The case for short- and long-term profits in oil … a brewing supply shortage … green energy can’t fill the gap yet … plateauing interest in EVs … how to play the coming oil boom

Oil and gas stocks are setting up for another run that’s going to make investors a hefty chunk of change.

There are actually two runs in the making…

A shorter-term profit opportunity as we move toward the summer, then a longer-term opportunity as our global economy faces the reality that we can’t transition to green energy yet – and we have an oil shortage.

That last part might raise an eyebrow – an oil shortage? Don’t we have an oversupply today?

Hang on, we’ll cover that.

Let’s begin with a 30,000-foot view of where the energy market is today

For help, here’s our macro expert Eric Fry, editor of Investment Report:

Although the energy sector has been “dead money” for more than a year, it was very much alive prior to that…

Energy stocks, in general, are reflecting soft demand and soft prices for oil and gas…

Global crude supply is roughly in balance with global demand. Despite this momentary parity, demand could soon begin outpacing supply, thanks to reviving economic growth worldwide.

We can see this “dead money” by looking at the SPDR Energy Select Sector ETF (XLE). It holds energy heavyweights including Exxon, Chevron, Conoco, Hess, and Phillips 66.

While XLE has offered some shorter-term swing trading profit opportunities in recent quarters, it has been flat since summer of 2022.

This sideways action makes more sense when we look at the price of West Texas Intermediate Crude (WTIC), which is the U.S. benchmark for oil.

As you can see below, over the same period since summer 2022, its price has cratered 36%.

So, what’s the case for a bullish trade at this point?

First, if you believe that Federal Reserve Chairman Jerome Powell has pulled off the near-impossible and engineered a soft landing (or a “no landing” as some analysts now suggest, meaning the economy won’t slow at all), then you’re an oil bull by proxy.

A stabilizing/strengthening economy is inherently bullish for oil demand, and by extension, oil prices.

Second, we have seasonality working in our favor.

As legendary investor Louis Navellier often points out, oil prices tend to climb as we move toward the summer driving season. You can almost set your watch to it. This is a tailwind behind earnings for oil companies as we move toward Q2 earnings season.

In fact, JPMorgan just came out with its forecast for Brent Crude. It expects we’ll see prices hit the high $80s by May.

Historically, Brent trades slightly higher than WTIC, so the WTIC-equivalent of this forecast would be prices in the mid-$80s by May, or a gain of about 15%.

Third, XLE’s technical charts suggest brewing bullishness. We can see this in XLE’s Relative Strength Index (RSI) and moving average convergence/divergence (MACD) indicators.

The RSI and MACD are two trading tools we often reference in the Digest to give us a better sense of a stock’s direction and momentum.

As you can see below, XLE’s RSI and MACD fell toward oversold levels back in January but have been building strength ever since as XLE has pushed higher.

There’s plenty of room on the RSI and MACD charts for more gains before XLE reaches overbought territory.

But all of this supports a short-term trade, meaning the next few months. And while that could result in a nice, low double-digit pop, the bigger opportunity lies farther out on the horizon…

An historical supply shortage could turbocharge prices as we look ahead two years

A reason often cited for why oil prices trade at today’s relatively low price is record oil production from the United States. Abundant supply prevents prices from rising.

This is true, but don’t get used to it. There’s a major shortage brewing.

Let’s go to CNBC:

The oil market will face a supply shortage by the end of 2025 as the world fails to replace current crude reserves fast enough, Occidental CEO Vicki Hollub told CNBC on Monday.

About 97% of the oil produced today was discovered in the 20th century, she said. The world has replaced less than 50% of the crude produced over the last decade, Hollub added.

“We’re in a situation now where in a couple of years’ time we’re going to be very short on supply,” she told CNBC’s Tyler Mathisen…

For now, the market is oversupplied, which has held oil prices down despite the current conflict in the Middle East, Hollub said. The U.S., Brazil, Canada and Guyana have pumped record amounts of oil as demand slows amid a faltering economy in China.

But the supply and demand outlook will flip by the end of 2025, Hollub said.

The shortage brewing in plain sight

Western governments really don’t like oil. If they had their way, green energy would power our world.

Now, that would be great, and I’m all for it. But today, it’s not economically feasible. At this point in time, green energy at scale is too expensive for the global economy. We still need fossil fuel energy.

The problem is many western governments have been disincentivizing oil production even though green energy can’t fill the energy gap.

Let’s rewind to Reuters from last fall:

Government policies to fight climate change are discouraging oil companies from investing heavily in new production even as they turn in record profits – a dynamic that could spell tight supply and high prices as clean energy alternatives seek to fill the void…

“If we don’t maintain some level of investment in the industry, you end up running short of supply which leads to high prices,” Exxon Mobil CEO Darren Woods said.

He said oil and gas reserves are depleting at 5-7% annually, and output will decline if companies stop investing to replace them.

Let’s get more granular to see what’s really happening.

Here’s Eric to fill in some key details:

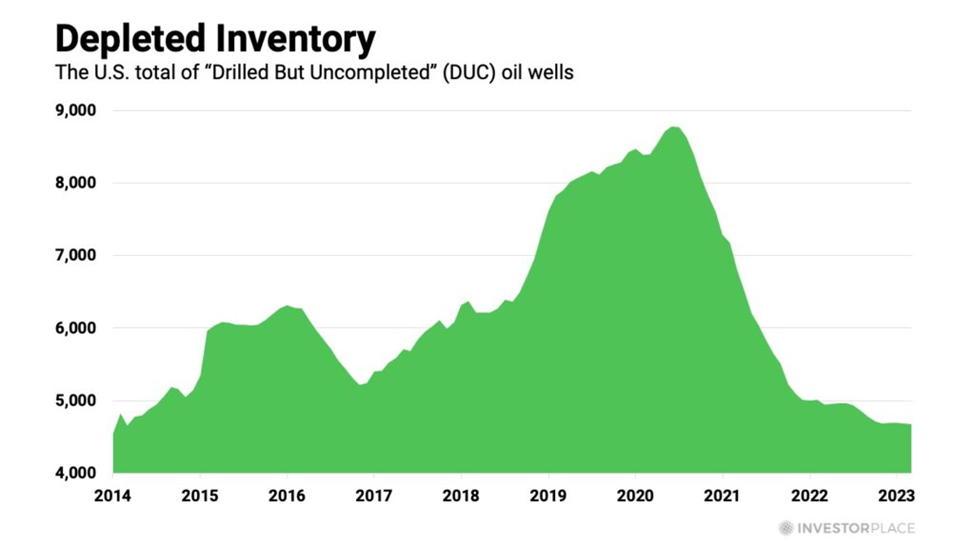

The number of Drilled But Uncompleted (DUC) wells has dropped to the lowest level in more than a decade.

A DUC well is one that has been drilled, but not yet been brought into production. In other words, the well has been drilled to the target depth, but the completion process has not yet been carried out.

Because an oil company can bring DUC wells into production quickly, they provide a great way to capitalize on oil price spikes without having to make sizeable new investments. Oil companies have been doing exactly that during the last four years.

As a result, the remaining inventory of DUC wells has dropped to a 10-year low. These low inventories mean that U.S. oil companies have exhausted most of the “easy money” they could make from oil price spikes.

Going forward, therefore, they would need to boost spending on new drilling activity, but that isn’t happening.

The number of active oil-drilling rigs in the U.S. has been falling for more than a year and currently sits 26% below the 10-year average number.

In other words, there is no significant U.S. supply boost on the horizon.

But wait, let’s step back. Why do we even need oil?

Studies show that in OECD member countries (Organization for Economic Co-operation and Development), 49.24% of all oil consumed is related to motor vehicle usage.

Aren’t we racing toward a world where we all drive electric vehicles?

Reality always wins

Two weeks ago in the Digest, we profiled the carnage in the electric vehicle (EV) sector.

From mid-2021 to mid-2023, EV sales penetration soared from 3% to 8%. But over the past six months, EV sales penetration has plateaued around 8% of total auto sales in the U.S. Meanwhile, the stocks of EV companies have been utterly destroyed.

Why?

Well, a huge number of drivers simply don’t want EVs. They’re more expensive than gas-powered cars, less reliable, and the national infrastructure of EV charging stations is nowhere near robust enough to make recharging convenient.

But don’t take it from me. Look at Ford.

From Reuters last week:

Ford Motor reported an about 11% fall in January sales of electric vehicles (EV) on Friday, as the industry grapples with shrinking demand for the cars that are typically costlier than their gasoline-powered counterparts…

Last month, Ford said it would reduce production of its marquee F-150 Lightning electric pickup truck at its Michigan Rouge EV plant, and increase production of gas-powered Bronco SUVs and Ranger pickups.

High prices of EVs and concerns about the limited range of these cars, especially in rural areas due to lack of charging infrastructure, have fueled sales of hybrid vehicles.

And here’s Business Insider:

…The pace of adoption has markedly slowed, and analysts have suggested the country is no longer on track to hit the government’s sales targets. The trickle-down effects of this decreased demand are everywhere.

EVs accumulated at dealerships [last] fall, even as automakers cut prices to try to entice customers.

Automakers have backtracked on their promised investments: Ford delayed $12 billion of its planned $50 billion investment in EV manufacturing capacity, while General Motors delayed production of key EV models and scrapped a $5 billion partnership with Honda to make cheaper EVs.

Even Tesla — once the superstar of EVs — announced it would delay a planned factory in Mexico.

Auto execs who were once trumpeting the potential of electric cars are even publicly acknowledging that EVs aren’t working.

If drivers are growing less enthusiastic about EVs and refocusing on gas-power vehicles, that’s going to goose oil demand at the same time that oil supply is being tapped out. That’s a great combo for higher prices.

Back to Eric:

Remember, the U.S. has supplied almost all of the world’s crude production growth during the last decade, not OPEC. In fact, OPEC production has fallen 22% during the last seven years.

A fresh wave of investment in exploration and production (E&P) could boost output somewhat, but very few oil companies are expressing any intention to do so.

Rising crude demand, coupled with flat supply growth, provides ample reason to take another swing at the oil market.

How do you play it?

The two simplest options are broad market ETFs.

There’s XLE which we profiled earlier. There’s also XOP, which is the S&P Oil & Gas Exploration & Production ETF. Its top 10 holdings include Antero Resources, Hess, Valero, Southwestern Energy, and Callon Petroleum.

If you subscribe to Eric’s newsletter Investment Report, you can access the portfolio to see Eric’s recommendations here. If you’d like to learn more about joining Eric in Investment Report, click here.

Bottom line: Oil demand isn’t going away anytime soon. But supply is.

Invest accordingly.

Have a good evening, Jeff Remsburg