Penny stocks are some of the best investments if you are looking for high-risk, high-reward bets to quintuple your money. That’s definitely easier said than done since most penny stocks in the market have loss-making underlying businesses and a lot of dilution.

However, it is still possible if you look at up-and-coming startups in sectors with a lot of tailwinds. These startups could deliver multibagger gains overnight if they land big contracts or deliver market-beating earnings.

In addition, rate cuts are likely very close right now. This would significantly improve the market environment for all penny stocks and help them restart growth.

With that in mind, explore seven overlooked penny stocks that could quintuple your money by 2026.

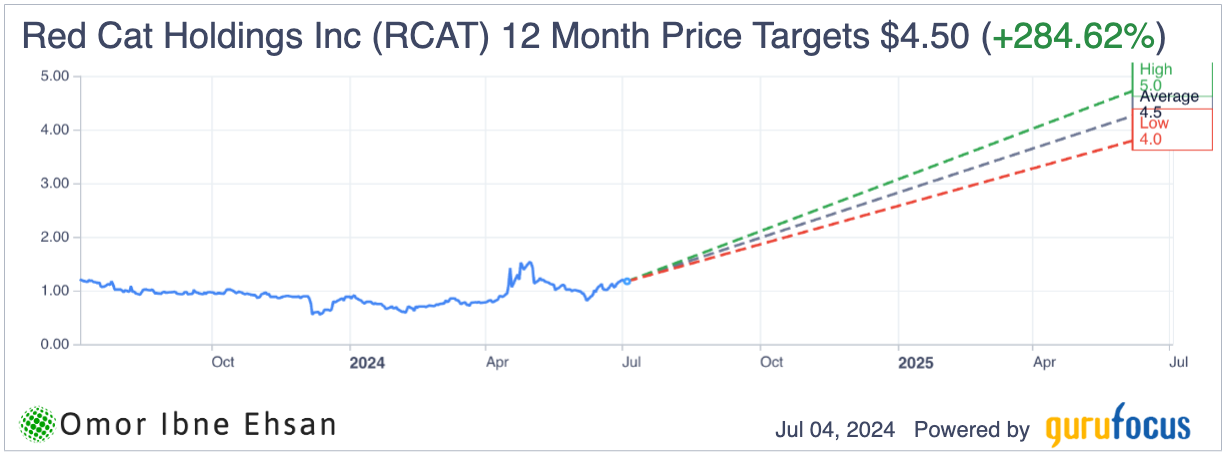

Red Cat Holdings (RCAT)

Red Cat Holdings (NASDAQ:RCAT) manufactures small unmanned aircraft systems (sUAS). I believe this under-the-radar drone stock could take flight and potentially deliver 5X returns by 2026. The company’s Q3 results were stellar, outperforming guidance by 16% to achieve record revenues of $5.85 million, up a staggering 88% year-over-year (YOY).

The star of the show is RCAT’s Teal 2 drone, which is rapidly gaining traction as the go-to sUAS for the U.S. Department of Defense (DOD), federal agencies and over 10 NATO countries. Teal 2 sets itself apart by its unrivaled nighttime capabilities and open-source architecture. These allow customers to easily integrate their preferred software, similar to downloading apps on an iPhone.

Red Cat Holdings is wisely partnering with top-tier software providers like Teledyne FLIR, Tomahawk Robotics—now part of AeroVironment (NASDAQ:AVAV)—and Primordial Labs to offer cutting-edge features like AI, autonomous tracking, voice control and multi-drone “swarming.” These high-margin software add-ons could boost RCAT’s profitability by 20-25%. Analysts covering this stock see huge potential going forward.

Click to Enlarge

It is one of the few publicly traded U.S. small drone manufacturers. Thus, I believe Red Cat is well-positioned to secure big defense contracts as it gains recognition.

Vislink Technologies (VISL)

Vislink Technologies (NASDAQ:VISL) is a video communications company that serves various sectors. It sells with high-quality live video feeds. For example, VISL can manage live video feeds for sports events. Its growth prospects look promising as demand for its technology surges across the industries it serves.

The stock has rebounded nearly 20% in the last six months. If Vislink Technologies can secure major contracts, particularly in the defense and law enforcement space given the favorable geopolitical landscape, the upside could be tremendous.

Further, Q1 results showed robust 20% YOY revenue growth to $8.6 million. This was driven by strong military and government customer adoption of products like AeroLink. Vislink Technologies is smartly pivoting to higher-margin solutions with recent rollouts like Cliq and LiveLink targeting key growth markets. Management expects these new products to approach 70% of total sales this year.

Plus, services and software revenue ticked up to 16% of the mix in Q1. Continued expansion here, especially with Vislink’s LINK MATRIX device management platform, could be a major profitability driver. Revenue is projected to surge 27% this year, and losses are anticipated to narrow by 57%.

Porch Group (PRCH)

Porch Group (NASDAQ:PRCH) provides vertical software and insurance solutions for the home. The company’s first-quarter results showed strong execution, with over 30% revenue growth YOY to $115.44 million, beating estimates by nearly $11 million. I was particularly impressed by the $5 million improvement in adjusted EBITDA.

Despite an early and costly Texas storm season that dented Q1 results by $8 million more than anticipated, management still raised full-year adjusted EBITDA guidance. Plus, the company has much best-in-class gross loss and combined ratios compared to industry peers. The successful April 1 reinsurance renewals will also provide strong a tailwind going forward.

This stock was on its last legs after the late 2021 selloffs that went through all of 2022. However, it did make a short-lived comeback, but it is down again by around 65% from April’s peak. I think that the stock is at an undervalued level now and could bounce back much higher in the coming months. Nevertheless, I’m more optimistic about its long-term prospects since losses are expected to narrow substantially. And, the company is expected to see 13%-plus annual sales growth starting next year. The biggest upside catalyst will be the rate cuts.

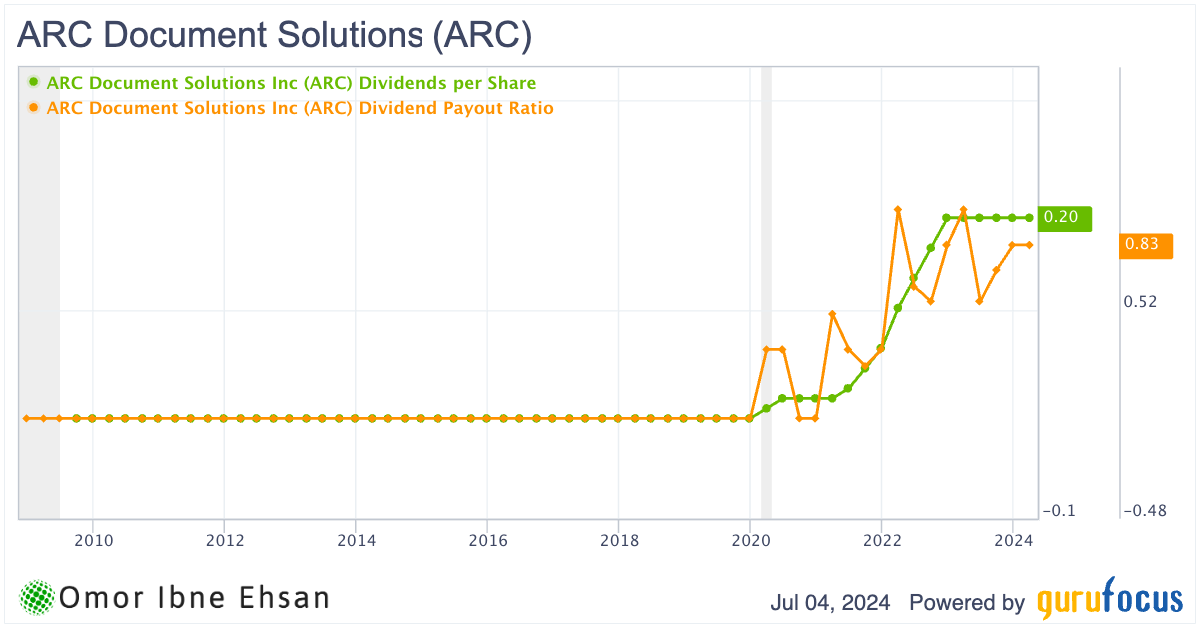

ARC Document Solutions (ARC)

Not all penny stocks have to be loss-making bets. ARC Documents Solutions (NYSE:ARC) is profitable and actually pays a dividend. The dividend yield is currently at 6.71%.

Regardless, the growth is a little bit muted, but plenty of margin expansion is ahead to drive upside. Of course, the printing business doesn’t have the best growth runway, but I believe the profitability it has will allow it to diversify more in the long run.

Click to Enlarge

Already, the company is expanding its addressable markets by targeting new verticals with customized marketing solutions. I believe if it can continue the trend of beating estimates, it can unlock substantial upside. Although it may not be the sexiest business, I still think it is a compelling under-the-radar pick with multibagger potential.

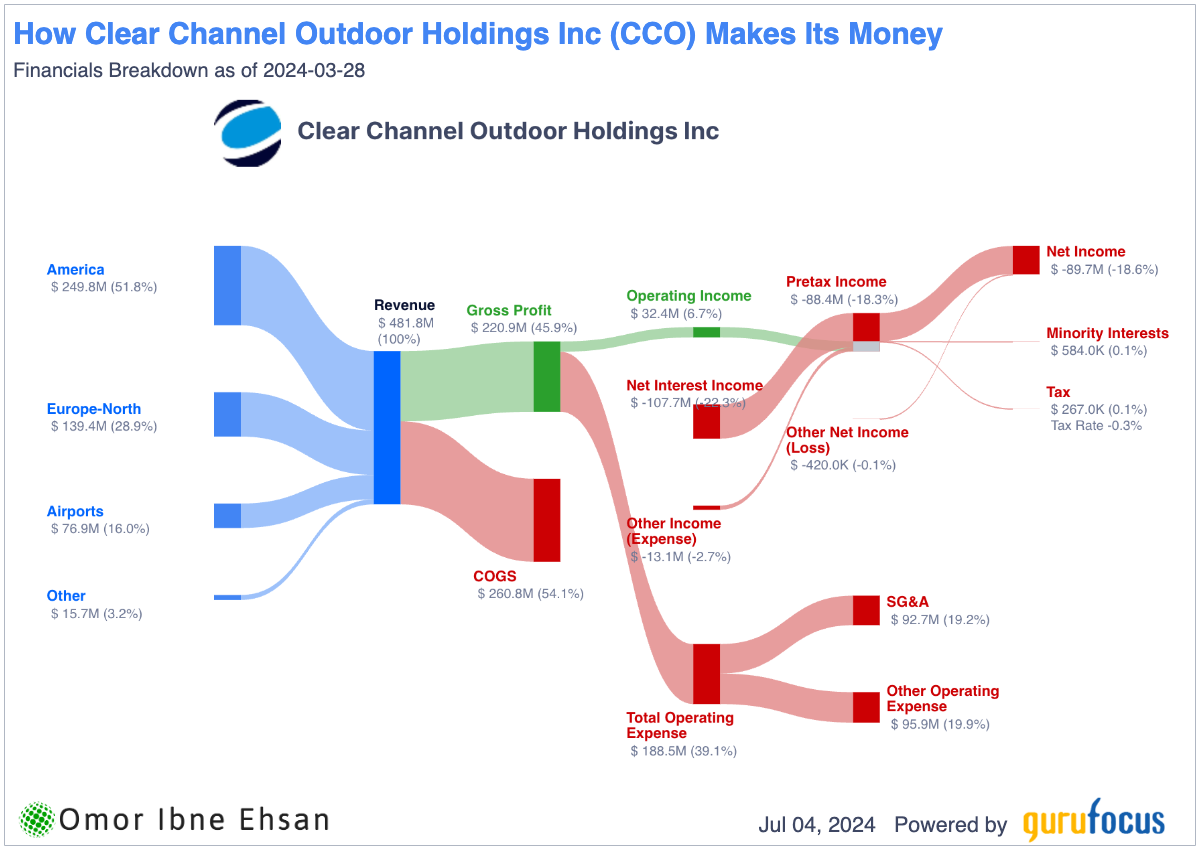

Clear Channel Outdoor (CCO)

Clear Channel Outdoor (NYSE:CCO) operates an outdoor advertising business. Its stock is a compelling long-term opportunity for investors willing to stomach some near-term volatility.

CCO posted revenue of $482 million, a 10.1% increase YOY. This was driven by record Q1 revenue in its America, Airports and Europe-North segments. Clear Channel Outdoor is benefiting from strong tailwinds in the out-of-home advertising market, particularly a surge in U.S. political ad spending ahead of the 2024 presidential election. Brand marketers and political media buyers are turning to billboards and street furniture to cut through the noise. CCO is well-positioned to capitalize on this with its massive nationwide footprint.

What really excites me is Clear Channel’s use of first-party data to enable precision-targeted omni-channel campaigns for advertisers. It can sync billboard exposure to mobile device IDs. I believe this should drive strong pricing power in the coming years.

In fact, analysts expect EPS could easily triple by 2026. A lot of the margin expansion is likely to come from debt servicing costs going down after rate cuts since this company sits on a $7.2 billion debt load.

Click to Enlarge

Finally, rate cuts bringing down those interest expenses will help earnings massively.

Urban-Gro (UGRO)

Urban-Gro (NASDAQ:UGRO) is a professional services firm that designs and builds cannabis cultivation facilities. UGRO stock has been one of the most volatile names in recent months. However, I believe it has significant upside potential going forward.

The company reported Q1 2024 revenue of $15.54 million, down 7.29% YOY but beating estimates by over $400,000. While Urban-Gro is still operating at a loss, those losses have narrowed substantially from $4.73 million in Q4 of 2023 to just $2.14 million this past quarter. At this trajectory, I expect them to reach cash flow neutrality in the near future.

More importantly, Urban-Gro seems poised for explosive top-line growth. Analysts are projecting 15% revenue growth this year, which will accelerate to 25% next year and a whopping 43% in 2026. If U.S. cannabis legalization gains traction, as hinted at by the U.S. Drug Enforcement Administration’s (DEA) recommendation to reschedule the drug, Urban-Gro’s growth could far exceed even these bullish forecasts. With over 1,000 cannabis projects under its belt, no firm is better positioned to capitalize on a legalization boom and the capex spree it would likely unleash.

Trading near trough valuations, UGRO stock looks like a coiled spring ready to catapult higher on any favorable regulatory catalysts. The potential to quintuple or more by 2026 appears very much on the table.

BARK (BARK)

Fifty-eight percent of millennials report they would prefer to have pets over human children. I am very bullish on the long-term prospects of pet-related companies. BARK (NYSE:BARK) is a leading provider of personalized dog products and services. The stock has been making a gradual comeback, rising 26% over the past year, despite the fading post-pandemic boom. So, BARK’s turnaround story could be just getting started.

While the lack of top-line growth has been a drag, analysts expect revenue to accelerate to nearly 10% next year and maintain a robust 13% annual growth rate going forward. If BARK can deliver on these projections and achieve profitability as anticipated, this overlooked penny stock may be poised to deliver multibagger returns.

The company’s gross margins improved by an impressive 600 basis points to 61.6% in fiscal year 2024, driven by enhancements in product quality and safety. In addition, shipping and fulfillment expenses decreased by nearly 300 basis points. This translated to $45 million in savings on approximately $500 million in revenue and adjusted EBITDA, proving by $47 million YOY. Looking ahead, the key will be BARK’s ability to sustain this momentum.

On Penny Stocks and Low-Volume Stocks: With only the rarest exceptions, InvestorPlace does not publish commentary about companies that have a market cap of less than $100 million or trade less than 100,000 shares each day. That’s because these “penny stocks” are frequently the playground for scam artists and market manipulators. If we ever do publish commentary on a low-volume stock that may be affected by our commentary, we demand that InvestorPlace.com’s writers disclose this fact and warn readers of the risks.

Read More: Penny Stocks — How to Profit Without Getting Scammed

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.