The market offers plenty of options, but only a select few have the potential to be true long-term winners. Not many people can look at a company and say that they have good enough conviction that the business in question will remain relevant a few decades from now. Even half a decade can completely change everything—as some can speak from personal experience.

Thus, it is important not to get “tunnel visioned” and keep your skin in the game. The means to an end matter. You should always be ready to sell if any of these companies become obsolete or face major stumbles in the coming decades. It pays to be flexible.

We’ll be looking at seven stocks that I personally think will be relevant in 20 or 30-plus years. Their historical records and market dominance give me peace of mind for the long haul. However, it’s equally important to focus on short-term growth. Remember, if you only wanted stability, you could park your money in bonds. We want our money to compound. Thus, each pick offers a blend of stability and growth and aims at nearer-term returns, too. Let’s take a look!

Intuitive Surgical (INTU)

Intuitive Surgical (NASDAQ:INTU) makes tools for robotic-assisted surgery and is riding high on the megatrends of minimally invasive procedures and an aging population. Q1 procedure volumes surged 16% year-over-year (YOY).

This company simply has a massive runway for expansion. With its current clearances, the company estimates it can reach around seven million patients annually, over three times its current patient base. New product launches like the da Vinci 5 in the U.S. and Europe should further fuel adoption.

Financially, Intuitive Surgical is firing on all cylinders. Its Q1 revenue jumped 11% to $1.89 billion, while GAAP net income soared 53% to $545 million. Analysts are bullish, too.

Sure, challenges exist, such as competition in China. However, with the stock up 32% year-to-date (YTD) and demographics in its favor, Intuitive Surgical’s best days are still ahead.

Costco (COST)

Costco (NASDAQ:COST) has been a standout performer in the stock market lately. The stock is up over 30% YTD. It has even been outshining Walmart (NYSE:WMT). Costco reported strong Q3 of fiscal year 2024 results, with revenue growing 9.1% to $57.39 billion and e-commerce sales jumping an impressive 20.7%. Net income surged nearly 30% to $1.68 billion. Same store sales growth has also started to pick up.

Click to Enlarge

Furthermore, analysts are bullish on the stock. Oppenheimer raised its price target to $950, citing Costco’s solid June sales driven by non-foods and its upcoming membership fee hike. Other firms like Baird, Loop Capital and Stifel also boosted their targets. The average 12-month analyst price target is now $910.05, implying an 8% upside.

Costco has consistently been gaining market share. It benefits from loyal members and a compelling value proposition. Nevertheless, Costco does lag behind its rivals in key growth areas like e-commerce and advertising. Thus, future gains may need to come more from earnings growth than valuation expansion. I’m still very bullish on the long run.

Linde (LIN)

Linde (NASDAQ:LIN) is a leading global industrial gases and engineering company that serves a wide range of industries. I believe Linde will remain one of the most consistent and stable stocks in the market going forward. The industrial gas sector has huge staying power, and Linde’s revenues and profits should stay sticky even as the white-collar world rapidly changes.

Several megatrends are providing tailwinds for Linde’s business, including the clean energy transition, digitization and the rise of advanced electronics manufacturing. Linde is investing heavily to capture growth from these trends, such as its recent $150 million investment to supply industrial gases to the world’s first large-scale green steel plant. Analysts are bullish on the stock, with an average price target of $489.31 (as of writing). That implies around an 11.7% upside.

Also, Linde delivered solid Q1 of 2024 results, with 6% operating profit growth. The stock has surged 115% in just the past five years. Thus, I’m optimistic Linde will continue its steady trajectory as a core industrial holding. Companies tied to long-standing industries with enduring demand rarely underperform.

Booz Allen Hamilton (BAH)

Booz Allen Hamilton (NYSE:BAH) provides management and technology consulting services to government agencies and corporations. BAH stock has climbed an impressive 136% over the past five years, and I believe it has room to run higher.

The company is deeply embedded with many federal agencies that are expanding operations as the geopolitical environment grows more complex. BAH’s expertise in areas like AI, cybersecurity and digital transformation aligns perfectly with the increasing technology needs of its government clients. I expect federal agencies will only become more reliant on the type of sophisticated solutions Booz Allen Hamilton delivers.

The firm posted Q1 earnings per share of $1.33 and revenue of $2.77 billion both topping expectations. While analyst opinions are mixed, the average price target of $168.78 points to further upside potential. I’m optimistic Booz Allen can sustain its impressive growth trajectory as it capitalizes on powerful tailwinds in the government services market. This is a high-quality company that looks poised to thrive for decades to come.

Walmart (WMT)

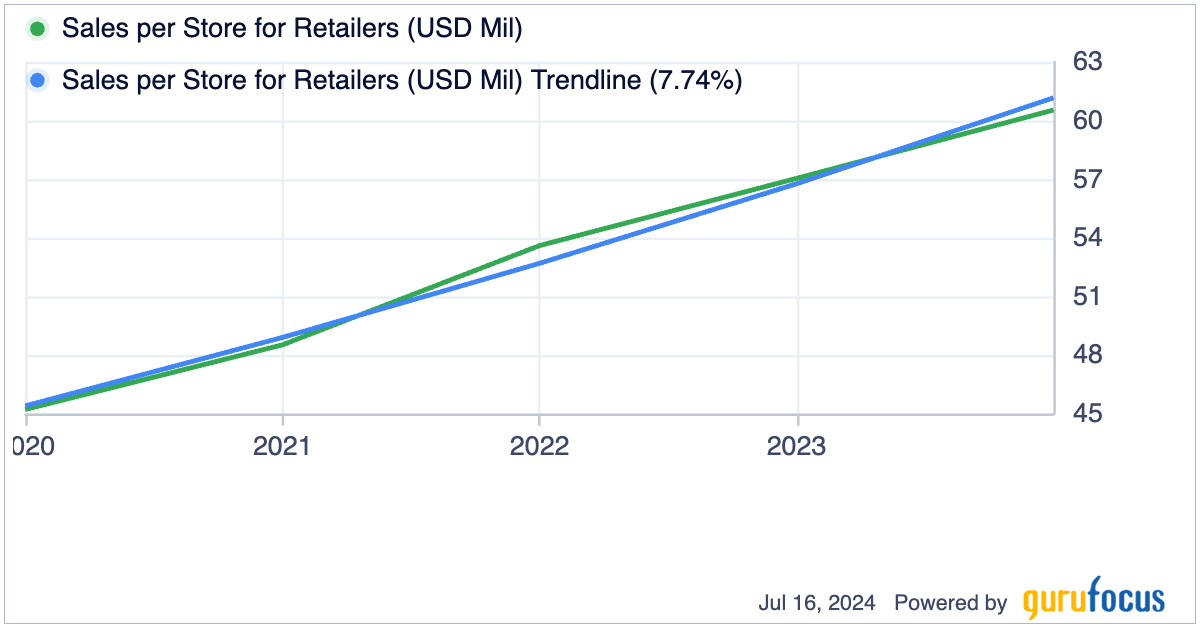

The world’s largest retailer of Walmart (NYSE:WMT) operates over 10,500 stores globally and generates over $600 billion in annual revenue. The company has been one of the best-performing retail stocks in 2024 so far, with shares jumping 29% in the first half of the year. Walmart crushed earnings expectations in Q1, with revenue growing 6% to $161.5 billion.

The company is rapidly automating its supply chain, which should massively increase profit margins in the coming years. In addition, Walmart is gaining grocery market share, growing e-commerce sales by 24%, and seeing huge tailwinds across the business. Per-store sales have naturally been booming, too.

Click to Enlarge

I’m confident this retail giant will continue to thrive for decades to come. While many retailers are struggling, Walmart looks poised to go from strength to strength. For patient investors, Walmart stock is a solid bet.

Amazon (AMZN)

Amazon (NASDAQ:AMZN) is the world’s leading e-commerce and cloud computing company. The company offers unparalleled exposure to two massive growth industries for decades to come. No other U.S. company can match Amazon’s e-commerce dominance.

Beyond retail, Amazon’s AWS cloud business gives it a stronghold in another critical sector. If artificial intelligence (AI) fulfills its immense promise, cloud providers like AWS stand to benefit enormously. Amazon is investing heavily to capitalize on the AI revolution. The company recently committed $230 million to expand its Generative AI Accelerator program for startups.

Amazon’s stock is up over 28.5% this year (as of writing) as investors recognize its leadership in e-commerce and cloud. Moreover, today and tomorrow’s Prime Days event could set new sales records, with JPMorgan analysts highlighting AI-powered shopping tools as a key driver.

Amazon’s financials are also robust, with $143 billion in Q1 revenue and 13% YOY growth. The company continues to innovate across its businesses while improving profitability. Amazon is uniquely positioned to ride multiple technological megatrends in the coming decades.

Microsoft (MSFT)

Microsoft (NASDAQ:MSFT) may be the single best bet on the software industry. This company has its hands on everything.

Windows remains hugely popular globally. Microsoft’s suite of productivity apps spans industries. Moreover, Microsoft deserves immense credit for making the AI breakthrough a reality through its massive early investments in OpenAI.

Those investments are now paying off handsomely. OpenAI is using Microsoft’s Azure cloud to power its AI systems. Additionally, Microsoft will receive a substantial share of OpenAI’s future profits. And, the company maintains significant influence over OpenAI’s direction.

In Q3 of 2024, revenue grew 17% YOY to $61.9 billion. Azure cloud revenue surged 31%. Cloud adoption is accelerating across industries. And of course, AI integration is driving increased demand for Microsoft’s products and services.

Few companies are as well-positioned to capitalize on the most important technology trends shaping our future.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.