Last week, Elon Musk’s Tesla Inc. (NASDAQ:TSLA) stole headlines by unveiling its prototype for its humanoid robot – dubbed Optimus – at the company’s artificial intelligence (AI) showcase.

On stage the robot walked, waved and even raised the roof. The company also showed videos of Optimus carrying boxes and watering plants around the Tesla office. According to a Tesla engineer, Optimus uses the same AI to detect objects as its cars Autopilot systems.

First, Musk plans to put the robots to work in Tesla’s factories. Long term, Musk has his sights set on a consumer robot that can do things like run errands or be a companion.

Reviews were mixed at best.

By Monday, though, any excitement about Musk’s Optimus dwindled when Tesla reported disappointing delivery numbers, sending shares down more than 8%. (Tesla’s deliveries are the best way for analysts to determine actual sales.)

In today’s Market 360, we’re going to take a look at Tesla’s recent report and what it means for the long-term prospects for the stock.

Tesla Delivers Disappointment

When we last looked at Tesla after its second quarter 2022 earnings report, we highlighted that supply chain issues and shutdowns in China have caused Tesla to raise the cost of its cars 25% to 30% from where they were a year ago… but margins shrunk to around 28% in the second quarter – falling below 32% from the first quarter.

We said, to meet its delivery goal the second half of the year, Tesla would have to ramp up production 70%. Something we thought might be tough with China’s zero-Covid policy threatening to shut down areas of the country again and again.

Fast forward to Sunday’s delivery and production report release, and the delivery goal remains the overwhelming issue.

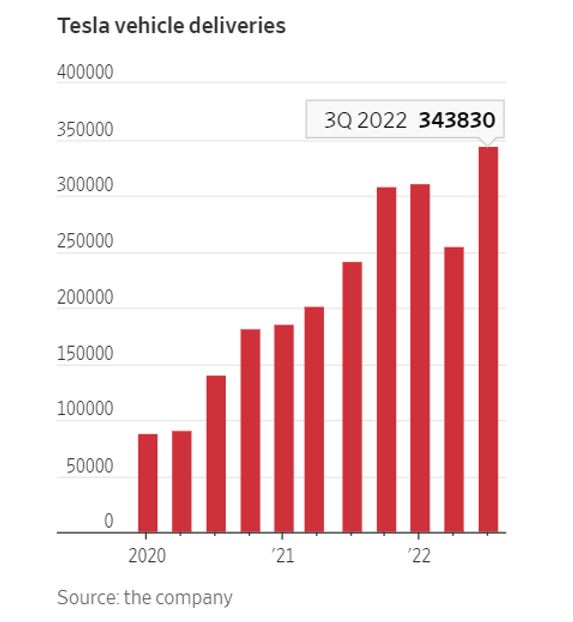

Tesla reported 343,000 total deliveries, which missed analysts’ expectations of 364,660.

That said, as reported by the Wall Street Journal, deliveries were up roughly 42% from last year’s third quarter, when Tesla delivered 241,000 vehicles.

Furthermore, the company’s total production increased from last quarter. Tesla produced 19,935 of its high-end Model S and X vehicles and 345,988 of its more affordable Model 3 and Y vehicles during the third quarter. In quarter two 2022, Tesla said it made 258,580 cars.

As reported by CNBC, “Tesla faced growing pains at its new factories in Germany and Texas, executive turnover and soaring commodity prices in the third quarter of 2022.”

Looking forward, to meet its goal, Tesla will have to deliver 495,000 vehicles in the fourth quarter – something the company has yet to achieve. Per FactSet, Wall Street thinks the company will struggle to meet its goal and deliver only 457,000 vehicles in the final quarter of 2022.

But… Tesla’s Still a Buy

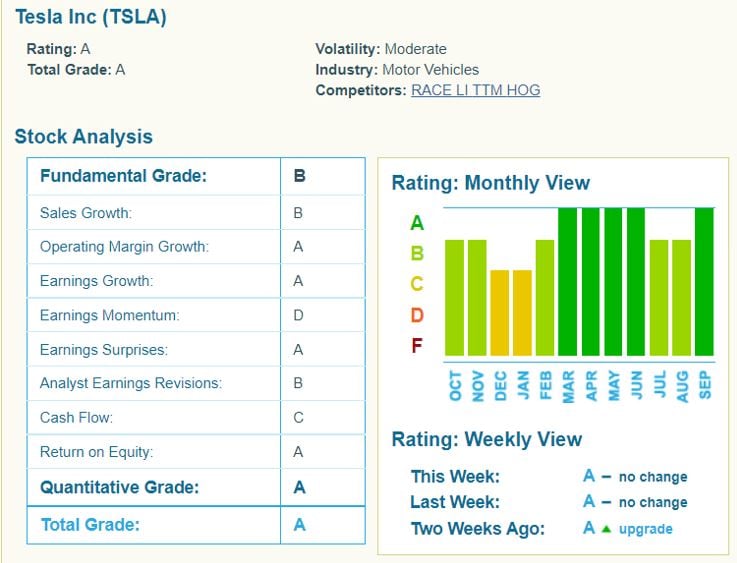

Taking a look at Portfolio Grader, Tesla was recently upgraded to an A-rating, making the company a Buy:

Tesla is scheduled to report third-quarter earnings on October 19. While they fell short of expectations, the company’s deliveries are expected to help the Tesla post its highest quarterly sales and record profits of $3.34 billion.

So no, the company didn’t deliver as many cars as analysts wanted. But the fact is, Tesla has survived the chip shortage better than most automakers because the company learned how to reprogram its cars.

Managing Director for Energy, Sustainability and Mobility Tech at Cowen, Jeffrey Osborne, wrote in a note:

Tesla has ample cash and has undertaken a meaningful global manufacturing expansion with facilities in China, Berlin, and Austin, TX with the latter two approaching full ramp. While competition in the EV space continues to heat up, Tesla’s focus on electrical efficiency and investment in battery technology likely makes them tough to chase in the short term.

If Tesla can beat expectations in a couple of weeks, we could see shares climb higher.

As I’ve been saying folks, fundamentally strong companies will be lifted by earnings – while the weaker companies will continue to struggle.

As we head into earnings season, my Growth Investor Buy List stocks are characterized by 64.2% annual sales growth and 473.9% annual earnings growth. Plus, the analyst community has revised our Buy List stocks’ earnings estimates 22.3% higher on average over the past three months.

How do our Growth Investor stocks remain characterized by accelerating earnings and sales momentum when the rest of the market has experienced a decline?

Well, we were proactive and filled the Buy Lists with companies that can thrive in an environment with a strong U.S. dollar and rising inflation.

To learn more about Growth Investor and how you can set yourself up for success, click here.

Sincerely,

Louis Navellier