Welcome to Smart Money! My name is Eric Fry, and I’m glad you’re here.

Wall Street has sold investors on the idea that they should start with “micro” analysis – the idea that they should make investment decisions by comparing things like price/earnings ratios, income statements, or other company details.

But I do the opposite; I start with “macro” analysis.

I look for big-picture trends that drive huge, multiyear moves in entire sectors of the market.

I’m talking about trends that can spin off dozens of triple- and even quadruple-digit gains in just a few years.

Catching just one of these trends – at the right time – can help anyone accumulate enough capital to finance their dreams and to provide themselves with an enviable retirement…

When investors use a global macro strategy, they identify investment opportunities from a broad, global, top-down perspective, rather than by examining stocks one by one (a micro, bottom-up perspective).

And today, I want to highlight my Top 7 Stocks for 2024, each of which capitalizes on a powerful megatrend.

Let’s get started…

2024 Stock No. 1: Corning

For more than 170 years, the Corning Inc. (GLW) name has been synonymous with best-of-breed glass products. It has continuously innovated and set the industry standard for excellence.

Today, the company operates six different business segments – each of which is beginning to benefit from powerful tailwinds.

Those six segments are…

- Optical Communications – accounting for 34% of Corning’s 2022 sales and 37% of its net income.

- Display Technologies – accounting for 22% of sales and 44% of net income.

- Specialty Materials – accounting for 14% of sales and 19% of net income.

- Environmental Technologies – accounting for 11% of sales and 16% of net income.

- Life Sciences – accounting for 8% of sales and 9% of net income.

- Hemlock and Emerging Growth Businesses – accounting for 11% of sales and 2% of net income.

The worldwide 5G buildout tops the list of tailwinds that are benefiting Corning’s largest segment, Optical Communications. That’s the one that provides optical fiber and related connectivity solutions to telcos, data centers, and other enterprises.

As the global 5G build-out proceeds, so too will demand for Corning’s fiber-optic cable and components. This substantial source of new demand could become shockingly large.

Looking further down the road, I expect the coming decade to reward Corning with a level of profitability that few investors anticipate today. As a small bonus, the stock pays an annual dividend yield of 4.2%.

Let’s give the final word to Corning CEO Wendell Weeks…

When it comes to the critical components that enable high technology systems in multiple markets that we serve, the bar just keeps getting higher. This leads to a world where precision glass and ceramics win, and we have been winning…

Corning is one of the world’s most proficient innovators in materials science. We combine our unparalleled expertise in glass science, ceramic science, and optical physics with our proprietary manufacturing and engineering platforms to develop category-defining products that transform industries and enhance lives.

2024 Stock No. 2: Intel

According to an oft-repeated corporate mantra, “Offshore production is cheaper than made-in-America.” That assertion seemed so obvious for so many decades that almost no one ever dared to question it.

But today, that ancient corporate mantra seems much less obvious… or even true. In fact, it is close to joining the catalog of American folklore, alongside Paul Bunyan and his blue ox, Babe.

To be sure, some forms of offshore production are cheaper than domestic alternatives, but many are not… especially after including the intangible cost of unreliability.

As the COVID pandemic started blowing apart global supply chains, American corporations learned that there is nothing cheap about not knowing if critical production inputs will arrive on time. Broken supply chains can cause crippling production delays, multibillion-dollar losses, and/or lost market share.

The era of unfettered globalization is over… and is now reversing course toward something less global.

In 2022, a UBS survey questioned U.S. manufacturing executives about their future production plans. More than 90% of the respondents said they either were in the process of moving production out of China or had plans to do so; about 80% said they were considering bringing some portion of it back to the U.S.

Researchers from Bloomberg attempted to analyze this deglobalization trend by tabulating the number of times buzzwords like “onshoring,” “reshoring,” or “nearshoring” appear in corporate earnings calls or conference presentations.

According to the researchers’ calculations, these deglobalization buzzwords are appearing 10 times more frequently now than they were before the pandemic.

Intel Corp. (INTC) is leading this new megatrend – and attracting a lot of scorn and ridicule from investors in the process. The company has committed to a multiyear, multibillion-dollar plan to build new semiconductor fabrication facilities (known as fabs) in the U.S.

Already, Intel has broken ground on two new factories in Arizona. The $20 billion plants – dubbed Fab 52 and Fab 62 – will bring the total number of Intel factories at its campus in Chandler, Arizona, to six.

Meanwhile, the chipmaking giant is spending an additional $20 billion to establish a “Silicon Heartland” by building a massive new fab in Licking County, Ohio.

According to Dodge Construction Network, construction of new manufacturing facilities in the U.S. has soared 116% over the past year – far outpacing the 10% increase on all building projects combined.

But Intel is not simply “onshoring.” The chipmaker is onshoring capabilities that could become absolutely essential in the years ahead.

Consider, for example, the hottest new technological buzzword: artificial intelligence, or AI.

Because of the recent release of ChatGPT, an AI-powered “chatbot” that can do everything from answering questions to writing essays, AI-focused investing has become the newest Wall Street sensation.

But that’s much easier said than done. AI is not a tangible product like an automobile or a TV set, so it is difficult to invest in AI directly. However, as we peel away at this onion, we find that a handful of semiconductor companies might offer an indirect play on AI.

Names like IBM, NVIDIA, and, yes, Intel top the ranks of AI-chip producers. In fact, in 2017, Intel became the first semiconductor company in the world to generate more than $1 billion in sales from AI chips. (Importantly, Intel is the only company of these three that continues to operate fabs – and plans to invest tens of billions building next-generation ones here in the United States.)

IBM and NVIDIA design chips here at home, and then outsource the actual production to overseas companies like TSMC and Samsung.

But that paradigm may be ending quickly – and Intel could be a big player in this megatrend.

2024 Stock No. 3: Alcoa

Because of widespread anxiety about the near-term risk of recession, many “battery metal” stocks have plummeted 50% or more.

Therefore, at their current depressed valuations, some of these stocks are pricing in so much doom that they fail to reflect any of the long-term boom for battery metals.

One of those stocks is Alcoa Corp. (AA), the largest U.S.-based aluminum producer.

Aluminum does not receive the same high-profile attention that other battery metals do, but the solar industry is a prodigious consumer of aluminum, and so is the EV industry.

Certainly, Alcoa’s stock might fall further. But the current valuation is cheap enough that the stock could deliver outsized gains over the next several months, especially if aluminum demand ramps up more quickly and powerfully than recession-phobic investors currently expect.

Plus, the stock might also catch a boost if the White House enacts a ban on Russian aluminum. That story surfaced in early February 2023.

Trends in the aluminum market are similar to trends in the copper market, which is good news for Alcoa, based in Pittsburgh.

But first the bad news…

After spiking to $4,000 a tonne during the early days of the Ukrainian invasion, the aluminum price tumbled about 40%, which caused Alcoa’s share price to drop as much as 65%.

Incessant chatter about recession and demand destruction is weighing on the price of aluminum. But as with copper, the long-term outlook for the silvery metal is excellent.

A new report from the London-based International Aluminium Institute (IAI) finds that global aluminum demand will jump about 40% by 2030 – and cleantech industries will power most of that growth.

As a result, the report states that aluminum producers will need to ramp up their production from 86 million metric tons in 2020 to 120 metric tons by 2030.

According to the research firm, Wood Mackenzie, solar industry demand for aluminum could increase from just under 3% of total world consumption to nearly 13% by 2040.

In the EV industry, aluminum does not play a significant electrification role, but the body and chassis of each Tesla Model S contains about 410 pounds of aluminum!

That’s no accident. Because aluminum is so much lighter than steel, EV manufacturers covet the metal. An aluminum vehicle can travel much farther on a single charge than a steel vehicle can.

For this reason, many EV manufacturers are ramping up their aluminum consumption. In fact, aluminum is the fastest-growing material in the automotive market.

In 2021, the auto industry accounted for about 20% of global aluminum demand. Within that slice of the pie, the EV portion was only about 2%.

But that percentage is certain to grow rapidly over the coming decade. Wood Mackenzie expects aluminum demand for EVs to hit 2.4 million tonnes by 2025, and then quadruple to nearly 10 million tonnes by 2040. At that point, EV demand for aluminum would total about 12% of the global total.

Obviously, these forecasts are merely guesses, but the trend is clear. EV demand for aluminum is ramping higher. And that’s just one source of demand from the cleantech sector.

According to the IAI, renewable energy needs will create demand for aluminum to replace existing copper cabling for power distribution. In total, the electric sector will require an additional 5.2 million metric tons by 2030, according to the group.

You get the idea.

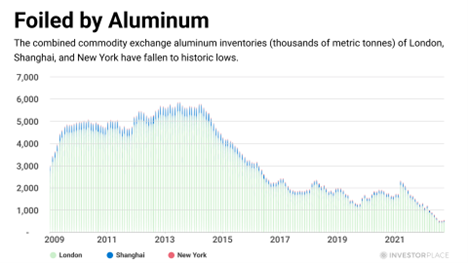

Interestingly, despite all the talk about slack demand for aluminum, global stockpiles of the metal are near historic lows… just like they are in the copper market!

The combined aluminum inventories of the major commodity exchanges in London, Shanghai, and New York have fallen to their lowest levels in more than 20 years.

But despite the strong supply-demand dynamics in the aluminum market, the Alcoa share price is reflecting all doom and no boom. The stock changes hands for less than four times earnings.

From this low valuation, Alcoa offers substantial upside potential – both over the next few months and over the next few years.

2024 Stock No. 4: Mosaic

I am bullish on the fertilizer industry in general and The Mosaic Co. (MOS) in particular, which is one of the largest U.S.-based fertilizer companies. I expect the company to capitalize on resurgent demand growth for potash and phosphate fertilizer.

The “Big 3” types of fertilizer are nitrogen, phosphate, and potassium (potash). The latter two of these crop nutrients produce about 85% of Mosaic’s revenues.

The prices for both phosphate and potassium fertilizers are far above their 10-year average levels. And yet, Mosaic’s share price has dropped more than 30% since last spring.

Recession fears are to blame…mostly.

Let’s dig into the story.

High As an Elephant’s Eye

As I mentioned above, nutrients are not Nikes.

Yet the stock market is hammering the purveyors of both footwear and fertilizer as if they were joined at the hip.

During the past six months, Nike stock has slumped 31%, while Mosaic shares have dropped an identical 31%.

Nike might still be a “sell,” but I’m ringing the “buy” bell on Mosaic.

Fertilizer demand has slackened somewhat from peak levels, but it remains fairly elevated, as pricing levels clearly indicate.

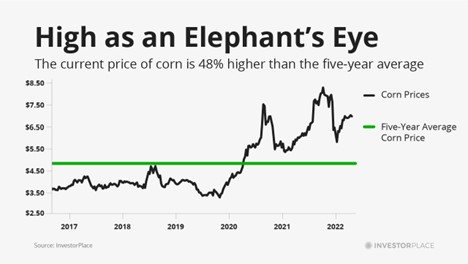

For example, even though diammonium phosphate prices have slumped 27% from their May peak, they remain about 70% above their five-year average.

Similarly, the benchmark Brazil Potash CFR Granular price is down 50% from the peak it hit last May. Nevertheless, at $600 per metric tonne, the current price is still 32% above the average price of the last five years.

But instead of focusing on these historically high fertilizer prices, many investors seem to be fretting about the recent price drops. Certainly, fertilizer prices could continue tumbling from their peak, but that’s unlikely.

Fertilizer prices spiked last spring because of Western sanctions against both Belarus and Russia. Together, these two countries produce about 30% of the world’s potash supply and about 20% of all fertilizer exports.

In the U.S., for example, Russia supplies about 6% of total potash imports and 20% of diammonium phosphate imports.

Therefore, when this massive supply “disappeared” from Western supply chains, fertilizer prices skyrocketed. Since then, however, prices have “normalized” to some extent. The recent price declines simply reversed part of the springtime price spike.

But the sanctions against Belarus and Russia remain in place, which should put a floor under prices. As farmers acclimate themselves to the “new normal” and resume buying, fertilizer prices should stabilize, if not move higher once again.

But what about demand destruction? Won’t high fertilizer prices curtail demand somewhat? Maybe, but we must remember that crop prices are also well above long-term average levels.

Relative to their five-year average prices…

- Wheat is 37% higher…

- Corn is 42% higher…

- Sugar is 29% higher…

- And soybeans are 29% higher.

Because the prices for these crops are well above their five-year average levels, farmers have ample incentive to “pay up” for the nutrients they need to maximize their crop yields.

Full Steam Ahead

On the other side of the equation, the current phosphate and potash prices are high enough for Mosaic to produce sizeable profits.

In fact, earlier this week, Mosaic reported a 126% year-over-year jump in third-quarter profits.

Even though that result came in below analyst expectations, it did not dim the company’s strong profit outlook.

As Mosaic CEO Joc O’Rourke remarked on this week’s conference call…

Food security remains a concern around the world. Global grain and oilseed stock-to-use ratios remain at 20-year lows and early data continues to suggest there may be further downside to total production once the fall harvest is complete… We’re seeing food security issues play out in other crops as well. Staples like rice are also seeing significant production shortages… Because of this, we see a tight market for global grains and oilseeds continuing into 2023 and beyond.

[Meanwhile], the global fertilizer market remains tight with supply constraints in both potash and phosphates still unresolved… Global channel inventories of phosphate and potash remain below historic norms… But prices have retreated back to levels low enough to entice growers to step back into the market…

To summarize, the strength of crop prices and more affordable fertilizer prices suggest nutrient demand will recover from the summer low we experienced during the third quarter. Given the constructive agriculture backdrop, we believe our business is well-positioned to benefit.

The Wall Street community of analysts seems to agree with that assessment. It expects the company to post earnings per share of more than $10 next year. At that level of profitability, Mosaic is trading for less than five times earnings.

Looking farther down the road, most fertilizer industry observers anticipate strong long-term demand for all crop nutrients, especially phosphate and potash.

BHP expects global potash demand to double over the next two decades. Similarly, Grand View Research predicts global phosphate demand will triple over the next two decades.

The relentless need to feed a hungry planet will power these demand trends. Additionally, basic botany will play a key role.

Potassium is essential for optimizing plant health. Potassium-deficient soil produces a range of undesirable effects, like low-quality, low-yielding plants that utilize water less efficiently and are more susceptible to pest and disease damage.

Additionally, many crops remove large amounts of potassium from the soil. For example, harvesting an average crop of…

- Alfalfa removes about 450 pounds of potassium per acre…

- Potatoes remove about 500 pounds of potassium per acre…

- Tomatoes remove about 500 pounds of potassium per acre…

- And sugarcane removes about 350 pounds of potassium per acre.

Therefore, in order to maintain the viability of their fields, farmers must replace at least some of the lost potassium.

Bottom line: The outlook for fertilizer demand, both near-term and long-term, supports a bullish outlook for fertilizer pricing… and bodes well for companies like Mosaic.

2024 Stock No. 5: GE Healthcare

In 1979, General Electric introduced its famous tagline, “We bring good things to life.”

One of the things this iconic American company brought to life was its stock price, which soared more than 10,000% from the end of 1979 to its peak in 2000.

But shortly after that peak, the lights started flickering at GE, and its share price slumped for nearly two decades. Between 2000 and 2018, GE stock produced an abysmal 80% loss – leading to its ignominious eviction from the Dow Jones Industrial Average.

Enter Larry Culp, who became CEO in October 2018. The widely respected and heavily compensated CEO accepted the daunting task of reversing GE’s long-term decline.

Nearly five years into the mission, Culp cannot yet claim victory. But GE’s revenues are on the rise, and more importantly, its annual net income just reached a six-year high.

To spearhead GE’s turnaround, Culp proposed a major restructuring two years ago that would split the company into three distinct entities – each of which would become standalone publicly traded companies.

That action plan took its first of three giant steps forward last January when GE spun out its healthcare operations as GE HealthCare Technologies Inc. (GEHC).

The next step will combine GE Renewable Energy, GE Power, and GE Digital into a new operation called GE Vernova – which GE plans to spin out as a new standalone entity in 2024.

For the final step, the remaining third of GE will become GE Aerospace and will also trade in the stock market as a standalone company.

Obviously, shuffling divisions around and giving them new names does not necessarily create any additional value for shareholders. But the new GE HealthCare spinoff possesses some compelling investment attributes.

The Next Step for Healthcare

GE HealthCare is interesting – both for what it is already and what it could become.

As one of the oldest “new” healthcare stocks in the market, GE Healthcare is a blue-chip company with a formidable presence in the medical imaging industry.

The company operates in more than 160 countries. It sells medical equipment like CT scans, MRIs, X-rays, and ultrasound machines. It also sells service contracts on those machines.

GE HealthCare’s installed base of four million medical machines and devices serves more than one billion patients per year. The company conducts its operations through four main business divisions…

- Imaging…

- Ultrasound…

- Patient Care Solutions…

- And Pharmaceutical Diagnostics.

During the first quarter of the year, all four divisions produced double-digit revenue growth (on a constant currency basis) and are on track to deliver high single-digit growth for many years to come.

The company is a leader in the field of AI-enabled medical devices. Of the more than 500 devices included by the U.S. Food and Drug Administration on a recently updated list of AI-enabled device authorizations, 42 are from GE HealthCare. That achievement places the company on the top of the heap. Siemens Healthineers is No. 2 on the list with 29.

From an investment perspective, therefore, GE HealthCare is a two-part story. It is a solid, steadily growing medical imaging company that also includes considerable fast-growth potential from its AI product line and investments.

According to Grand View Research, artificial intelligence will become a key driver of medical device innovation over the coming decade. The research firm predicts the AI component of the healthcare market will skyrocket from $15.4 billion in annual sales last year to more than $200 billion in 2030. That’s a compound annual growth rate of 37.5%.

To support its robust forecast, Grand View explains…

Artificial intelligence and machine learning algorithms are being widely adopted and integrated into healthcare systems to accurately predict diseases in their early stage based on historical health datasets…

Healthcare functions such as diagnostics, patient management, medication management, claims management, workflow management, integration of machines, and cybersecurity saw a remarkable surge in the integration of AI/ML technologies.

Importantly, GEHC’s AI solutions do not replace medical professionals; they assist them. The company’s AI-enabled devices and services operate alongside traditional medical practitioners to support and optimize their efforts.

As Vignesh Shetty, a Senior Vice President at GE Healthcare, explains…

GE Healthcare’s digital strategy is to look at AI to help clinicians achieve clinical and operational outcomes that create maximum impact for patients, providers, and health systems… AI is an incredible lever to tackle problems at a speed and scale that our providers are coming to expect, to help save lives and improve outcomes for millions of patients everywhere.

GEHC is embracing this new paradigm with gusto.

2024 Stock No. 6: PayPal

PayPal Holdings Inc. (PYPL) is a titan of the digital payments industry.

The company traces its history to the year 2000, when Elon Musk merged his online bank, X.com, with Peter Thiel’s software company, Confinity, to form PayPal. The merged entity started spinning gold almost immediately for Musk and Thiel, as the inventive pair sold the company to eBay just two years later for $1.5 billion.

Then in 2015, eBay spun out PayPal as a separately traded company, which it has remained ever since. (Interestingly, 2015 was also the year that Musk and Thiel partnered up again to form OpenAI, the company that would go on to create the AI sensation, ChatGPT.)

During the last five years, the tally of active accounts on PayPal’s platform has swelled 63% to 435 million, while the annual volume of processed payments on its platform has doubled to a whopping $1.37 trillion.

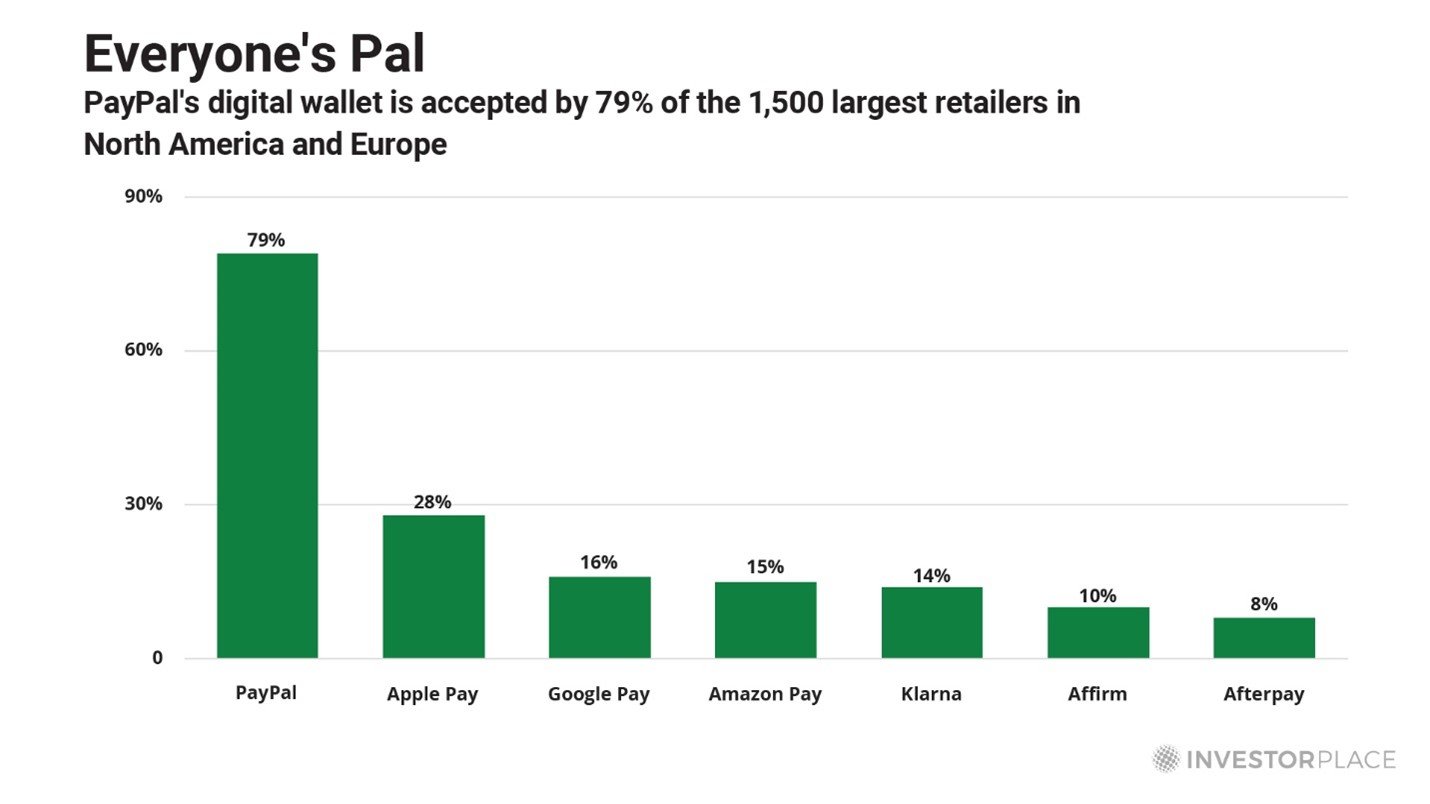

PayPal’s dominant position in the “branded checkout” segment has powered most of that growth. The “PayPal/Venmo” checkout button you might see when shopping online is an example of that business. 80% of the top 1,500 retailers in North America and Europe feature PayPal in their digital wallets – which is nearly three times more than the No. 2 player, Apple Pay.

But PayPal is not taking its success for granted. The company is fortifying its market leadership by integrating leading-edge AI and machine-learning processes into key aspects of its operations. For example, the company uses AI to detect fraudulent transactions and to boost the approval rate of valid transactions.

But despite the company’s formidable competitive position and superior growth prospects, the stock took a hit last May when the quarterly earnings report disappointed Wall Street analysts.

However, I believe this short-term selloff is providing an excellent opportunity to purchase a leader in the financial technology world…

Buy Now, Pay Later

PayPal’s growth strategy relies on three key initiatives…

- Strengthening its core “branded checkout” solution…

- Growing its “unbranded checkout” solution…

- And developing and integrating AI processes that increase merchant sales, boost customer “stickiness,” and/or reduce operating expenses.

Branded Checkout is the foundation of PayPal’s business because of its high-margin fee structure. This business segment accounts for about one-third of the Total Payment Volumes (TPVs) the company processes, but it produces more than half of its total revenues.

PayPal is the market leader in branded online checkout with 35 million merchants on that platform. Although the company does not possess the commanding 99% merchant acceptance rate of legacy credit card companies like American Express and Mastercard, it has the largest acceptance rate of any “alternative payment method” (APM) provider. This category of payment solutions includes direct debit transactions, prepaid debit cards, and eWallets like PayPal, Venmo, Google Pay, and Apple Pay.

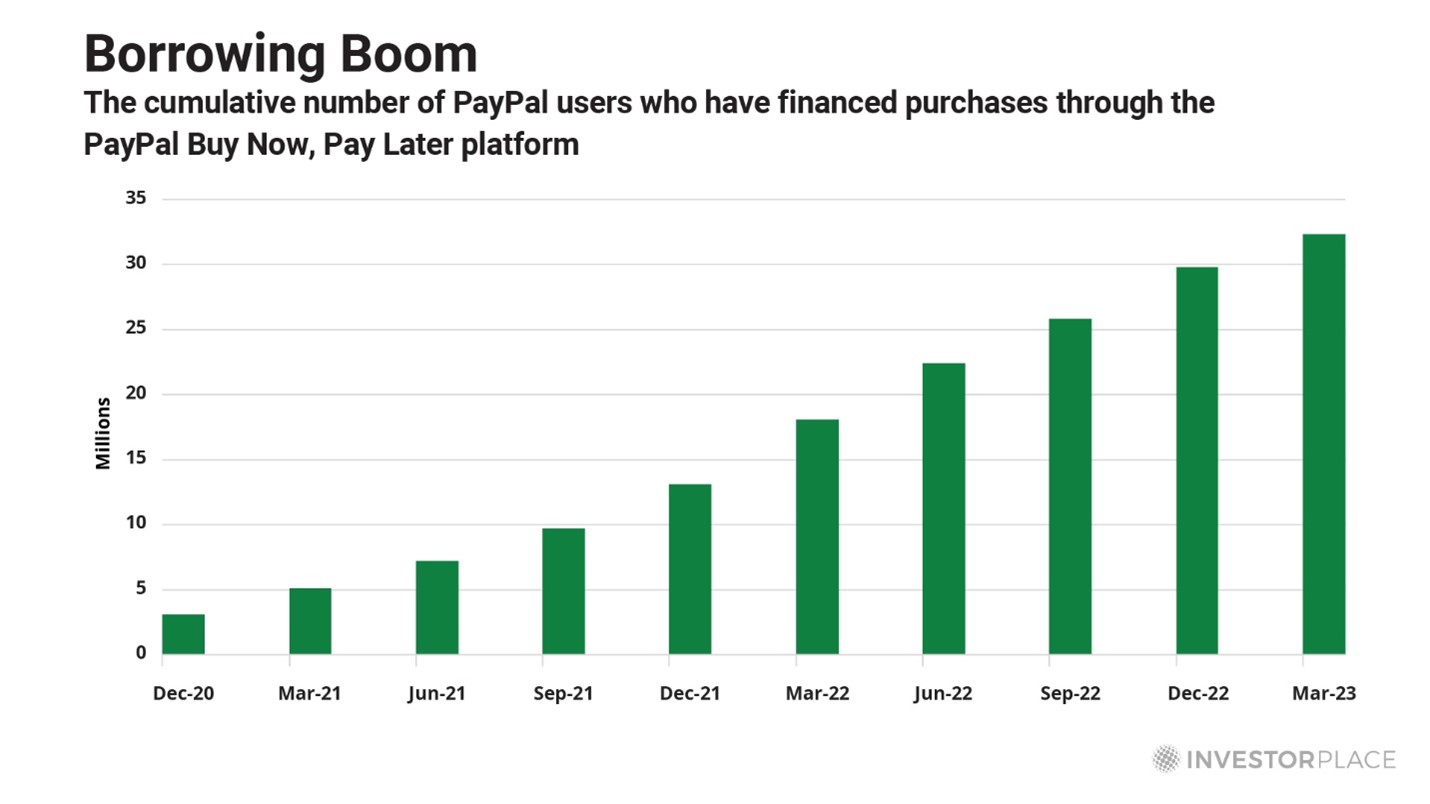

Three years ago, PayPal launched a new “Buy Now, Pay Later” (BNPL) feature to bolster the appeal of its branded checkout offering.

This credit facility is similar to what established BNPL players like Klarna, Afterpay, and Affirm offer an immediate opportunity for shoppers to finance an online or in-store purchase at the point of sale.

Despite the brief operating history of PayPal’s BNPL offering, it has made rapid strides. Since launching BNPL in 2020, PayPal has issued loans to nearly 30 million customers. In 2022 alone, PayPal processed more than $20 billion of BNPL loans – up 160% from the prior year.

Thanks to that rapid growth, PayPal’s 13% market share in the U.S. is nearly identical to that of the No. 1 player, Afterpay. PayPal’s momentum in this market should propel it to undisputed leadership by next year… and that’s no small matter in a sector that is growing as rapidly as BNPL consumerism.

According to GlobalData.com, the global BNPL market size will top $309 billion this year – up more than 150% during the last two years. BNPL-financed transactions now account for about 4% of all online purchases worldwide – up from less than 1% four years ago.

Importantly, this category of transaction delivers an outsized benefit to merchants. PayPal customers who adopt BNPL solutions spend 30% more through PayPal than those who do not.

As PayPal attempts to expand its presence in the BNPL market, it will benefit from one major competitive advantage. The company has preexisting relationships with a huge swathe of the target market – both the merchants and the individual consumers.

Unlike its competitors, which must win new business to establish a BNPL relationship with a merchant, PayPal can deliver BNPL capabilities as a “bolt-on” to an existing relationship.

PayPal simply incorporates BNPL functionality into the existing checkout protocol. It is not a “new sale.” For example, earlier this year, PayPal added BNPL capabilities to its existing relationship with Microsoft. Online shoppers at Microsoft’s Xbox Store can now access BNPL if they wish.

As CEO Dan Schulman explained recently…

Buy Now Pay Later continues to provide meaningful value to both our consumers and merchants. Over 32 million consumers have used our Buy Now Pay Later service since inception, at nearly 3 million merchants. We are now one of the most popular Buy Now, Pay Later services in the world… growing at 70% [year-over-year] on a currency-neutral basis.

Prudently, PayPal is working to “externalize” these loans by selling them to a third party, rather than retaining them on their own balance sheet. By selling the loans, PayPal removes the risk of holding bad loans.

The company took a giant step forward toward achieving that goal last month when it struck a deal to sell up to €40 billion of BNPL loans to the global investment firm KKR.

Under the terms of the agreement, KKR will acquire PayPal’s existing European BNPL portfolio, along with future originations of eligible BNPL loans. PayPal will continue to conduct all the customer-facing activities of the loans, including underwriting and servicing.

This major transaction not only removes a large dollop of credit risk from PayPal’s balance sheet, but it also frees up capital to accelerate BNPL originations in Europe and/or to conduct shareholder-friendly activities like buying back stock.

PayPal expects to generate about $1.8 billion in net proceeds from this transaction and states that it will use a portion of the proceeds to boost its 2023 share repurchase program to $5 billion. Last year, the company repurchased $4 billion in stock, which reduced the share count by about 3%.

Paving the Way

In addition to fortifying its leadership position in branded checkout, PayPal is expanding in the rapidly growing Unbranded Checkout segment. The company boosted its unbranded business by 30% last year – lifting this sector’s contribution to total revenues to 28%.

The company refers to this solution as the PayPal Complete Payments (PPCP) platform, and it opens the door to a vast, new opportunity. Because this solution primarily serves small to mid-sized businesses, the total market opportunity is enormous. PayPal estimates the Total Addressable Market (TAM) to be roughly $750 billion.

The PPCP platform enables small businesses to accept credit cards and digital wallets as well as a range of Venmo and PayPal services. In April, PayPal gave this platform a major upgrade by adding Apple Pay to it.

That means that small businesses using PayPal as the backend for their payment processing can now accept Apple Pay alongside various other popular payment options.

Additionally, PayPal merchants can use their iPhone as a mobile point of sale terminal without the need for a dongle or other accessory device. Apple launched the technology in February.

CEO Schulman says that growing the unbranded checkout business has become a “strategic imperative” for PayPal – not just because it adds incremental revenue but also because it broadens and deepens customer relationships.

These expanded relationships produce vast troves of data that can fuel future AI enhancements.

2024 Stock No. 7: Equinor ASA

Equinor ASA (EQNR) is the largest energy company in Norway and the ninth largest in the world, based on revenue. It is Europe’s largest supplier of natural gas and also a major crude oil producer.

The fact that this company operates next door to Russia used to be a footnote that barely deserved a mention. But that footnote became a headline after Russia invaded Ukraine.

At that time, Russia supplied about 40% of the natural gas Europe consumed every year. Norway was a distant No. 2 – providing 20% to 25% of Europe’s natural gas needs.

But as Europeans countries have been phasing out Russian supplies of oil & gas, they have been phasing in additional supplies from Norway. As of April this year, Norway provides about 30% of Europe’s gas, while Russia provides just 13%.

Equinor benefits directly from this shift. Last year, Equinor boosted its natural gas production by 5% to a record-high 729 million barrels of oil equivalent (boe).

Looking at recent financial results, Equinor is an enormously profitable company. In 2023, it produced gross earnings (EBITDA) of $45.1 billion, along with free cash flow of $13.8 billion.

On a per-share basis, the company earned $3.50, and could earn even more in 2024, if oil prices continue ratcheting higher.

These robust results could be a taste of things to come. The company’s strong pipeline of development projects that will come on stream by 2030 will deliver around 6.5 billion barrels of oil equivalent (boe), at a breakeven level of $35 per barrel, while also producing a rapid average “payback” on investment of just two and a half years.

In keeping with that disciplined approach, Equinor recovered its investment in the recent Troll Phase III expansion in less than a year.

Additionally, the company has a long history of replacing reserves through disciplined exploration activities. During the last three years, Equinor achieved an average reserve-replacement ratio of 107%, In other words, it ended each year with 7% more reserves than when the year began. That’s an excellent record for a company of Equinor’s size.

Thanks to the ample cash flow coursing through Equinor’s income statement, the company has made significant progress on the debt front and is now debt-free. In fact, its balance sheet boasts more than $8 billion in net cash.

That impressive achievement has enabled Equinor to boost its dividend payouts and ramp up its stock-repurchase program. During the past around 12 months, Equinor stock paid a hefty 13.4% yield, thanks to a combination of regular and special dividends. The dividend yield in 2024 will not hit that lofty level, but it should remain above 5%.

All good news… and the good news seems very likely to continue throughout 2024.

Equinor is an outstanding buy.

Moving Forward

I’m so glad that you decided to further your journey to wealth by joining Smart Money.

While these five stocks are sure to fortify your portfolio in 2023 and beyond, those aren’t the only benefits of this free e-letter…

Nearly every Tuesday, Thursday, and Saturday, you’ll receive an email from me or my Editor, Dave Gilbert, wherein we’ll share insights on the latest market “megatrends,” how to hedge against inflation, which stocks you should avoid, and more.

Get started by visiting your Smart Money website here.

Regards,

Eric Fry