PPI inflation comes in hot … the Red Sea problem isn’t getting better … Louis Navellier is bullish on oil … yesterday’s bad retail sales report … is the U.S. consumer finally cracking?

It’s a busy news cycle. Let’s bounce around to a handful of stories likely impacting your portfolio.

Today’s Producer Price Index (PPI) confirmed that inflation can be stickier than we want

As we covered in the Digest on Tuesday, January’s CPI number came in above forecasts, resulting in a heavy down day on Wall Street.

The selling pressure was due to fears that the hotter-than-expected CPI data would cause the Federal Reserve to delay its initial rate cut, while potentially cutting rates fewer times in 2024.

The hope was that today’s Producer Price Index (PPI) print would be more encouraging, giving the Federal Reserve members the “cool” data that they’re looking for. Instead, the number also came in higher than expected.

Here’s CNBC:

Wholesale prices rose more than expected in January, further complicating the inflation picture, according to a U.S. Department of Labor report Friday.

The producer price index, a measure of prices received by producers of domestic goods and services, rose 0.3% for the month, the biggest move since August. Economists surveyed by Dow Jones had been looking for an increase of just 0.1%. PPI fell 0.2% in December.

Excluding food and energy, core PPI increased 0.5%, also against expectations for a 0.1% gain. PPI excluding food, energy and trade services jumped 0.6%, its biggest one-month advance since January 2023.

As I write, Wall Street is responding as it did to Tuesday’s hot CPI report – poorly.

It knows that the Federal Reserve is basing its rate-cut decisions on inflation data. Clearly, this week’s inflation data isn’t supportive of fast-and-furious rate cuts that were the centerpiece of the 2024 bull market thesis at the turn of the year.

Just a few weeks ago, the futures market was pricing in the first rate cut in March. Today, it’s a coinflip that a cut happens in June. And if the inflation data continue to prove stubborn, next fall is the safer bet.

Regardless of when it happens, you can kiss the idea of a slew of rate cuts in 2024 goodbye (barring a recession). So, if your portfolio requires lots of cuts as fuel for gains, be careful today.

Speaking of inflation, keep your eye on continuing problems in the Red Sea and its impact on consumer goods prices

As we’ve been reporting in the Digest, Houthi rebels have continued their missile-strikes on ships in the Red Sea, disrupting one of the world’s busiest trade routes. Since November, the Houthis have attacked or threatened commercial ships at least 46 times, according to U.S. defense data.

This is a major problem for global commerce since the Red Sea is the only route to the Suez Canal (from Asia) and is a lifeblood for trade connecting Europe and the East. About 12% of global trade comes through the canal, which represents approximately 30% of all global container traffic.

Despite hopes that Western governments would be able to stop the Houthi attacks, the situation is deteriorating and shipping companies are sounding the alarm.

From CNBC on Wednesday:

A.P. Moller-Maersk, the second-largest global ocean carrier, is advising customers to prepare for a Red Sea crisis that could stretch well into the second half of this year.

“Unfortunately, we don’t see any change in the Red Sea happening anytime soon,” Charles van der Steene, regional president for Maersk North America, tells CNBC.

“We’re advising them the longer transit routes could last through Q2 and potentially Q3. Customers will need to make sure they have the longer overall transit time built into their supply chain.”

These longer transits are impacting shipping costs.

Here’s JPMorgan:

While several aggregate measures of container shipping costs are now two-and-a-half to three times of their early December levels, prices along routes that typically go through the Suez Canal — particularly from Asia to Europe — have surged nearly five-fold.

Costs from China to the U.S. have also more than doubled.

For now, we’re seeing limited impact on consumer prices. Shipping costs aren’t a huge portion of most product’s total cost, and many manufacturers are eating the markup to protect customer loyalty.

But if the situation doesn’t improve, that’s likely to change, throwing a monkey wrench into the fight against inflation.

Back to JPMorgan:

As global goods disinflation has been the primary driver of lower inflation around the world, the recent reductions in global shipping capacity, at the very least, risk interrupting the disinflationary trend.

At worst, they will push traded goods prices higher for a period of time. While we do not expect a rise anywhere near as large as the COVID-era shock, even a modest rebound in goods inflation could render global core CPI inflation sticky around the 3% mark.

If inflation stalls out at 3% (50% higher than the Fed’s target inflation rate), the question stops being “how many cuts will we get from the Fed this year?” and becomes “will the Fed cut rates at all this year?”

As we noted earlier in this Digest, if you’re banking on lots of rate cuts, be careful.

Meanwhile, are you ready for an oil trade?

One week ago today, we analyzed the oil market with the help of our macro expert Eric Fry. Our conclusion was oil and energy stocks appear attractive for a trade – both on a shorter-term basis (as we head toward the summer) and a longer-term basis (as supply shocks hit the market by 2025).

Well, oil keeps climbing, and legendary investor Louis Navellier is feeling bullish about his Big Energy Bet.

Let’s jump to Louis’ Special Market Update Podcast from Growth Investor earlier this week:

Oil prices are up, and, of course, we still have our Big Energy Bet. It’s very important that you have stocks that zig when others zag, which is why I keep the energy bet.

Energy stocks benefit in the spring because as people get out-and-about more, demand rises. There have also been many refineries that have shut down for maintenance, so inventory for refined products is pretty tight right now.

So, I like my best energy stocks.

Unfortunately, I can’t share with you those specific names since they’re reserved for subscribers. But I’ll offer you the next best thing – Louis’ free Portfolio Grader tool.

If you’re new to the Digest, Louis is a quant investor which means he bases his market activity on cold, impartial numbers instead of hunches or guesses. Louis analyzes eight key fundamental factors:

- sales growth

- operating margin growth

- earnings growth

- earnings momentum

- earnings surprises

- analyst earnings revisions

- cash flow

The Portfolio Grader is a free diagnostic tool that evaluates the earnings strength of a stock you’re considering through these same metrics. It’s the next best thing to calling Louis directly and asking for his opinion on a stock.

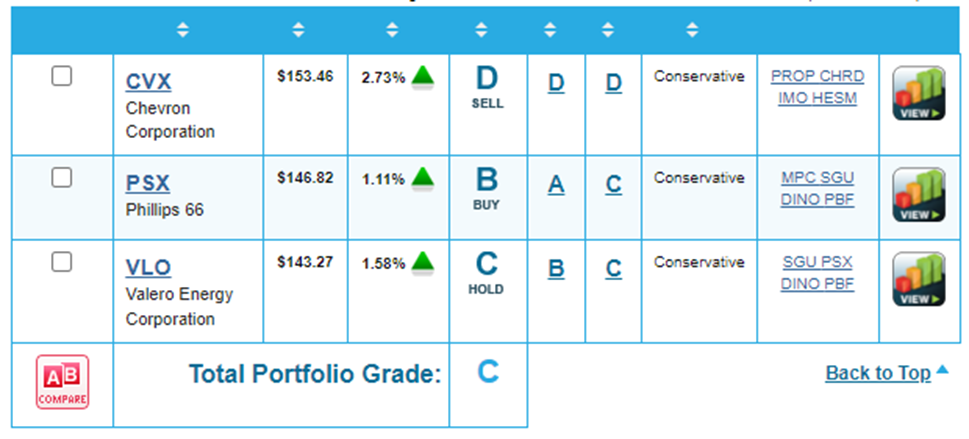

To illustrate, say you’re trying to decide between adding one of three energy plays to your portfolio: Valero, Chevron, and Phillips 66.

Which one might Louis pick?

Here you go:

Phillips 66 is the only one with an active “buy” status today.

To take the Portfolio Grader for a test drive, just click here.

Finally, Louis isn’t pleased with yesterday’s retail sales report

Yesterday, we learned that consumer spending fell hard in January, signaling cracks in the “resilient” U.S. consumer.

From CNBC:

Advance retail sales declined 0.8% for the month following a downwardly revised 0.4% gain in December, according to the Census Bureau.

A decrease had been expected: Economists surveyed by Dow Jones were looking for a drop of 0.3%, in part to make up for seasonal distortions that probably boosted December’s number.

However, the pullback was considerably more than anticipated. Even excluding autos, sales dropped 0.6%, well below the estimate for a 0.2% gain.

Here’s Louis’ perspective from yesterday’s Growth Investor Special Market Update podcast:

The retail sales report was very disappointing. It was weak across the board.

The only thing that was really up was furniture sales and spending at bars and restaurants…

Clearly, consumers spent too much during the holidays…

Now, it wasn’t all bad. In today’s upside-down market, the silver lining of weaker consumer spending is that it gives the Fed some data supportive of a rate cut.

Back to Louis:

The disastrous January retail sales report will cause a lot of downward GDP revisions.

Don’t let that bother you, because it will just make the Fed consider cutting rates sooner than later.

For more color on the health of the U.S. consumer, let’s rewind to last week’s latest data on consumer debt

According to TransUnion, credit card balances jumped 10% from one year ago. The average balance sits at $6,360, which is the highest it’s ever been.

Now, that alone isn’t huge cause for concern. Part of this elevated figure reflects inflation.

The more concerning aspect is how more Americans are unable to pay off their balances each month.

Back to CNBC:

…Households continue to show signs of strain — more cardholders are carrying debt from month to month or falling behind on payments.

Credit card delinquency rates jumped across the board, the New York Fed and TransUnion found. Credit card delinquencies surged more than 50% in 2023, the New York Fed reported.

According to TransUnion’s research, “serious delinquencies,” or those 90 days or more past due, reached the highest level since 2009.

“Consumers are struggling with their payments,” Wise said. “I think we will continue to see those delinquencies tick up.”

Now, as Louis noted, this could accelerate the timing of the Fed’s first interest rate cut. But as it stands today, this has all the makings of a photo finish…

Will the U.S. consumer be able to hold out until the Fed lowers interest rates, taking pressure off nosebleed credit card interest rates and balances, as well as squeezed household budgets?

Or will more sticky inflation data mean the Fed doesn’t cut rates anytime soon, which causes consumers to tap out and stop spending later this year, dashing hopes of a soft landing?

Based on this week’s inflation data, it’s looking neck-and-neck.

We’ll keep you updated on all these stories here in the Digest.

Have a good evening,

Jeff Remsburg