Are shares of Celgene Corporation (NASDAQ:CELG) finally bottoming? Without news flow for the stock to react on, it’s hard to confirm whether the peak-to-trough drop of 49.6% in CELG stock is over or if more losses are still to come. Still, the recent action surely has some investors hopeful that the beatdown in Celgene is over.

Even if more lows are on the way, is CELG stock compelling enough for investors to start a new position?

Celgene is far from perfect. That’s fairly evident by the fact that CELG stock has been absolutely pulverized over the last eight months. However, the company isn’t languishing through a period of little to no growth. In fact, despite its missteps, Celgene actually has pretty good growth.

Of course there are concerns about future growth, drug pricing and management’s recent sloppiness. I would be amiss to leave those factors out. But the truth is Celgene continues to make in-demand treatments and is a leading biotech company. With that in mind, should we buy the stock?

Valuing CELG Stock

CELG stock trades at a very respectable 9.3 times this year’s earnings. On 2019 estimates, Celgene trades at just 7.7 times earnings. There is a very large disconnect here vs. what the stock should be trading for. For instance, consider the growth.

Analysts expect Celgene to grow sales 15% this year and another 12% in 2019. That’s good, but not as good as its earnings estimates. Forecasts call for 14.5% growth this year and an acceleration to 20% growth in 2019.

Cash flows have been under pressure somewhat due to recent acquisitions. But overall, the company is generating plenty of money. Last quarter, management dumped a bunch of good news on investors. Not including the impact/dilution from its Juno acquisition, Celgene raised its full-year sales guidance from a range of $14.4 billion to $14.8 billion, to the top end, now expecting $14.8 billion in total sales.

When accounting for dilution, the Juno deal will obviously impact operating margins — from 45% down to 38% — and earnings — down from $7.36 to $6.31 on a generally accepted accounting principles (GAAP) basis. Granted, this isn’t great, but it still shows that Celgene is doing well and that its valuation is somewhat unreasonable down here in the single digits.

If investors aren’t using the Juno-impacted GAAP earnings results, it still leaves CELG stock at just 12.5 times this year’s earnings.

Finally, its main revenue-driving drug in Revlimid didn’t see its revenue estimates cut. In fact, management now expects $9.5 billion in sales this year vs its prior guide of $9.4 billion. It also gave a slight boost to Pomalyst/Imnovid, from $1.9 billion up to $2 billion for the year.

As we said, CELG stock isn’t perfect, but it’s far from a disgrace.

Trading CELG Stock

Click to Enlarge

Above is a weekly five-year chart and below is a daily one-year chart. On the long-term one, you can see where CELG stock broke below two significant price levels, one at $95 and the other at $85. It was bad enough for shares to fall from $145 to $85 in such a short span. But for it to break below this level was even worse.

Bulls and bears alike need to watch this level now. Should CELG stock break over $85, the tides may shift back into the bulls’ favor. If this level becomes resistance and Celgene is unable to get back above it, new lows are not necessarily off the table.

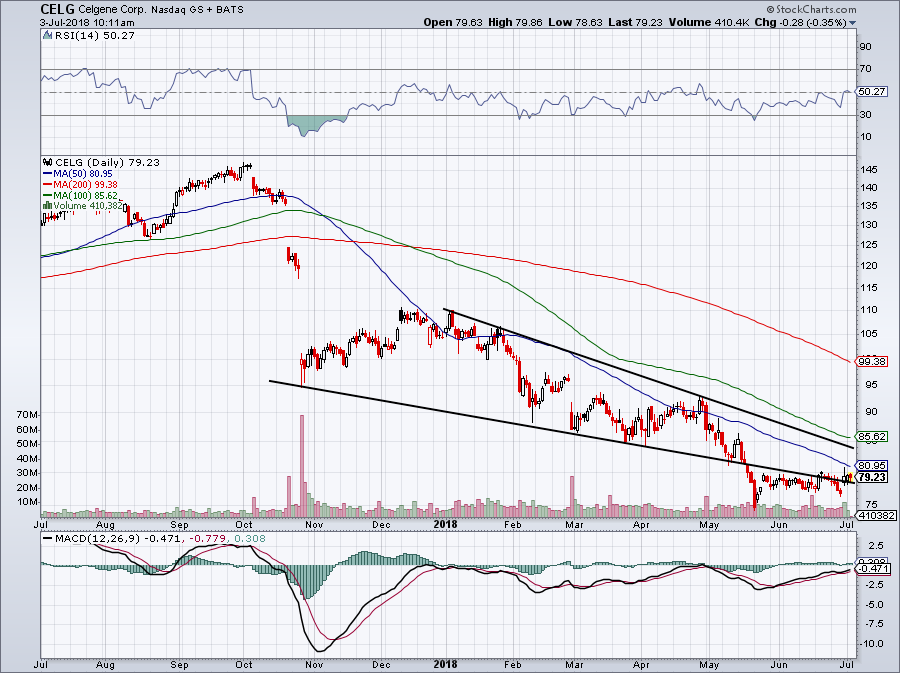

Click to Enlarge

Now on the short-term chart, we can see some of the more recent developments. CELG stocks has made an important move over a recent downtrend line. This level was previous support, before becoming resistance after Celgene fell below it in early May. For bulls, it’s important that CELG stock stays over this level and does not make new lows.

Trend-line resistance is likely still in place though (the top black line near $85). Between $80 and $85, there could be some resistance. If CELG stock can push through it though, perhaps its lows really are in. Obviously bulls would cheer the move, as would holders of the iShares NASDAQ Biotechnology Index (ETF) (NASDAQ:IBB), given that CELG stock is the fund’s fourth-largest holding.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long CELG.