This morning, CVS Health Corp (CVS), the pharmaceutical chain, reported earnings that just missed analysts’ expectation. Nonetheless, the results did show the company is growing at a healthy clip. Year-over-Year revenues grew to $38.64 billion, rising 10% (and beating analysts’ forecasts). Meanwhile, EPS came in at $1.11, missing estimates.

Taking a closer look at the results and forward guidance, one thing becomes clear. Now is the time to be cautious on CVS stock.

Taking a closer look at the results and forward guidance, one thing becomes clear. Now is the time to be cautious on CVS stock.

CVS Stock: Quick View

CVS Health has a solid growth story. The company, through aggressive M&A, has been expanding. The goal, of course, was to gain more and more market share. That, in turn, would give CVS more negotiating power with pharmaceuticals and thus secure better margins.

The M&A phase began with the Omnicare(OCR) merger and later the purchase of Target’s chain store pharmacies. The purchase of Omnicare was especially important. The Omnicare merger allowed CVS to gain greater access (and thus demand) from nursing homes. As baby boomers age, that segment will become a bigger and bigger market.

CVS Earnings Flagged Risks

At $1.11 EPS, CVS Earnings

missed estimates of $1.30 EPS. The excuse was, of course, operational costs involving the Omnicare merger. While missing estimates is never a good thing, it’s not the real reason investors should be worried. So what is that reason?

Let me backtrack and correct that question: So what are those reasons? There’s your clue. First, CVS lowered its guidance for 2016-2017 to $5.68- $5.88 per share, on the back of the merger costs. Second, the company reported that the financial leverage (aka debt) jumped above the 2.7 target. CVS has said they will act to reduce it, but that’s not necessarily a good thing.

CVS has basically been funding its growth strategy (i.e. M&A) with debt. This means that mergers could be put on hold until the leverage falls back. In other words, the buying spree which led to the rise in revenues is also on hold. See, that’s not such good news.

True, in the long run it will reduce the risk for CVS stock. But it also means that, as long as leverage falls, so will the ROE. That, of course, makes CVS stock less attractive.

Hillary Clinton Not Helping

Another reason for concern comes from presidential candidate, Democrat Hillary Clinton, who proposed a cap on drug costs. Now, at this early stage in the primaries, no one knows if Mrs. Clinton will even be nominated for president. Nor is it a done deal that, if elected, her campaign proposal would even make it into law. Still, the risk is there.

Consider that possibility, though. CVS has made leveraged buyouts to increase its market share and profit margins. A sudden cap on the price of medicines could certainly erode profits. Even if the proposal doesn’t ever come up in Congress, the uncertainty could eventually weigh on CVS stock.

CVS stock Value vs Risk

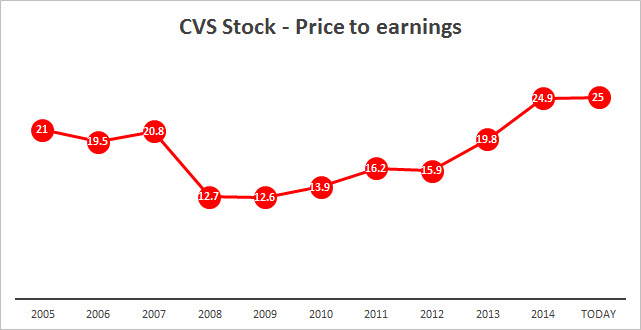

Now, don’t be mistaken; CVS stock still has a lot going for it. With the Target merger and a focus on aging baby boomers, CVS has demographics on its side. But CVS stock is currently trading at a P/E ratio of X25, historically, its highest multiple in more than a decade. As illustrated in the chart below, if we add that high premium to looming risks we reach one conclusion. Given the current earnings and potentially declining ROE, CVS stock is pricey.

Click to Enlarge

CVS stock needs to be put aside until the price reflects that uncertainty or until that uncertainty abates. Since uncertainty could be long term, this writer believes the former scenario might be the most likely.

As of this writing, Lior Alkalay did not hold a position in any of the aforementioned securities.