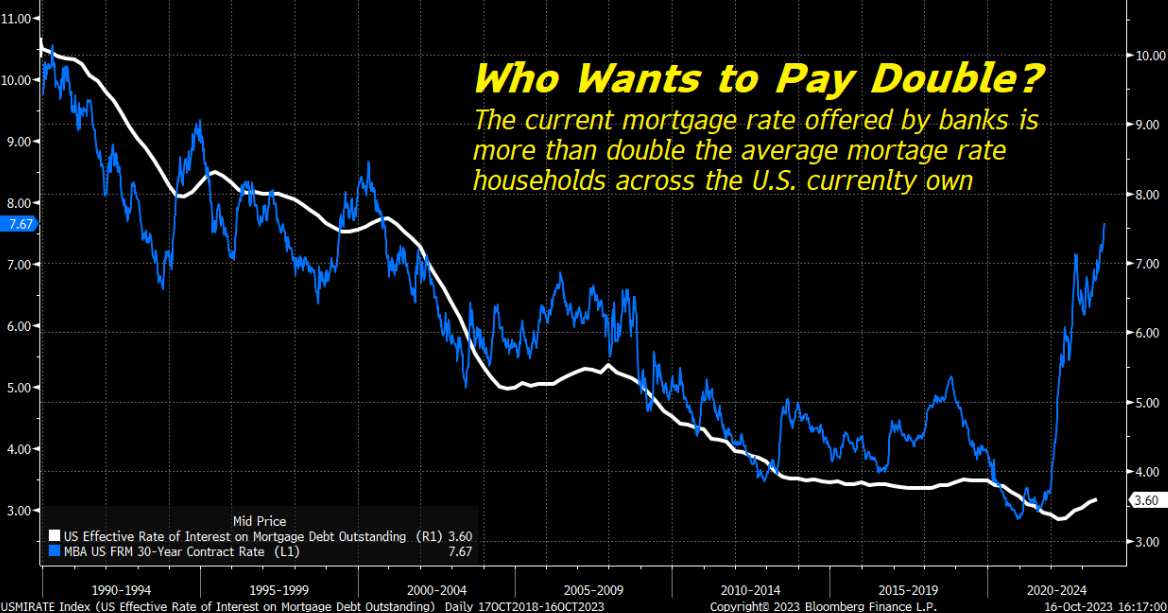

Sure, the Federal Reserve has jacked up interest rates to fight home price inflation by diluting demand through higher mortgage rates.

But the flip side of that coin is that by jacking up interest rates so quickly, it has dramatically decreased the value proposition of trying to sell a home.

The average mortgage rate these days is about 7.6%. But the effective average mortgage rate among U.S. homeowners is 3.6%.

Who wants to swap a 3.6% mortgage rate for a 7.6% one? Apparently, no one. That’s why no one is selling their home unless they absolutely have to and why housing inventory is at an all-time low.

The Final Word on the Housing Market

In other words, the housing market crash that everyone has been predicting for two years now is likely to never come because of an enormous housing inventory shortage.

Sure, if the Fed lowers interest rates in 2024 and the gap between the effective and average mortgage rates narrows, more homeowners would be inclined to sell. But lower rates will also energize a whole army of sidelined prospective buyers.

After all, we’re still hearing that in most markets, there are at least four to five bids per home. That means for each home that sells, there are three or four people still looking for a new home. To meet all the demand, housing inventory would have to triple or quadruple. And that assumes demand doesn’t go up with lower rates.

In short, the housing market isn’t crashing, now or anytime soon. Instead, it is likely to boom as lower rates energize a whole army of sidelined demand in 2024.

And we have some great stocks for you to play that housing market renaissance.

On the date of publication, Luke Lango did not have (either directly or indirectly) any positions in the securities mentioned in this article.