Due to the novel coronavirus, all travel-related stocks have been under severe pressure. That includes Uber (NYSE:UBER). However, it would be foolish to think that the virus will wipe out ride-hailing companies, eliminating Uber stock and Lyft (NASDAQ:LYFT).

That doesn’t mean both companies are created equal, though. Although both firms were thrust into a difficult position, they are not alone. Almost every company — from Fortune 500 brands to mom-and-pop small businesses — has been impacted as well.

However, there are multiple reasons that Uber stock is a better pick than Lyft stock.

Uber Is Larger

Click to Enlarge

Uber operates around the world. As a result of consumers’ familiarity with it, they tend to use it more consistently than Lyft, leading to more repeat revenue for Uber.

But sometimes operating in other countries creates headaches for both companies. Some of these countries are profitable and some are not. However, Uber is the dominant player here in the U.S.

Growing too quickly can create problems, and that’s been the case sometimes for Uber. However, large reach can also give companies an advantage over their competitors, which we’re also seeing play out between Uber and Lyft.

When Uber was making every mistake in the book, Lyft had the opportunity to expand to more markets and take market share. Lyft did that, but not to a sufficient extent.

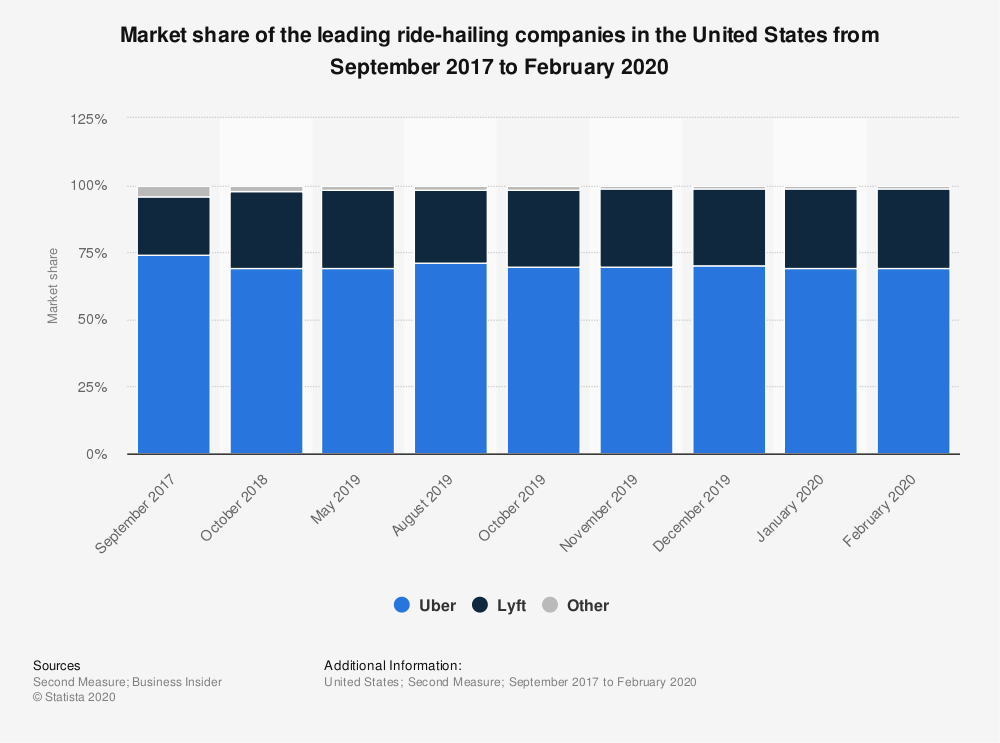

Lyft’s market share increased from 22% in September 2017 to 30% as of February 2020. However, Uber only saw its market share sink from 74% to 69% during the same period. In other words, Uber still dominates.

Uber’s Financials

We can extrapolate all of the numbers and make this into a long section. But there’s no reason to do so. I placed the higher number in each category in bold type below.

| Metric | Uber | Lyft |

| Revenue (ttm) | $14.15B | $3.62B |

| Gross Margin (ttm) | 49.05% | 39.81% |

| Operating Margin (Q) | -23.86% | -37.54% |

| Quick Ratio (Q) | 2.3 | 1.2 |

| Total Cash (Q) | $11.3B | $2.95B |

Lyft is superior to Uber when it comes to free cash flow. Both companies generate negative FCF, but Lyft’s total burn is smaller than Uber’s. I believe that’s due to Lyft’s smaller size. But Uber has higher revenue, generates higher gross and operating margins, and has a stronger balance sheet.

Plans for Profitability

Lyft expects to become profitable by the end of 2021. That was a solid goal, with the company coming public in 2019 and now easing investors’ concerns about its bottom line. However, Uber subsequently said it plans to be profitable by the end of 2020, a full year ahead of Lyft.

Uber’s larger size and improved bottom line will help fuel its way to break-even operations ahead of its smaller peer. Of course, that is likely to all change due to the coronavirus outbreak.

We’re not yet sure how the pandemic will impact Uber’s goal of reaching profitability by the fourth quarter of this year. Uber’s management also probably isn’t even sure about that at this point, as it pulled its guidance and reduced its revenue outlook.

However, we know that Uber is in a stronger position than Lyft from a financial perspective. On top of that, Uber was expecting to become profitable well before Lyft. That’s encouraging, even if that goal ends up being pushed back due to the coronavirus.

Uber’s Technicals Are Stronger, Too

Click to Enlarge

Uber stock has been clobbered and it doesn’t take a rocket scientist to figure out why. With lockdown and stay-at-home orders plentiful, few people are leaving their homes, let alone traveling around the country.

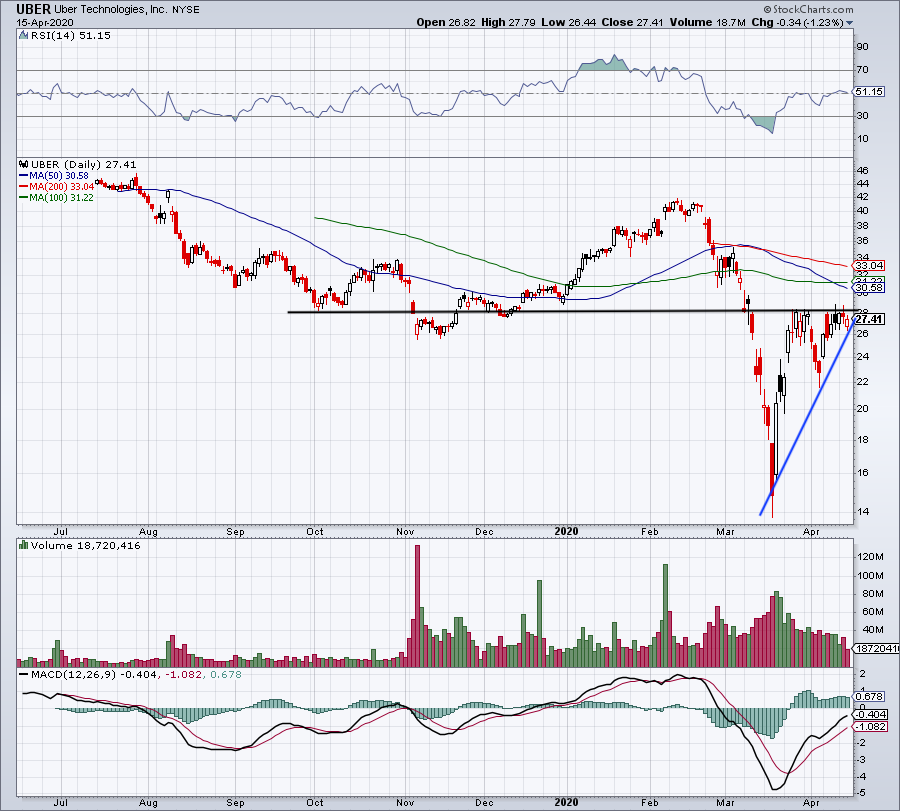

That dealt a blow to the stock’s charts, although Uber stock has done a great job at rebounding. Its shares hit a low just below $14 last month and have since doubled.

If the stock can break out over $28, it could reach the $30.50 to $33 area, where it will run into its 50-day, 100-day and 200-day moving averages. On the downside, a break below $26 could put $22 back in play, particularly if the drop comes amid a selloff of the stock market.

Further, Uber stock is down just 5% in 2020. That’s much better than Lyft’s 30% slide and even better than the S&P 500’s performance. I’m not saying that Uber is the best stock to buy in the market. However, it appears to be a better investment than Lyft.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.